The Case for Recalibrating Rates Gets a Winning Streak

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThought to ponder…

“Everything can be taken from a man but one thing: the last of the human freedoms—to choose one’s attitude in any given set of circumstances, to choose one’s own way.”

-- Victor Frankl, Man's Search for Meaning

The View from 30,000 feet

Putting it all together

- The case for beginning to recalibrate rates in the S. is on a winning streak for getting stronger with each data print.

- Inflation is below the Fed’s year end target and falling

- Unemployment is above the Fed’s year end target and rising

- GDP has grown below the annualized rate the Fed is projecting for 2024 for Q12024 and is projected to for Q22024, and the latest economic data has been riddled with disappointments on the downside, suggesting further downside weakness is probable

- As with the when the Fed decided to beginning their hiking cycle, they waited until they were absolutely sure they had to make a move, and in doing so left themselves open to well founded criticism. They appear to be headed for the same trap as they look to embark on an easing cycle.

- The Fed thinks they have plenty of time because the employment market is still deteriorating at a linear pace, real wages are rising, financial conditions are relatively loose and corporate earnings remain They may be correct that these factors provide for momentum in the economy may allow them time to move slowly while inflation continues to fall toward 2%. However, this is a large risk, because historically the economy tends to look fine, until suddenly it doesn’t.

- Like the old joke goes… What does the window washer say when he’s fallen off the skyscraper as he passes the 5th floor on the way to the ground? Everything looks good from here.

Powell testimony interpreted dovish

- Perhaps the largest central issue facing the Fed today is that they have no defensible Unpredictable data has caught them flatfooted on multiple occasions since the pandemic, so rather than utilize a methodology that allows them to forecast the economy, over the last two and half years, they have focused solely on one side of their mandate (inflation) and proclaimed they are data dependent.

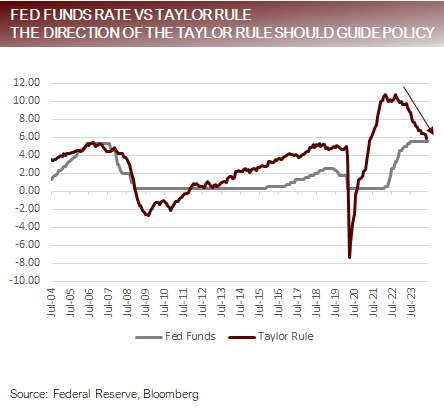

- Powell’s most recent testimony, taken in the context of the recent Fed meeting minutes, indicates a shift to focusing on both sides of their mandate.

- The next step for the Fed will be to re-establish a framework and gain enough confidence to forecasts and set policy. Framework tools, such as the Taylor Rule, which defines targeted Fed Funds based on inflation and GDP, may be far from perfect, but directionally they tells us the Fed is off target.

Cooler CPI sets off everything rally

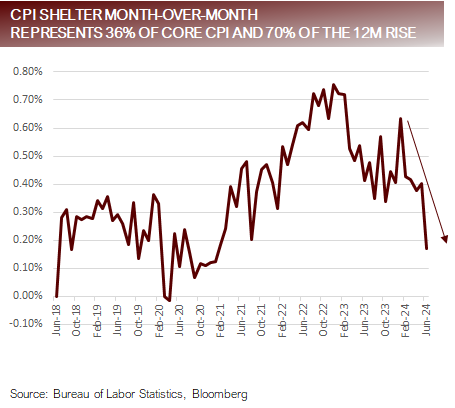

- The bond bulls were vindicated on Thursday when a negative print on Headline CPI provided the first signs of all out deflation (as opposed to disinflation) since the spring of 2020.

- The big story was Shelter, which has been responsible for about 70% of the increase in Core CPI over the last 12-months, only rising 0.17% month-over-month, the smallest monthly increase since January of 2021.

- On Friday, stronger than expected PPI did little to dissuade the bulls, who chose to focus on models that incorporate CPI and PPI data to estimate PCE, the Fed preferred measure of In looking at the models available to us, the range was for month-over-month PCE to be somewhere between -0.5% and 0.15%. The release date is 7/26, and the current average estimate according to Bloomberg’s consensus data is 0.28%, which would imply a large downside miss on PCE.

- Before anyone takes a victory lap on inflation, it should be noted seasonal factors and energy prices point to the current downward trend fizzling out soon.

Inflation expectations falling

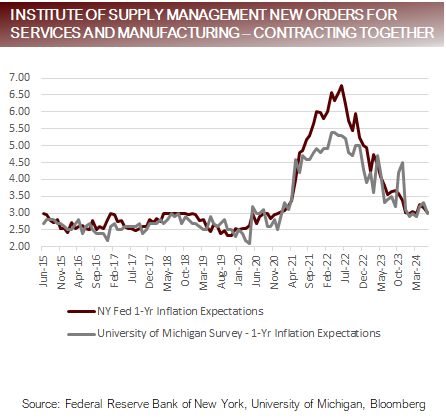

- Average monthly Inflation expectations for the four-years prior to the pandemic:

- NY Fed 1-Yr Inflation Expectations: 2.7%

- Univ of Mich Survey 1-Yr Inflation Expectations: 2.6%

- With both measures currently at 0% and falling, the Fed has little case that inflation expectations are not in check.

- Inflation expectations are just another one of a long list of data that are normalizing, which should lead the Fed to to two things:

- Gain confidence that forecasting tools provide value, rather than being solely data dependent

- Begin a recalibration process towards the neutral rate, which is likely 200 to 250 basis points lower than current levels

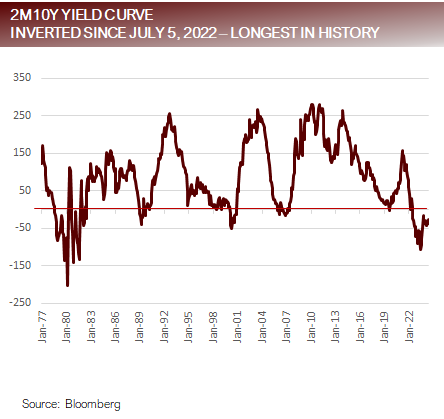

Happy birthday yield curve inversion (2 years and counting)

- The current yield curve inversion is the longest in the history of yield curve inversions, and the second deepest.

- There are a number of arguments as to why the yield curve has been a less reliable indicators of a recession this cycle:

- Central Bank Interventions Influence

- Massive Global Demand for Safe Assets

- Structural Changes in the Economy

- Idiosyncratic Sentiment Related to Post-Pandemic Transitions

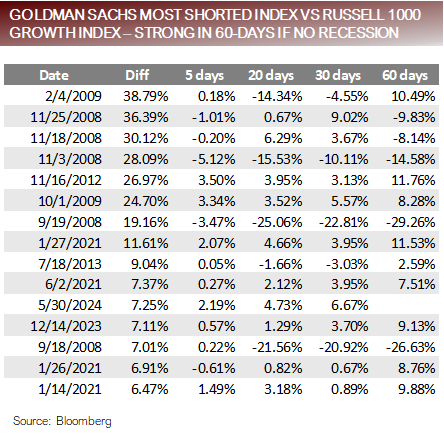

Rotation rally or short covering rally?

- We analyzed the daily dispersion between the Goldman Sachs Most Shorted Index and the Russell 1000 Growth in search of periods where heavily shorted stocks rallied versus market leadership.

- Thursday’s rally was marked the 16th largest dispersion between the Goldman Sachs Most Shorted Index and the Russell 1000 Looking at the other top 15 days we make the follow observations:

- Large dispersion days tend to happen in clusters of two to three within a 30-day window, suggesting that we will see another large dispersion day soon.

- The results can be categorized broadly into periods in, or around, a recession and those where there was not a recession in In the 9 cases out of 15 where there was no recession in sight, the average return of the S&P500 Index 60-days after the dispersion day was 8.9%. Suggesting, if the economy is not in or headed into a recession soon, dispersion days may be an indicator of market strength.

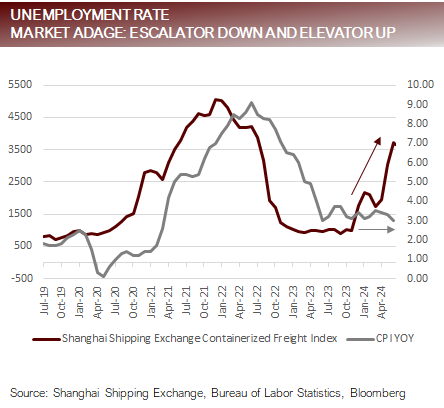

Conversations with clients: Biggest concerns and reasons to be on guard

- During calls with clients last week questions were centered around what kept me up at night and what makes me guarded about continued upside for equity I’ll list a few.

- One of the major drivers of inflation post-pandemic has been identified as supply chain disruptions. As the chart highlights there was a very tight, approximately 1-year lagging, correlation between the Shanghai Shipping Exchange Index, which is a proxy for supply chain disruptions, which rose almost 500% between April 2020 and December 2021, and year-over-year This relationship has broken down as of late, with the former spiking to near pandemic levels, and the later moving sideways.

- One of the common themes from the most recent earnings reports is a loss of pricing power. If real wages continue to grow, without corporate pricing power, margins will come under pressure, which is historically a more challenging time for equity markets

- UBS Chief Economist last week put out a note detailing the impact of washing machine tariffs. A tariff of 50% was placed on washing machines in 2017. Twelve-months later washing machine prices were up approximately 42%. Given some of the policy platforms in the Presidential race in the U.S. involve calls for large tariffs, the table for 2025 may be set for another round of inflation of the policies are implemented.

For more news, information, and strategy, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied.

FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.

A message from Advisor Perspectives and VettaFi: Join us on July 25 for the Q3 Fixed Income Symposium, where advisors will gain insights into essential fixed income strategies and market trends to navigate 2024's challenges.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All