Economic indicators provide insight into the overall health and performance of an economy. They are essential tools for policymakers, advisors, investors, and businesses because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending on June 13th, the SPDR S&P 500 ETF Trust (SPY) rose 1.46% while the Invesco S&P 500® Equal Weight ETF (RSP) was down 0.21%.

Inflation has been an ongoing topic of conversation over the last few years because of its role in the Fed’s interest rate policy and its ability to quickly influence financial markets. The Fed has been reluctant to make any changes to monetary policy, emphasizing the need for more data and confidence that inflation is moving towards their 2% target. At their meeting last week, the Fed voted to keep interest rates between 5.25% and 5.50% for a seventh consecutive meeting and expects only one rate cut for 2024. This article looks to summarize three important economic indicators from the past week to provide insight into the latest trends in inflation and consumer sentiment.

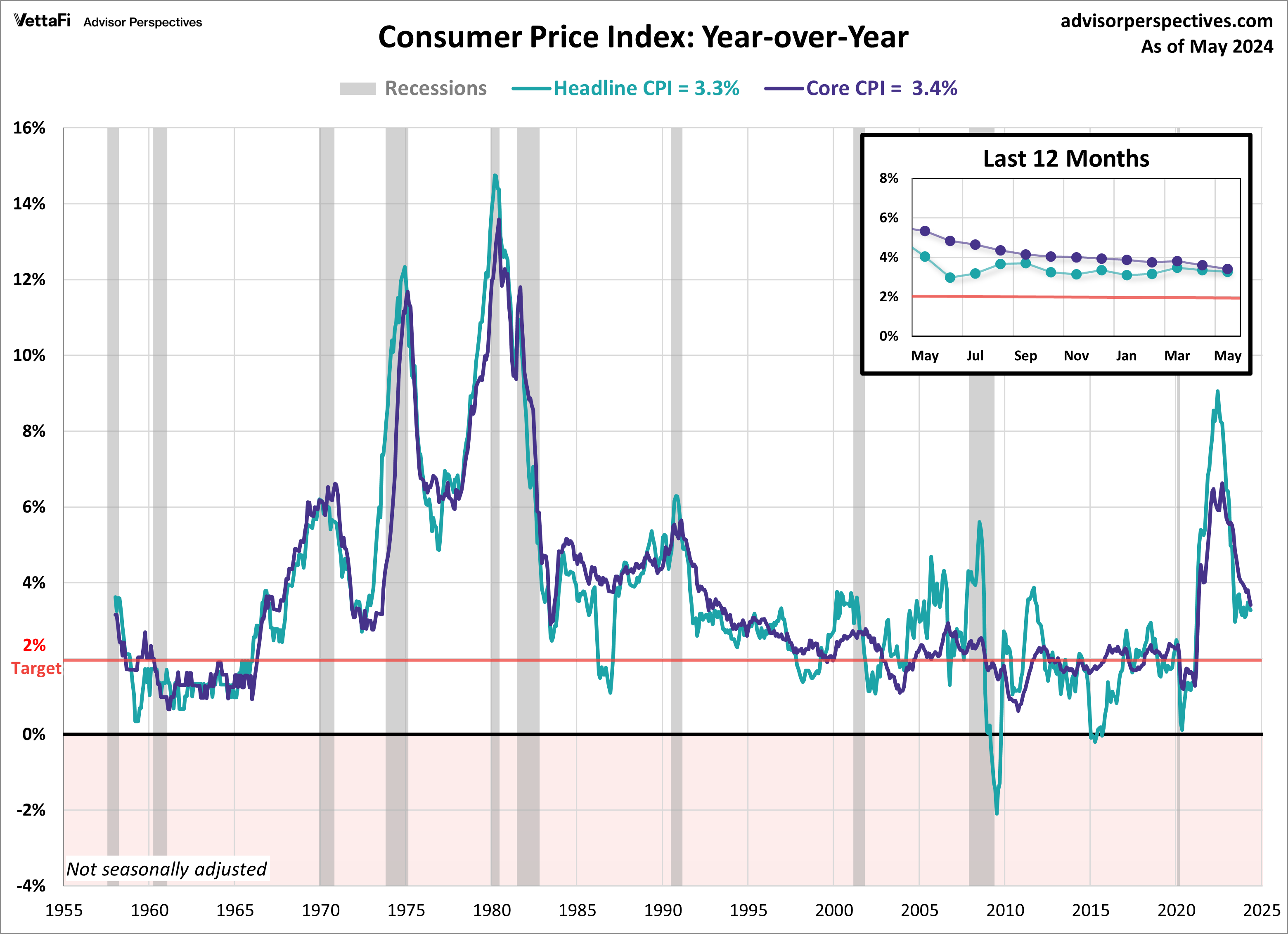

Economic Indicators: Consumer Price Index

Inflation continued to show signs of easing last month, even surprising to the downside, after several higher-than-expected readings to start off the year. The Consumer Price Index (CPI) rose 3.3% in May, down from 3.4% in April and below the expected 3.4% rise. Compared to the previous month, consumer prices were flat, which was lower than the expected 0.1% growth. In May, gas prices finally offered some relief to consumers’ wallets, dropping 3.6% from April and helping to slow inflation. However, the continued rise in shelter costs more than offset the decline in gasoline, as shelter costs rose 0.4% for a fourth consecutive month.

Core inflation, which excludes food and energy prices, cooled to its lowest level in over three years. Core CPI fell to 3.4% on an annual basis, coming in below the expected 3.5% growth. Additionally, core prices increased 0.2% from April, lower than the expected 0.3% growth.

It is still up for debate as to when the Fed will begin to cut rates. It’s still expected that the Fed will hold rates steady at their next meeting in July. And as previously mentioned, the Fed only expects one rate cut in 2024 according to their latest dot plot. At the time of writing, the CME Fed Watch Tool indicates a 90% likelihood for rate stability at the July meeting. However, the latest CPI numbers support the belief that two rate cuts this year remain a very real possibility. The CME Fed Watch Tool is currently showing a 61% probability that the first rate cut will take place in September with a December rate cut also on the table.

