Monthly Global Economic Report

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsShould We Be Worried About a Recession? Not Yet, But . . .

The expert and you are in a car and the expert is driving. After awhile, you notice that the expert is driving the car by looking through the rearview mirror. Concerned you ask him why he’s not looking ahead as he drives. He replies that there is nothing to worry about since he can see that the road we’re driving on is straight. The expert believes that the straight road he sees in the rear view mirror is discounting the straight road ahead. By the time the curve in the road appears in the rearview mirror, the car you’re in is hurtling toward an unwelcome outcome. The trend is your friend—until it isn’t. Markets don’t discount the future, but they do an excellent job of discounting the past. But, we already knew the past, didn’t we?

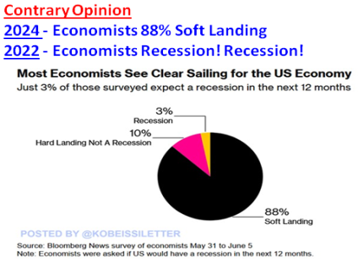

In the first week of June Bloomberg asked economists if they thought the US would have a recession in the next 12 months. Amazingly, Bloomberg’s survey found that 88% of the economists thought there would be a Soft Landing versus the 3% who thought a recession would develop. Another 10% thought the economy would experience a Hard Landing but still manage to avoid a recession. After seeing two consecutive quarters of negative GDP in the first half of 2022 in the rear view mirror, economists were confident a recession would take hold in 2022 or 2023. Instead, the economy kept motoring ahead. Now economists can only see growth in the rear view mirror so they aren’t worried about a recession taking hold anymore.

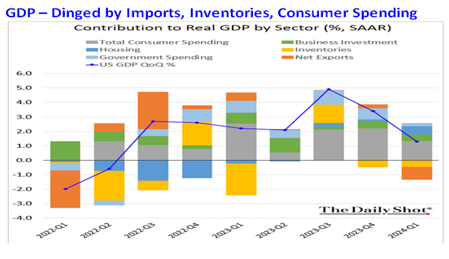

Contrary Opinion is taking the opposite side of a consensus narrative but only when there is data to warrant it. In 2022 and 2023 I didn’t think a recession would develop since monthly job averaged 399,000 in 2022 and a healthy 225,000 in 2023. In addition, GDP wouldn’t have been negative in the first two quarters of 2022 if it wasn’t for large downward adjustments from Imports (Q1) and a drawdown of Inventories (Q2). (Review GDP chart below showing quarterly breakdown for Net Exports – Imports and Inventories) These weren’t the only reasons why a recession wasn’t likely but the data was persuasive. In mid 2024 there are good reasons why I think the recession risk is higher than most economists realize since forward looking indicators of the labor market are uniformly pointing to a marked slowing in job growth. Consumer spending has buttressed the economy from higher interest rates, but that will change if the Unemployment Rate moves up meaningfully. Spending is being supported by the large increases in Net Worth, but that could change if the economy slows and the stock market falls out of bed. In the first half of this letter I’m going to review various indicators I’ve discussed previously to show why the economy is set to slow. In the second half of this letter I’m going to review the Advance – Decline Line and show how it has provided warning signs prior to recessions and large declines. Economists aren’t worried but the time for caution has arrived.

The third estimate for first quarter GDP in 2024 was revised to 1.4% 1.3%. As in the first report GDP was held down by an increase in imports (-0.9%) and decrease in inventories (-0.5%). As I’ve discussed imports reflect demand that is satisfied by production overseas, which is why it is subtracted from Domestic Production. A drop in inventories lowers GDP in the current quarter, but often lifts future GDP when inventories are replenished. Absent these two factors GDP growth would have been 2.7%, double the 1.3% reported. Normally, focusing attention on data that is far in the rear view mirror isn’t helpful. One reason for the revision that caught my attention was a marked drop in consumer spending, which was revised down from 2.5% to 1.5%. The consumer has been carrying the economy so any downshift in spending is worth noting. In April and May Retail Sales were softer than expected continuing the downshift.

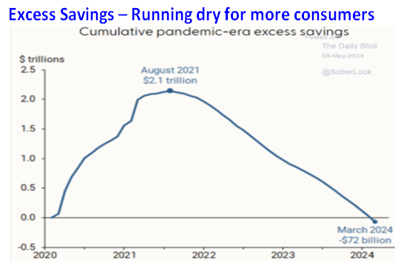

Consumer spending has been buttressed by a number of factors in the last few years. Consumers amassed more than $2.1 trillion in Excess Savings after the government transferred $3 trillion to consumers in direct payments and other benefits and spending tanked while the economy was shut down. The Unemployment Rate held below 4.0% for 27 consecutive months the most since 1969 before ticking up to 4.0% in May 2024. Wages have been growing by more than 4.0% and consumer savings have been earning 5.0% compared to nothing in March 2022. The big increase in home prices and the stock market since 2022 has increased the Net Worth of consumers by more than 40%. But there are clouds on the horizon which will diminish consumer’s ability to keep spending.

According to the San Francisco Federal Reserve Excess Savings peaked at $2.1 trillion in August 2021. Excess Savings are the amount of savings in excess of what would have been saved from personal income since 2019. Since July 2021 the Personal Savings rate has declined from 9.4% to 3.9% in May 2024, which is well below the pre Pandemic rate of 6.0%. Consumers have been drawing their savings down by roughly $85 billion a month since the peak in August 2021, and by March 31, 2024 the pool of Excess Savings will be drained. The increase in credit card and auto loan delinquencies are a symptom of the drawdown in Excess Savings. The absence of Excess Savings doesn’t mean the economy will crater. That will be determined by job growth and whether the Unemployment Rate remains low.

Will the Labor Market Weaken in 2024 and 2025?

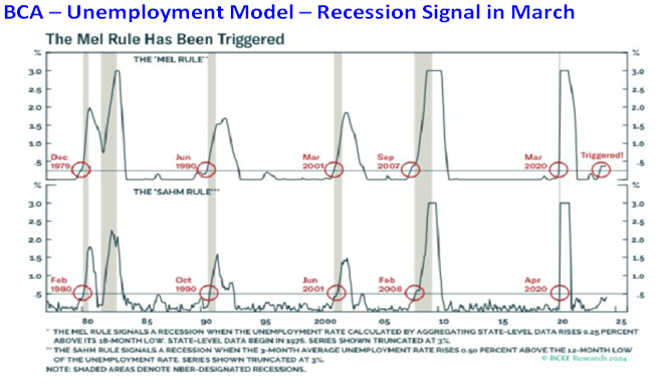

As noted a historically low Unemployment Rate (UR) has sustained consumer spending so any increase in the UR will send a ripple of caution through most consumers and cause the economy to slow. The BCA state level Unemployment Rate model provides a recession signal after it rises above its 18 month low by 0.25%. The BCA Unemployment Model predicted the recessions in 1980, 1982, 1990, 2001, and in 2008 – 2009 with a lead time of less than 6 months, and has never issued a false positive. In March the BCA model generated a recession signal, which indicates the labor market will weaken materially before the end of 2024.

