Weak Labor Data and Reduced Growth Expectations Boost Rate Cut Hopes

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“’Passing through difficulties.’ We often feel that suffering will engulf us, or that the suffering will never end, but if we can realize that it, too, will pass, or as the Buddhists say, that it is impermanent, we can survive them more easily, and perhaps appreciate what we have to learn from them, find the meaning in them, so that we come out the other side, not embittered but ennobled. The depth of our suffering can also result in the height of our joy."

Dalai Lama, Desmond Tutu, and Douglas Carlton Abrams; The Book of Joy

The View from 30,000 feet

Putting it all together

- Weak employment data last week in the form of ISM Employment data, Initial and Continuing Jobless Claims, Unemployment and Nonfarm Payrolls have combined with recent downward pressure on GDP expressed in Nowcast models to skew worries about employment and growth to the downside.

- The drumbeat from pundits and economists that the Fed is behind the curve on plans to cut rates is getting louder every Although projections are that the Fed will make their first move to cut interest rates in September, with probability as tracked by the CME FedWatch Tool increasing from 73% to 78% last week, the whisper on the Street is that weak inflation data this week, in the form of a soft CPI print on Thursday, will make July a live meeting for a rate cut.

- As Q2 earnings season kicks off, expectations are that companies will put up another strong quarter of As long as the data indicates real wage growth is in excess of inflation, theoretically, consumers should have more disposable income to put to work, which should support earnings.

- We continue to be optimistic about risk-asset prices in the short-term, but our positive outlook is contingent on continued strength in labor markets that flows though to corporate This is a heavily data dependent market. The current condition could persist longer than many expect, or it could end abruptly, but we believe data will act as a guide along either path.

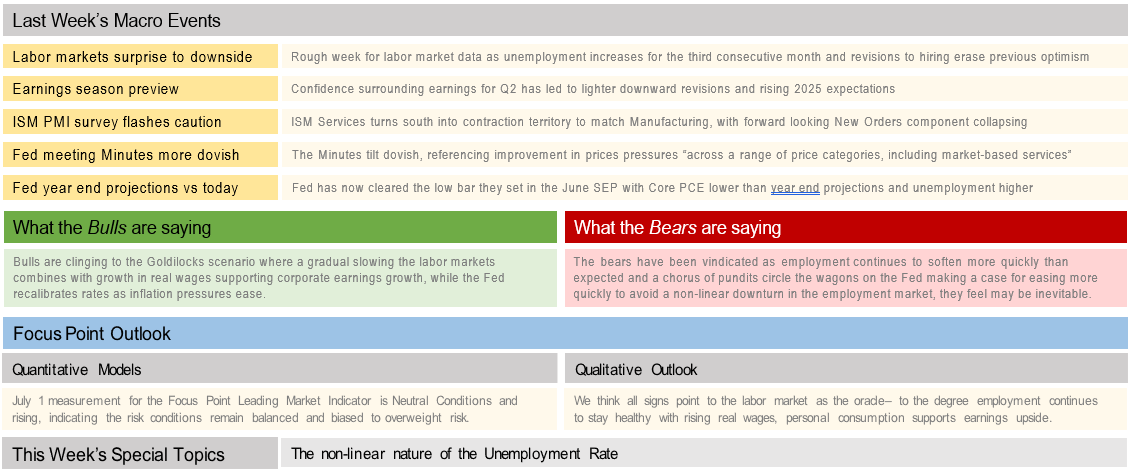

Labor markets surprise to downside

- Highlights (lowlights) from the most recent labor market report:

- The Unemployment Rate rose to 4.1%. The third consecutive increase, reaching the highest level since November of 2021.

- After a steep two-month revision of -111k, the three-month average of Nonfarm Payroll gains is now 177k, which is below the 200k number Fed Governor Lisa Cook recently estimated that the economy needs to produce to keep up with population growth, and deeply below where 2023 ended at 242k. Keep in mind that since 2023 payroll revisions have been negative 85% of the time, so odds favor that the 177k may soften further as well.

- Prime Age (25-54 year old) Labor Force Participation has now risen to 7, the highest level since 2002. Increased participation may be a sign the workers are having trouble keeping up with expenses.

- The number of Unemployed Workers has risen by 1.1 million since the beginning of 2023. The larger pool of unemployed is driving up Continuing Jobless Claims, the Duration of Unemployment and the Unemployment Rate.

- Out of the 24 indicators of the labor market that Focus Point follows, currently only three providing a positive signal in our employment model.

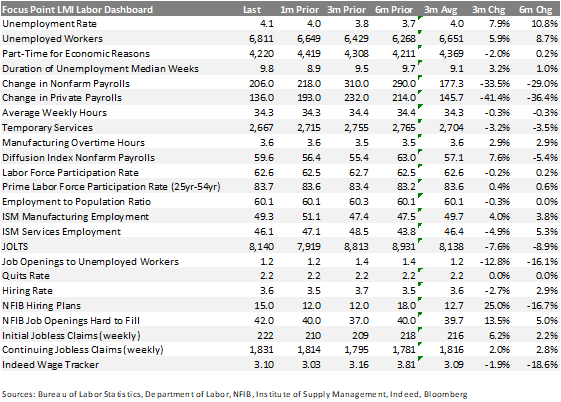

Earnings season preview

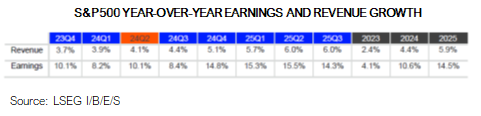

- Over the last three months earnings estimates have fallen 0.5%, which compares favorably since 2021. Over the last 20 years, earnings estimates have averaged a decrease 4.0% in the three months preceding the end of a quarter.

- Q224 Earnings look to be strong, the key questions will be related to guidance. According to I/B/E/S estimates table above, revenue and earnings growth accelerate rapidly beginning in Q424, which is inconsistent with consensus GDP and Consumer Spending estimates according to Bloomberg surveys that are projected to fall in the same time period. They both cannot be correct.

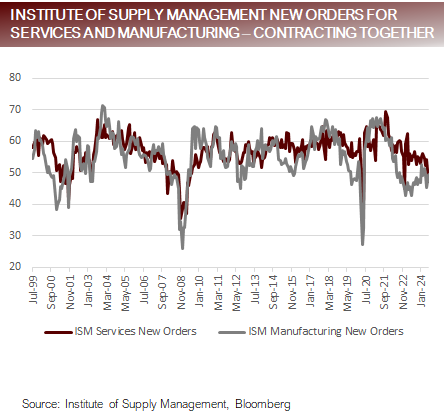

ISM PMI survey flashes caution

- Weakness in the Manufacturing Sector has spread to the Services Sector.

- Manufacturing Headline ISM Survey in contraction zone for the last three months and contracting 19 out of the last 20 months.

- Services Headline ISM Survey in contraction zone, falling to the lowest level since May of 2020.

- Summary of comments provides but the Institute of Supply Management in each of the sector reports:

- Manufacturing – key words from respondents reference weak demand and reduced backlogs, orders and inventories

- Services – key words from respondents reference inflationary forces still problematic and supply chain challenges.

- On the surface, weak PMI Surveys are cause for concern, but in the context of the current cycle, the surveys have been a poor indicator of economic activity. Further, S&P Global’s PMI Survey is providing conflicting findings.

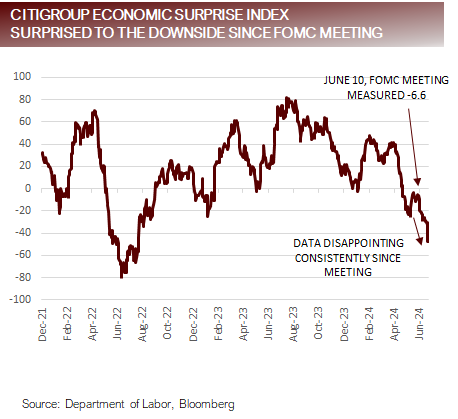

Fed meeting Minutes more dovish

- Minutes from the Federal Reserve Open Market Committee Meeting revealed discussions that indicated that members felt more balanced about the risks between inflation and growth than in previous meetings, which had favored risks related to inflation.

- Inflation comments centered around dialog including comments about retailers cutting prices, broad price reductions across categories, including services, and noting factors that may promote continued disinflation.

- Growth comments centered around dialog including questioning the data indicating recent job growth, concern that slowing growth could increase layoffs and views that the normalization in the labor market may mean that demand weakness from restrictive policy could pressure employment market.

- Perhaps the most interesting thing about the Minutes is what has happened since the June 10th, the date of the meeting. Growth and employment data have materially disappointed, which should tip the Fed toward a more dovish stance based on the tone of the meeting.

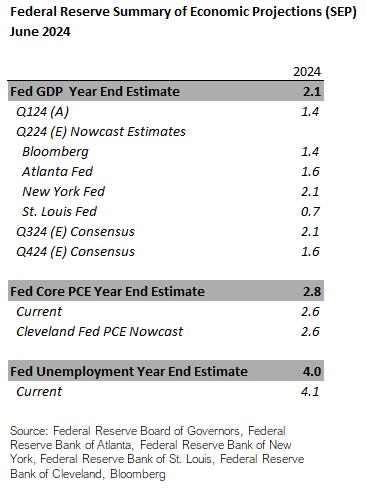

Fed year end projections vs today

- Less than a month ago the Federal Reserve Board of Governors met and updated their Summary of Economic Projections, laying out what they thought the most likely path was for growth and inflation.

- GDP projections are too high compared with actual and estimated performance through Q2, as well as compared to consensus economist estimates.

- PCE projections are too high compared with most recent Core PCE. In fairness, due to base effects the second half of the year could be more challenging.

- Unemployment projections are too low compared to the most recent Unemployment Rate. In addition, the risks are heavily skewed toward increase labor market stress with an uptick in claims data and broad weakness shown in Focus Point’s Labor Dashboard.

- The June SEP essentially lowered the bar for the Fed, making it easier to cross the threshold where they would begin cutting rates.

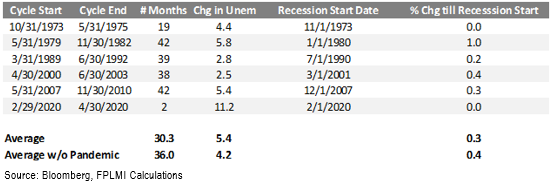

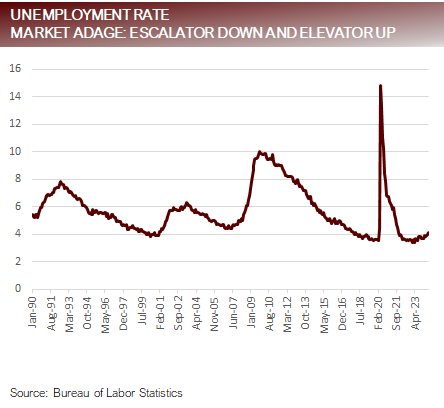

The non-linear nature of the Unemployment Rate

- There’s an old market adage – Unemployment takes an escalator down and an elevators up.

- In the last 50 years there have been 6 unemployment cycles.

- Excluding the pandemic, the data is remarkably consistent across unemployment cycles.

- Average increase in Unemployment from beginning level: 2%

- Average time from trough to peak in Unemployment: 36 months

- Unemployment is currently 0.7 above its trough value. If this were to hold, it would be the first time in the last 50 years that Unemployment didn’t continue to move higher.

For more news, information, and analysis, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All