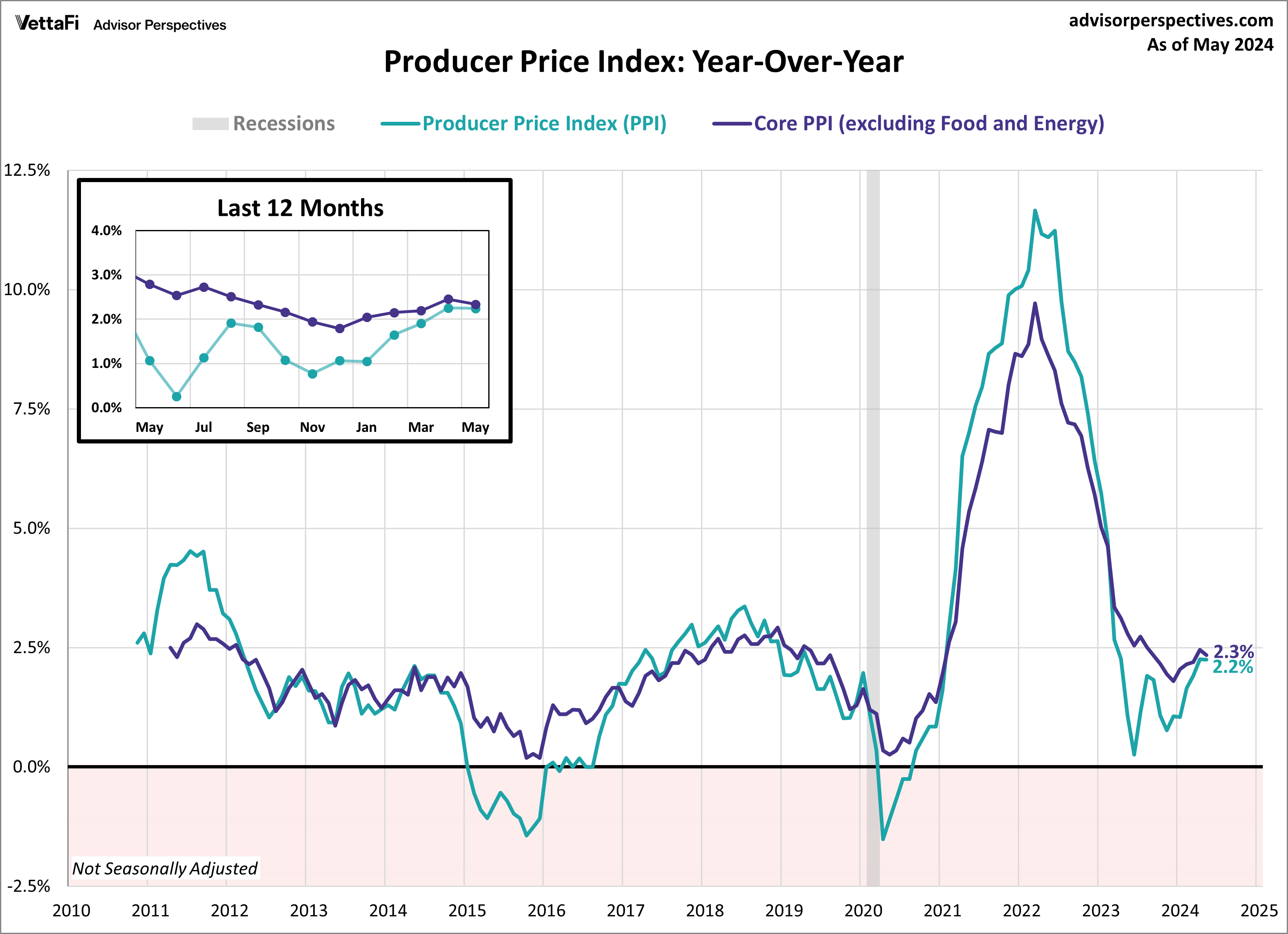

Producer Price Index

Wholesale inflation unexpectedly cooled in May, providing yet another positive sign for consumers. In May, the Producer Price Index (PPI) fell 0.2% from the previous month, less than the projected 0.1% growth from April. The latest figure is the largest monthly decline for the headline index since October 2023. On an annual basis, the PPI rose 2.2%, a slight slowdown from April’s 2.3% growth and below the expected 2.5% increase.

Additionally, the Core Producer Price Index (PPI), which excludes food and energy, was flat on a monthly basis, lower than the projected 0.3% growth. Core PPI was up 2.3% from one year ago, a deceleration from the previous month’s 2.5% rise in wholesale prices and lower than the projected 2.4% increase.

The producer price index is widely considered a leading indicator of consumer inflation, as shifts in producer-level prices often trickle down to consumers. The latest PPI report showed wholesale inflation cooling which could signal an easing in future consumer prices, ultimately providing some relief for consumers.