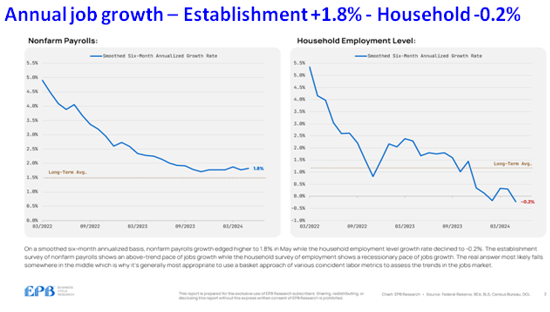

Over the last year monthly job growth has been overstated. The Establishment Survey produces the monthly job numbers and the Household survey generates the data for the Unemployment Rate. The two surveys treat the issue of part time jobs differently. In the Establishment survey a person who takes on a second part time job is counted as a new job, but the Household survey doesn’t. In May the Establishment Survey pegged job growth at a 1.8% annualized rate after 2.8 million jobs were created in the last 12 months. In contrast the number of jobs counted in the Household survey registered a decline of -0.2%. This is one reason why the Unemployment Rate is trending higher despite monthly job growth.

Normally, the Unemployment Rate trends down as the economy consistently generates more jobs. It is unusual for the Unemployment Rate to rise as job grow continues. When the Establishment survey has reported job growth but the Unemployment Rate was moving higher, it proved to be a warning that the economy was at an inflection point. Prior to the 2008 recession the mixed message from the Establishment survey (job growth) and an increase in the Unemployment Rate lasted 8 months (September 2007 – April 2008). The lead time before the 2001 recession was 6 months (January 2001 – June 2001), and 12 months prior to the 1990 recession (November 1989 – December 1990). The Unemployment Rate was 3.4% in April 2023, so it has been inching its way higher to 4.0% for 12 months.

Labor Market Is Already Weakening

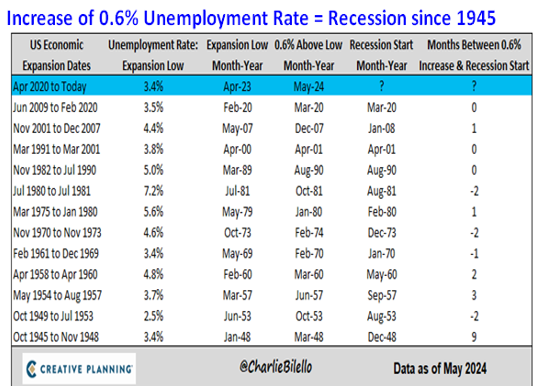

The increase of 0.6% in the Unemployment Rate from 3.4% to 4.0% has been gradual and non-threatening especially since the 6 and 12 month averages for Headline job growth have held above 200,000 per month. Although the increase of 0.6% in the Unemployment Rate seems innocuous, history suggests otherwise. Since 1945 an increase of 0.6% in the Unemployment Rate has preceded a recession without fail, which shouldn’t be a surprise. Businesses are reluctant to let good workers go so they resist firing workers for as long as they can, even as business growth slows. When the economy downshifts more and employers are forced to react to the weakness, the Unemployment Rate moves up aggressively. In the 12 cycles since 1945 the lead time between an increase of 0.6% and the onset of a recession was quite short (less than 3 months).

FOMC – Yield Curve Inversion

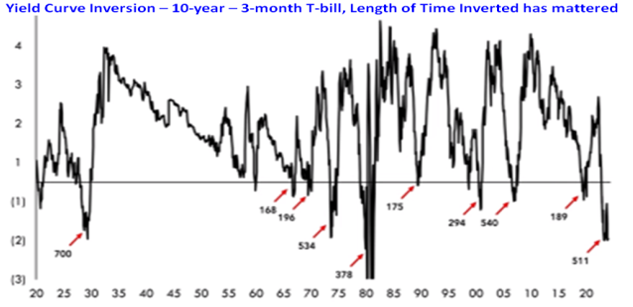

Since the first rate increase in March 2022 the FOMC’s goal has been to lift the Funds rate to a restrictive level to bring inflation down and without causing a recession. The lag time between when monetary policy is tightened and the onset of a recession has varied significantly. Since 1920 the amount of time the inversion of the 10-year Treasury yield and the 90-day T-bill lasts appears to be correlated with the depth of the eventual recession.

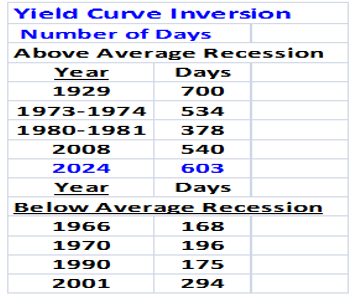

When the inversion has endured for more than 350 days the ensuing recession was deep. Since the numbers on the chart may be difficult to read, here’s a quick summary. Prior to the Financial Crisis in 2008 the inversion persisted for 540 days. The double recession in 1980 and 1982 was preceded by an inversion lasting 378 days. The yield curved remained inverted for 534 days prior to the recession in 1973–1974. Prior to the Great Depression in the 1930’s, the inversion lasted 700 days. Milder recessions were presaged by an inversion of 294 days in 2001, 175 in 1990, 196 in 1970, and 168 in 1966. The current inversion through June 20 is 603 days. Whether the length of the current inversion leads to a serious recession is debatable, but it does increase the odds of a materially slowing before the end of 2024 and in 2025 that few on Wall Street are expecting.

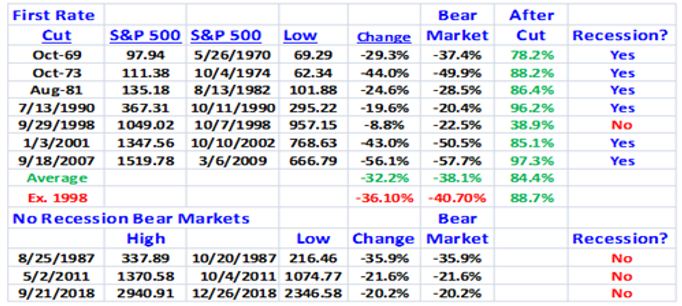

The FOMC hasn’t cut the Funds rate in response to inflation falling, but has when the economy was falling into a recession. Historically, when it became apparent that the economy was sliding into a recession the S&P 500 has declined sharply. These declines were the result of the expected decline in earnings and a compression in the market’s Price/Earnings ratio.

This double whammy took hold even though the FOMC started lowering the Funds rate to offset the severity of the recession. The average Bear Market decline in the last 7 instances was -38.1% and -40.7% (red) if 1998 is excluded. In 1998 the FOMC cut the Funds rate in response to an event, rather than the threat of a recession. In August 1998 Long Term Capital Management imploded and shook the financial system enough that the FOMC felt a response was required, even though the economy grew 3.9% in 1998. The average decline after the first FOMC cut was 84.4% of the total Bear Market decline when 1998 is included (green 32.2 / 38.1 = 84.4%), and 88.7% if 1998 is excluded (red 36.1 / 40.7 = 88.7%). The message from these numbers is clear: The bulk of the losses in the stock market occurred after the FOMC cut the Funds rate for the first time.

The FOMC uses a rear view mirror to drive the economy since the data guiding policy is 30 to 60 days old and is often revised measurably at inflection points in the business cycle. This virtually guarantees that the FOMC will be 3 months or more behind the economic curve. The FOMC has tried to minimize this monetary Achilles heel in the current cycle by holding the Funds rate at what appears to be a restrictive level for longer since last July, rather than hiking more as the economy continued to grow above its long term potential of 2.0%. Nonetheless, a recession has consistently taken hold in the last 60 years because the FOMC waited too long to make the first cut.

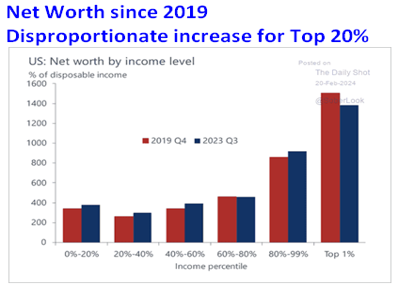

The odds of a significant slowdown if not an outright recession are increasing based on the trends and indicators discussed. A large decline in the stock market will show why the outsized increase in Net Worth for the top 20% is a two edged sword. Consumer spending is being sustained now as the wealth effect prompts discretionary spending by those who have benefitted the most from the increase in Net Worth (Top 20%). History shows that the stock market has suffered large declines when a recession developed, even if the FOMC cuts the Funds rate. If the stock market experiences a decline of more than 20% in the next 12 months, any slowdown in the economy will intensify as high end consumers cut back on travel, dining out, music concerts and consumption in general. The second edge of the sword is a cutback in spending by the wealthy which will make the recession deeper.

There have been many unusual aspects to the current business cycle due to the government and monetary responses to the COVID Pandemic, so the lead time could be longer. The message from the various labor market indicators I’ve reviewed suggests the Unemployment Rate is likely to move up more before the end of 2024. Once the increase in the Unemployment Rate makes headlines consumer spending will slow as workers with jobs become more cautious. The FOMC will respond at some point by lowering the Funds rate. Wall Street thinks the stock market will weather any slowdown or recession once the Fed cuts the Funds rate. History suggests that’s not correct.

Technical Warning Signs Are Increasing

There are an increasing number of technical indicators that are warning of a decline in the stock market that could be substantial through 2025. However, one must understand that the majority of institutional money managers and retail investors pay virtually no attention to technical indicators. Institutional money managers are ‘Buy and Hold’ investors and currently believe the economy will avoid a recession and that corporate earnings will continue to increase in 2024 and 2025. Unless they have a reason to sell they won’t, irrespective of warnings from technical indicators. Retail investors have been educated to only “Buy and Hold’ (and most adhere to that dogma), until the stock market declines a lot. At that point human nature takes over and mounting losses can be a persuasive motivator.

If the economy slows and unemployment increases as seems likely, institutional and retail investors won’t sell immediately as they will think a recession could still be avoided. They will start to sell if and when the economy slows enough to raise concerns that a recession may actually occur. Selling will increase as the onset of a recession becomes reality and the stock market declines more. This is why the largest losses in every Bear market since 1969 have been after the first rate cut by the Federal Reserve. The realization that the economy is in recession, so earnings estimates will have to be revised significantly lower in coming quarters is what causes an increase in selling pressure that swamps the reduced number of buyers. Historically, the stocks and sectors that benefitted most from the prior Bull market and are ‘over owned’ are the stocks that get hit the hardest in the Bear market.

Whether our car has a 6 or 8 cylinder engine we understand that if all the cylinders aren’t working together acceleration suffers, fuel economy drops, and ultimately significant damage to the engine develops. In a healthy stock market the majority of major market averages (cylinders) move up and down together. An uptrend or downtrend are confirmed when the majority of market averages make new highs or new lows together.

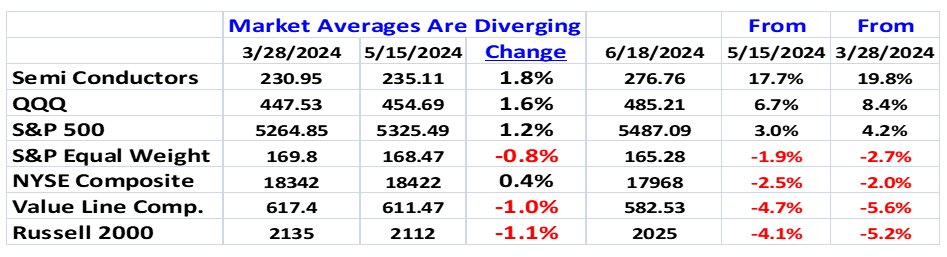

When the majority of market averages don’t record a new high or a lower low together it often signals that a change in trend is not far away. Recently, more money has been flowing into a smaller number of Mega Cap stocks rather than the broad market. The capacity of the stock market to withstand negative news is less when fewer stocks are strong. Since the initial high on March 28 broader market averages like the New York Composite (1700 stocks), Value Line Composite (1700 stocks), and the Russell 2000 have significantly lagged behind the S&P which only has 500 stocks. The Equal Weight S&P 500 assigns a 0.2% weight to every stock in the S&P 500 so 10 stocks are 2.0%. The top 10 stocks in the capitalization weighted S&P 500 contribute 36.1% to the daily percentage change and 8 are being boosted by AI enthusiasm. The buzz about the potential of Artificial Intelligence is why the Semi Conductor stocks have been performing so well with Nvidia being the leader of the pack. If the majority of these heavily weighted stocks are up on any given day, the other 490 stocks have to be weak for the S&P 500 to decline. This is why the S&P 500 can go up even though a majority of stocks decline and why the S&P 500 can make a new high even though the majority of stocks aren’t performing well.

From March 28 thru May 15 the negative performance gap between the Semi Conductor stocks and the NYSE Composite, Value Line Composite, and the Russell 2000 was relatively small. For the NYSE Composite was just -1.4% and -2.8 and -2.9% for the Value Line and the Russell 2000.

The negative performance gap widened considerably after May 15 through June 18. This shift highlights how more money is being funneled into fewer and fewer stocks. This has pushed the Semiconductor stocks up while the broad market is actually weakening. Since March 28 the Semiconductor Index is up 19.8%, but the S&P 500 Equal Weight is down -2.7%, the New York Composite is down -2.0%, the Value Line Composite has shed -5.6%, and the Russell if off -5.2%. In less than 3 months the Semiconductor Index has outperformed the S&P 500 Equal Weight by 22.5%, the NYSE Composite by 21.8%, the Value Line by 25.4%, and the Russell 2000 by 25.0%.

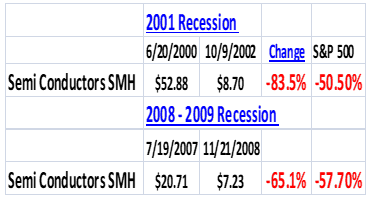

In 2000 the world was abuzz in how transformative the internet would be. As we know with the benefit of hindsight the internet has exceeded those lofty expectations. Think about this: When the Pandemic swept the world in 2020 and 2021, how would our economy been able to function if high speed internet didn’t exist? Semiconductors were at the forefront of the internet in 2000 and its phenomenal expansion ever since. The recession in 2001 was relatively mild with GDP only contracting by -0.4%, but semiconductor stocks lost -83.5% compared to a loss of -50.5% for the S&P 500. This occurred in large part because Semiconductor stocks were overvalued in 2000. In the 2008 recession GDP contracted by -4.3%. The S&P 500 fell -57.7% and the Semiconductor stock index lost -65.1%. The performance of Semiconductor stocks during recessions shows they are sensitive to the economy and highly cyclical.

I have no doubt that Artificial Intelligence will change the world in many ways in coming years, but that doesn’t change the reality of how Semiconductor stocks are likely to perform during the next recession. In recent months the Semiconductor stocks have been lifting the S&P 500 to higher highs and this trend could persist for awhile. When a recession materializes in late 2024 or in 2025, Semiconductor stocks will drag the S&P 500 lower just as they did during the last two recessions. During the 2001 recession businesses cut back on technology spending which popped the tech bubble and caused Semiconductor stocks to crash by -83.5%. In the last 12 months $50 billion has been invested in Nvidia chips but generative AI startups have only received $3 billion in sales. Unless this imbalance changes soon, demand for Nvidia chips will slow or even decline. During the next recession companies will look to cut costs just as they did in prior recessions so the demand for computer chips will plunge. At some point Nvidia’s stock will be cut in half from whatever the all time high proves to be.

The bifurcation between the major market averages isn’t the only technical indicator flashing yellow. The Advance – Decline Line is created by adding the daily difference between the number of stocks increasing and declining and adding the difference to a running total. If more stocks declined, the running total declines and rises if advancing stocks outnumbered declining stocks. In an uptrend more stocks consistently go up on the majority of trading days and the Advance – Decline Line (ADL) trends higher. It is healthy and a reflection of a strong market when the ADL line confirms a new high in the S&P 500 by also making a higher high. In a confirmed downtrend the ADL will make lower lows as the S&P 500 declines confirming a downtrend.

Trend changes in the S&P 500 have often been signaled when the ADL doesn’t confirm either a new low in the S&P 500 or a new high. If the S&P 500 drops to a lower low and the ADL records a higher low, a positive change in trend is more likely. Conversely, if the S&P 500 makes a higher high but the ADL is below its prior high, a Negative Divergence is signaled. Since 1928 the majority of declines of more than -20% have been preceded by an ADL Negative Divergence. No Technical Indicator is infallible but the Advance – Decline Line is one of the more reliable technical indicators especially when a Negative Divergence has developed.

The capacity of the stock market to withstand negative news is less when fewer stocks are strong, but the depth of the subsequent decline is dependent on the strength and staying power of the reason to sell. If an event explodes after a Negative Divergence the decline has often been greater than -20% but compressed in time. Once the fallout from the event is contained the stock market stabilizes and usually resumes the uptrend if the economy is good shape. The best example is the 1987 Crash in which the S&P 500 lost more than -30.0% of its value but economy was strong and the S&P 500 resumed its bull market. Declines that are accompanied by a recession are more protracted since earnings contract for 2 or more quarters. Now let’s review how valuable the Advance – Decline Line (ADL) has been.

2021 - 2022

In November 2021 the S&P 500 and the ADL jointly made higher highs. In January 2022 the ADL was lower than in November as the S&P 500 topped at 4818. The FOMC provided a good reason for institutional investors to sell in 2022 as it aggressively increased the Funds rate. From the January peak of 4818 the S&P 500 fell to 3492 a drop of -27.5%.

2007 - 2009

The S&P 500 and the ADL registered new highs in June 2007. However, in October the S&P 500 reached a higher high but the ADL was well below its June level. In late 2007 I wrote that a recession was coming in 2008, and in July 2008 warned that a liquidity event was developing. This is an excerpt from the July 2008 Macro Tides. “Even though the Federal Reserve has slashed the Funds rate from 5.25% to 2%, and pumped hundreds of billions of dollars into the banking system, the balance sheets of large banks are so burdened, and the credit market is so dysfunctional the net effect is a tightening of monetary policy.”

In the August 2008 Macro Tides I noted the ineffectiveness of the Federal Reserve’s actions and the potential risk. “One of the most dangerous experiences a pilot can face is if his airplane rolls into a spiral decline. As the plane falls and begins to spin, the pilot loses orientation, which makes it difficult to regain control. As the plane falls, it gains air speed, making it even more difficult to pull out of the spiral. The pilot usually has less than 30 seconds to make all the correct decisions. If he doesn’t, the airplane gains so much downward momentum, it becomes impossible to pull out of the spiral. Pilots refer to this as a ‘death spiral’. The Federal Reserve has done everything it can to reflate the deflating credit bubble, and I’m sure they will be forced to do even more in coming months, since the plane they are piloting is still spinning and falling.” In September 2008 Lehman Brothers failed and a full blown credit crisis swept through Wall Street. From its high of 1576 in October 2007 the S&P 500 lost -57.4% of its value before bottoming in March 2009.

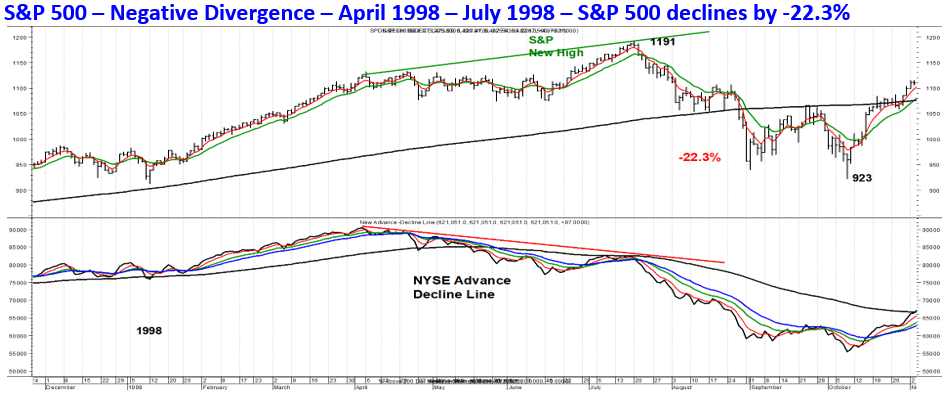

1998

The S&P 500 was in a strong uptrend before reaching a high in April 1998. The ADL mirrored the strong move up in the S&P 500 and also reached a new high in April. The S&P 500 experienced a modest -5.0% correction from early April into June, before rallying to a higher high in July. During the S&P 500’s correction, the ADL was weak so that when the S&P 500 reached a higher high in July the ADL was noticeably lower. On August 17 Russia defaulted on its debt which sent a shock wave through the global financial system. Long Term Capital Management was a hedge run by 2 Nobel Prize recipients in economics and lost more than -10.0% of its assets from its exposure to Russian debt and other credit instruments in August. In late September the Federal Reserve orchestrated a $3.6 billion bailout to contain a potential systemic meltdown. The Fed’s actions stabilized the financial system but didn’t prevent the S&P 500 from falling -22.3% from its July peak. In 1998 GDP grew by 4.5% and 4.8% in 1999. This is another example of an event crisis that didn’t do lasting harm to the economy.

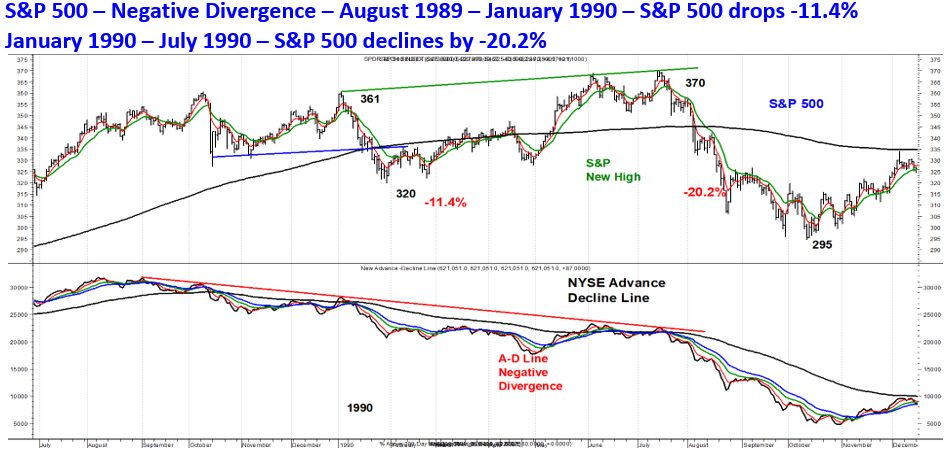

1989 - 1990

The two Negative Divergences that developed in 1990 provide a study in how a good reason to sell results in a larger decline. The S&P 500 reached a higher high in January 1990 compared to its level in August 1989. In January 1990 the ADL was lower so a Negative Divergence was signaled. The S&P 500 quickly lost -11.4% by the end of January. Some of this decline occurred after the S&P 500 fell below the lows in October and November 1989, so -4% of the -11.4% decline was due to technical selling.

After bottoming in January 1990 the S&P 500 subsequently rallied 15.6% to a higher high in July, but the ADL was well below its January peak. On August 2 Saddam Hussein invaded Kuwait which sparked a large increase in oil, from $21 a barrel at the end of July to $46 in October 1990. From its high in July the S&P 500 shed -20.2% by October when oil prices peaked. The US economy experienced an 8 month recession that ended in March 1991 after GDP fell -1.8%.

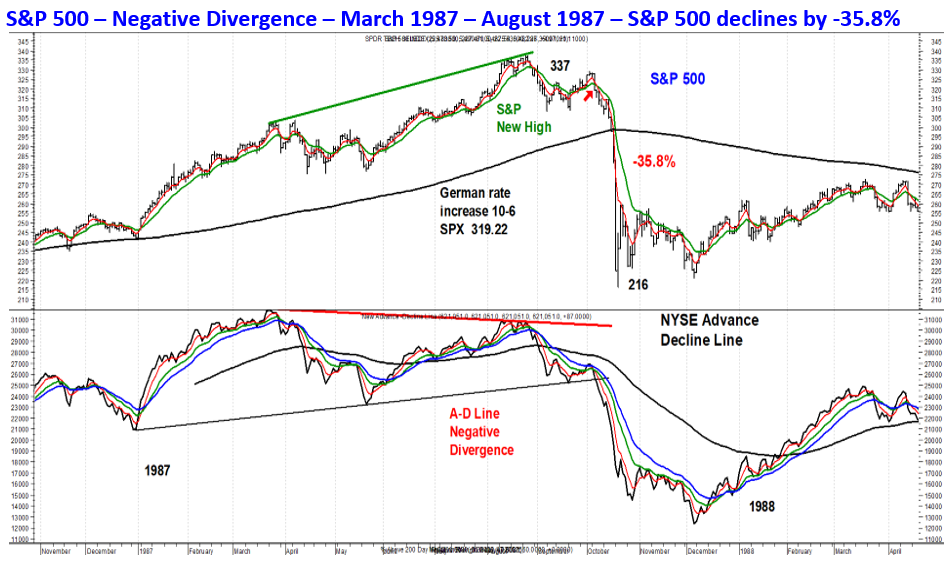

1987

In 1987 the S&P 500 rallied strongly before reaching a short term high in March, which was followed by a correction of -8.6%. By August the S&P 500 had rallied to another new high of 337.89, but the ADL didn’t confirm and then weakened significantly when the S&P 500 rebounded to 328.94 on October 2.

In 1987 the Dollar was weak and after August 11 it declined from 101.88 to 96.00 on September 3. Treasury Secretary James Baker had been told by Germany that the German Bundesbank wouldn’t increase the policy rate as that would strengthen the German Mark and weaken the Dollar. The Dollar bounced to 99.2 on October 1. On October 6 the Bundesbank increased its policy rate and the Dollar began a decline that brought it down to 90.05 on November 10. This is one factor that contributed to the S&P 500’s decline of -3.0% on October 6. By October 15 the S&P 500 was down -9.4% from its high on October 2.

Portfolio Insurance was used by Pension funds in 1987 which required they sell S&P 500 futures as the S&P 500 fell. At times this caused the S&P futures to trade below the S&P 500 cash. Arbitrage firms closed the gap between the discounted futures and the cash by buying the futures and selling the cash. Although these trades briefly narrowed the gap between the futures and the cash and stabilized the market, the decline in the S&P cash led Pension funds to sell futures again. At one point on October 19, 1987 the futures traded -10% below the cash and the Crash was on. On October 20 the Federal Reserve intervened with an injection of liquidity and many large companies announced their intention to buy their stock. These actions stabilized the market and a possible financial crisis was averted. The S&P 500 declined -20.2% on October 19 but the economy was strong growing 3.5% in 1987 and 4.2% in 1988.

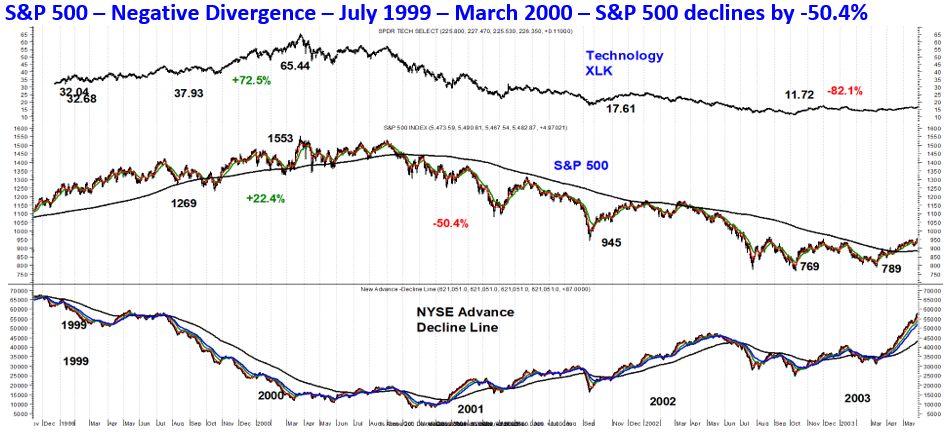

1999 - 2003

The ADL declined nonstop from July 1999 into March 2000. During the same period the S&P 500 rallied from 1269 to 1553 a gain of 22.4%. This was made possible because Technology stocks (as measured by the Tech ETF XLK) increased by 72.5%. Between July 1999 and March 2000 and tracking the decline in the ADL the broad market as measured by the Value Line Composite fell -16.6%. Something similar has been happening since March 28, 2024. The Semi Conductor index is up 19.8% through June 18, Tech XLK is up 10.7%, while the Value Line Composite is down -5.6% (Table on page 8).

By March 2000 Technology represented 34% of the S&P 500. From its March 2000 high Tech (XLK) lost -82.1% of its value as the S&P 500 dropped by -50.4%. Although the economy experienced a shallow recession (GDP was down -0.4%), the Bubble valuation assigned to Tech stocks and the unwinding of the Tech Bubble is why the S&P 500 declined from its March 2000 high of 1553 high until October 2002 when the S&P 500 hit 769.

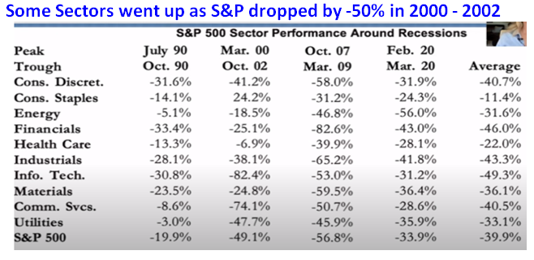

When Technology stocks broke down in October 2000, money rotated into cyclical stocks. The S&P 500 continued to decline because of the overweight of Technology stocks, but the ADL bottomed in October 2000. As the S&P 500 declined in 2001 and 2002 the ADL proceeded to make higher highs and higher lows as some sectors went up in price and others fell far less than Technology. There were more stocks in these sectors than the number of Tech stocks. Between March 2000 and October 2002 Consumer Staples gained 24.2%, Health Care only fell -6.9%, while Energy stocks declined by -18.5% which was less than the -49.1% plunge by the S&P 500.

As we have seen the correlation between the S&P 500 and the Advance – Decline Line is usually tight. But from 1999 through 2002 that wasn’t the case. The Negative Divergence that developed in March 2000 provided a good warning about the S&P 500 and especially Technology stocks. After the ADL bottomed in October 2000 and began to trend higher, the ADL provided a good reason to look at the Sectors within the S&P 500 other than Technology to identify which sectors were outperforming.

Negative Divergences by the Advance – Decline Line were registered in 1972 – 1973 before the S&P 500 declined by -48.2%, before the S&P 500 fell -36.1% in the 1970 bear market, the decline of -28.0% in 1961 – 1962, and the 86.2% plunge in 1929 – 1932. So what’s the current message from the Advance – Decline Line?

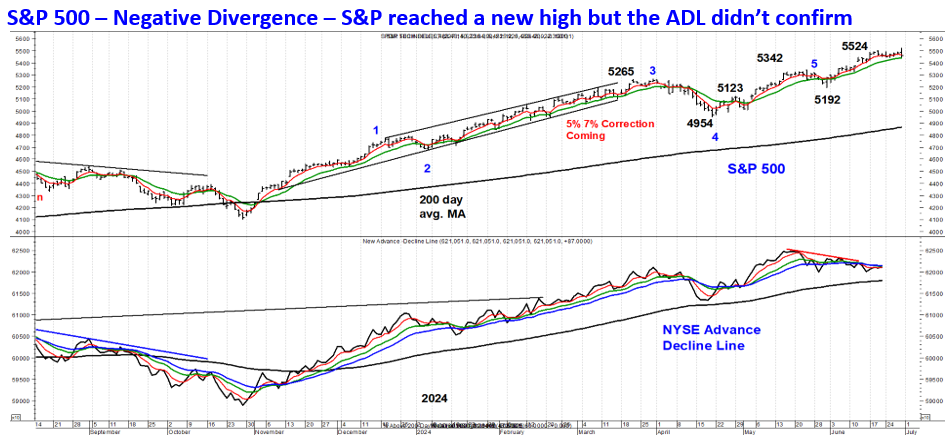

2024

Since May 15 the S&P 500 has rallied from 5325 to 5524 on June 28. However, the ADL peaked on May 15 and has been far weaker than the S&P 500, which is why it has recorded a Negative Divergence in June. In late March I thought the S&P 500 was likely to decline by -5% to -7% after Nvidia, the Semi Conductor Index, and the S&P 500 experienced Negative Key Reversals on March 8 and second Negative Key Reversal on April 4. The S&P 500 fell -5.7% as Nvidia and the Semi Conductor Index fell more. This correction unfolded even though the ADL confirmed the March 28 high. The Table of the market averages on page 8 shows the broad market has been far weaker since the high on May 15. The Negative Divergence signal from the ADL in June and the weakness in the broad market averages suggests the S&P 500 is vulnerable to a decline of more than -5% to -7%.

As the analysis of the ADL indicates the lag time between a Negative Divergence signal and a larger decline varies and is more dependent on when a good reason to sell motivates institutional investors to sell. The majority of investors who have a diversified portfolio though have already seen deterioration in the value of their account since May 15.

In the June 24 Weekly Technical Review I recommended aggressive traders establish a short position in the S&P 500 if it traded above 5505. “If Nvidia and SMH rebound as the broader market averages bounce more, the S&P 500 can make another new high above 5505. Most rallies in any market average are comprised of 5 waves, but it’s possible that an extended rally will be 9 waves or even 13 waves. Since the low of 5191 on May 31 the S&P 500 appears to have rallied in 7 waves to 5505 with wave 8 being the current dip. As long as the S&P 500 holds above 5402 one more rally for wave 9 above 5505 is possible. The rebound in the broad market averages isn’t expected to follow through since it would require solid evidence that the economy was strengthening. Since mid May the opposite has occurred.”

“Irrespective of the short term squiggles a deeper correction in coming weeks is likely. The 50% retracement of the rally from 4954 to 5505 is 5230 with a decline to near 5191 (wave 4 of lesser degree) also a target. A larger decline will be dependent on data showing that the economy is slowly meaningfully and that may not develop until after Labor Day. Aggressive traders can establish a 25% short position in the S&P 500 (via inverse ETF SH) if the S&P 500 trades above 5505.” This trade was triggered on June 28 when the S&P 500 rallied to 5524 before reversing lower. In the process the S&P 500 registered a Negative Key Reversal. Based on seasonality the market may hold up in the near term since the first half of July is the best two week period of any 2 weeks in the year, and the 4th of July is usually a plus.

Treasury Yields

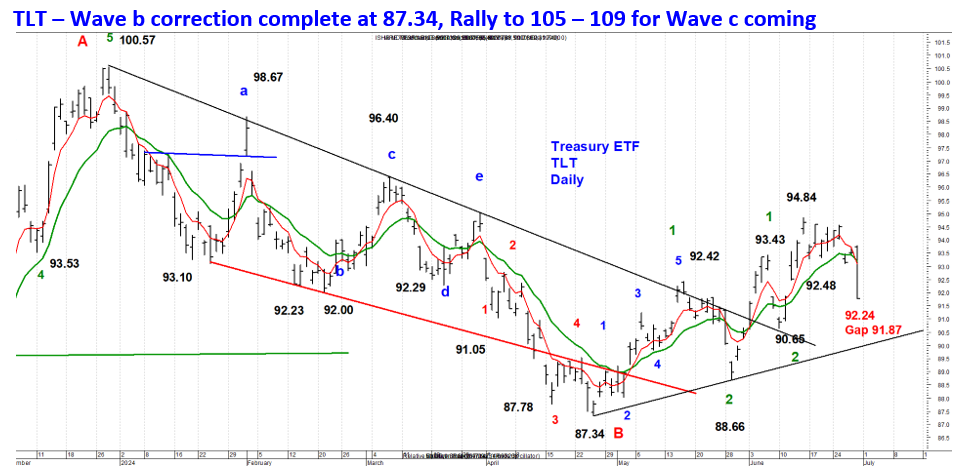

If the economy slows as expected Treasury bonds will rally strongly. TLT plunged from 179.70 in March 2020 to 82.42 in October 2023 for 43 months. At a minimum TLT can be expected to rally for 23.8% of the 43 month plunge (10 months), or until August – September 2024. If the rally consumes 38.2% of the time TLT spent declining, the rally could last for 16 months or until April 2025. TLT’s move up from 82.42 to 100.57 was the first phase (wave a) of a large rally that is expected retrace a portion of the decline from 179.70 to 82.42. The decline from 100.57 to 87.34 represents (wave b), which should be followed by another large advance (wave c). Wave c is expected to lift TLT above 100.57 and potentially to 105 – 109 by August – September or April of 2025. If TLT retraces 38.2% of the 97.28 point drop, TLT could rally up to 119.58.

The Personal Consumption Expenditures Index (PCE) for May was released on June 28 and showed a larger drop in inflation during May than expected. The annual rate for the Headline and Core fell to 2.6% from 2.7% and 2.8% for the Core in April. This was good news but was overshadowed by the Presidential debate which increased the odds that Donald Trump will be the next President. Since he is viewed as better for the economy and potentially worse for inflation, Treasury bonds declined despite the better inflation news. This drop occurred on a summer Friday and is overdone. The economy is set to slow and the next president won’t be sworn in until January 20, 2025, and any policy changes won’t impact the economy until mid 2025 or later. The decline opens the door for a possible drop below $90.65. Investors are long TLT at $91.13 and I’m lowering the stop to $88.66 from $90.65. TLT closed the gap at 91.87 on June 28.

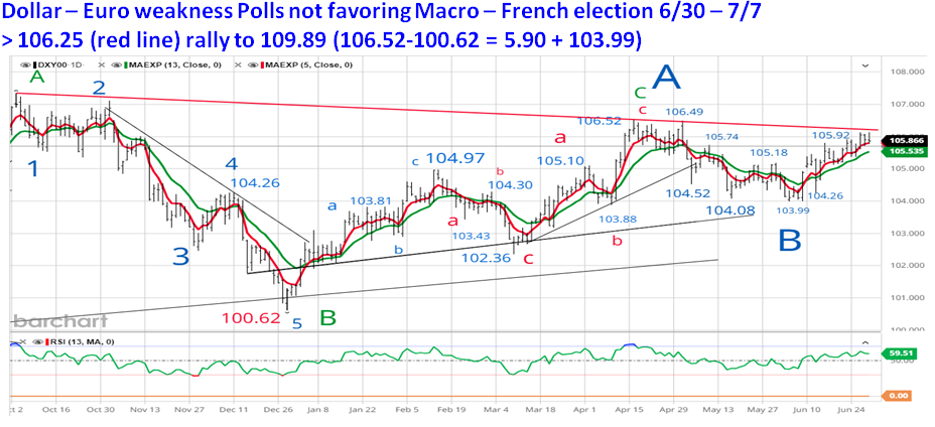

Dollar

In the last two weeks the Dollar has been trading off the coming French elections on June 30 and July 7 than economic data in the US. The uncertainty about the outcome and the prospects it may hold for France and the European Union has caused the Euro to decline and it represents 57.6% of the Dollar index. European Union rules hold member countries to keeping the annual deficit to less than 3% of GDP and the total ratio of debt to GDP at 60%. France’s deficit in 2024 will be 6% and its debt to GDP is 75%. A new President may not want to abide by the EU rules. This could cause a showdown that raises the possibility of France leaving the EU. That would be very disruptive and isn’t likely to happen, but we live in interesting times. French polls have shown that President Macron isn’t doing well so the outcome may not be a big surprise. But it’s what the future may hold that’s the larger issue.

The Dollar is hovering just below the red trend line and a solid break above it would allow the Dollar to rally to 109.89. Dollar strength is not a plus for the US economy as it makes US exports (12% of GDP) more expensive.

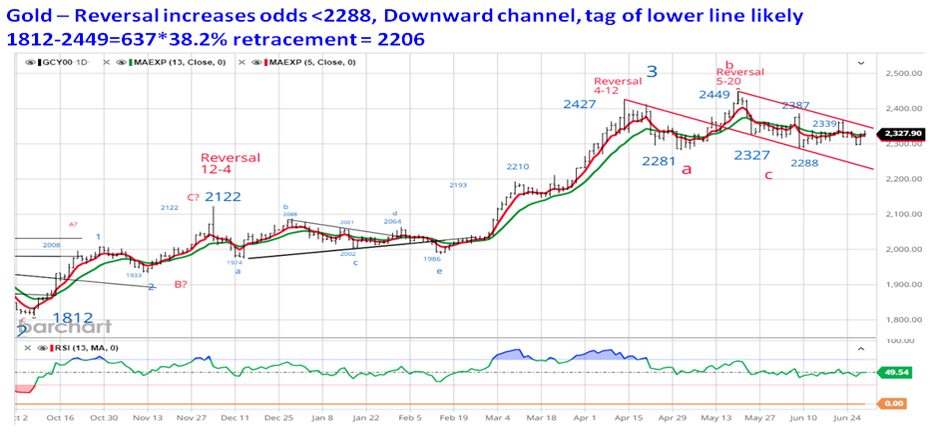

Gold

A surge in the Dollar would put pressure on Gold and the price pattern agrees. Gold is stuck in a downward trending channel which suggests Gold can drop below the lows of $2281 and $2288 before a trading low is in place. The 38.2% retracement of the rally from $1812 to $2449 is $2206, although I’ll be surprised if Gold reaches it. There must stops under the prior lows of $2281 and $2288, so a decline below these support levels will trigger stop loss selling that could easily cause an additional decline of $30. Aggressive traders can establish a 50% position at $42.65 and increase the position if IAU trades below $42.15.

The correction that started when Gold reached $2427 or $2449 is wave 4 from the low of $1812 in September 2023. Once wave 4 is complete Gold is expected to rally above $2449 at a minimum and probably above $2500. IAU would be expected to rally above $46.08 and might exceed $46.50 in wave 5.

Recommendation

I’ve known Jim Puplava for a long time and we both are concerned about the risk of a Secular Bear market in stocks developing in the not too distant future. Most Financial Planners adhere to the Buy and Hold investment approach which is appropriate during a Secular Bull Market. Jim has been a financial advisor for decades and I know he anticipated the large declines in Tech stocks during the 2000 – 2002 Bear market and the Financial Crisis in 2008.

Financal Sense

“Looking for a seasoned money manager? Reach out to Jim Puplava at Financial Sense Wealth Management, who is also a regular reader and follower of my newsletter. Jim and his firm are based in San Diego, CA, and provide money management and comprehensive financial planning services to clients all over the US. You can contact his firm at (888) 486-3939 or visit their website at www.financialsensewealth.com. Please note that I am not a client of Financial Sense Advisors, Inc, an SEC registered investment advisor or Financial Sense Securities, Inc, member FINRA/SIPC, both firms doing business as Financial Sense Wealth Management. I was also not paid compensation for this endorsement. The statement above may not be representative of the experience of other customers and this endorsement is no guarantee of future performance or success.”

The Daily Shot

Every month I include dozens of charts and the majority of them come from The Daily Shot. I highly recommend those who like charts of economic data to subscribe to The Daily shot.com.

Jim Welsh

@JimWelshMacro

[email protected], MacroTides.com

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All