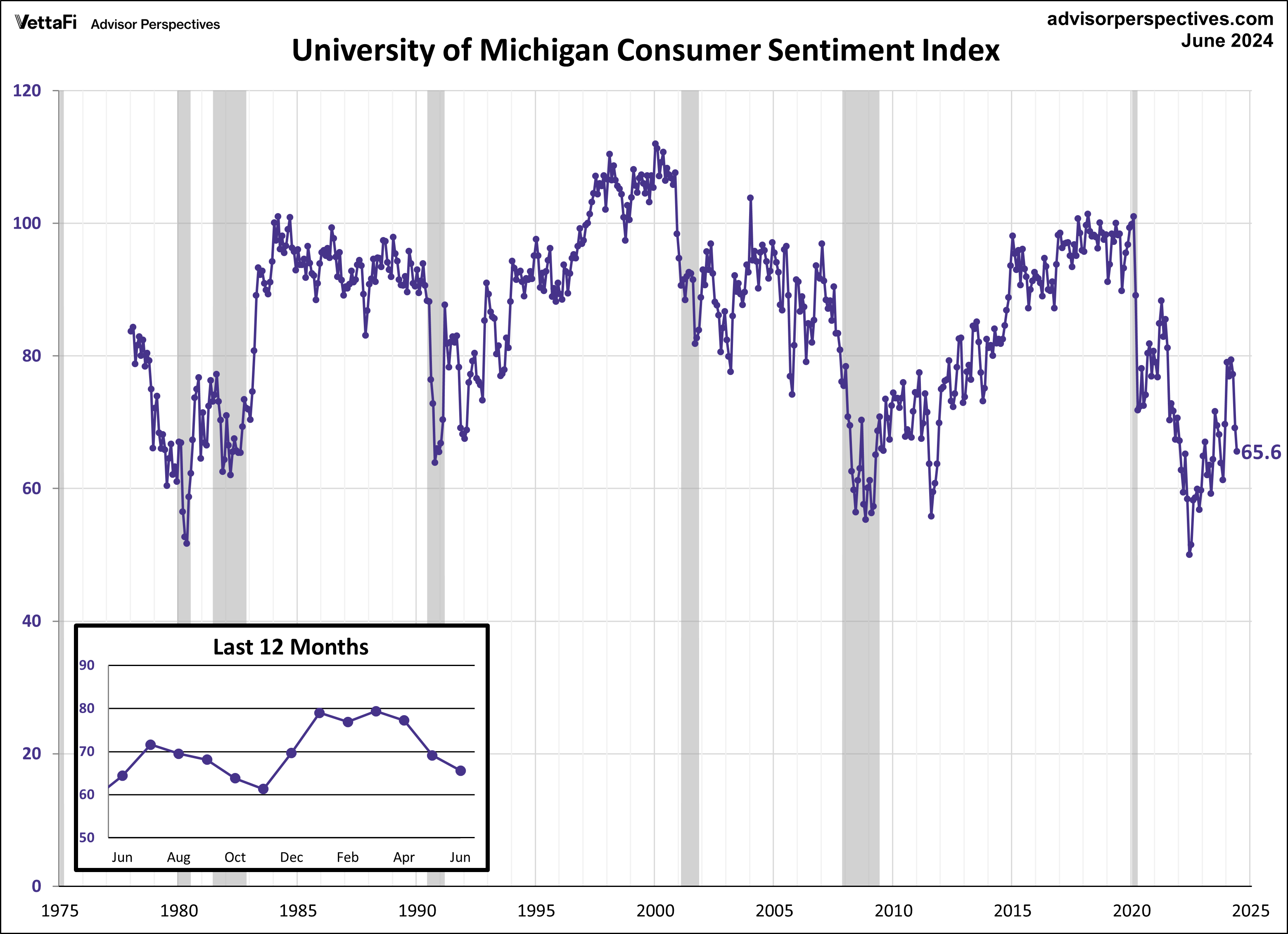

Michigan Consumer Sentiment

Consumer attitudes worsened this month according to the preliminary report for the Michigan Consumer Sentiment Index. The June preliminary report came in at 65.6, marking a 5.1% decrease from May’s final reading. The latest reading was well below the forecasted value of 72.1. Sentiment has now weakened for three consecutive months and is currently at its lowest level since November 2023.

The Michigan Consumer Sentiment Index is a monthly survey measuring consumers' opinions with regards to the economy, personal finances, business conditions, and buying conditions. In the latest report, consumers cited concerns over personal finances due to high prices as well as weakening incomes.

Consumer attitudes are closely monitored since their confidence levels tend to influence their spending behavior. Given that consumer spending accounts for approximately 70% of the economy, consumer spending has a major impact on economic growth.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

Economic Indicators and the Week Ahead

The upcoming week will unveil key economic data, featuring the latest figures on retail sales, industrial production, and the Conference Board's Leading Economic Index. Individually, these metrics offer insights into distinct aspects of economic activity: retail sales reflect consumer spending, industrial production measures manufacturing strength, and the Leading Economic Index provides guidance on future economic trends. But when taken together, they help paint a more holistic view of the economy's overall health.

The retail sales data could impact interests in the SPDR S&P Retail ETF (XRT) while the industrial production data could impact interests in the Industrial Select Sector SPDR Fund (XLI).

For more news, information, and analysis, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi