Third Quarter Equity Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Great Lengthening

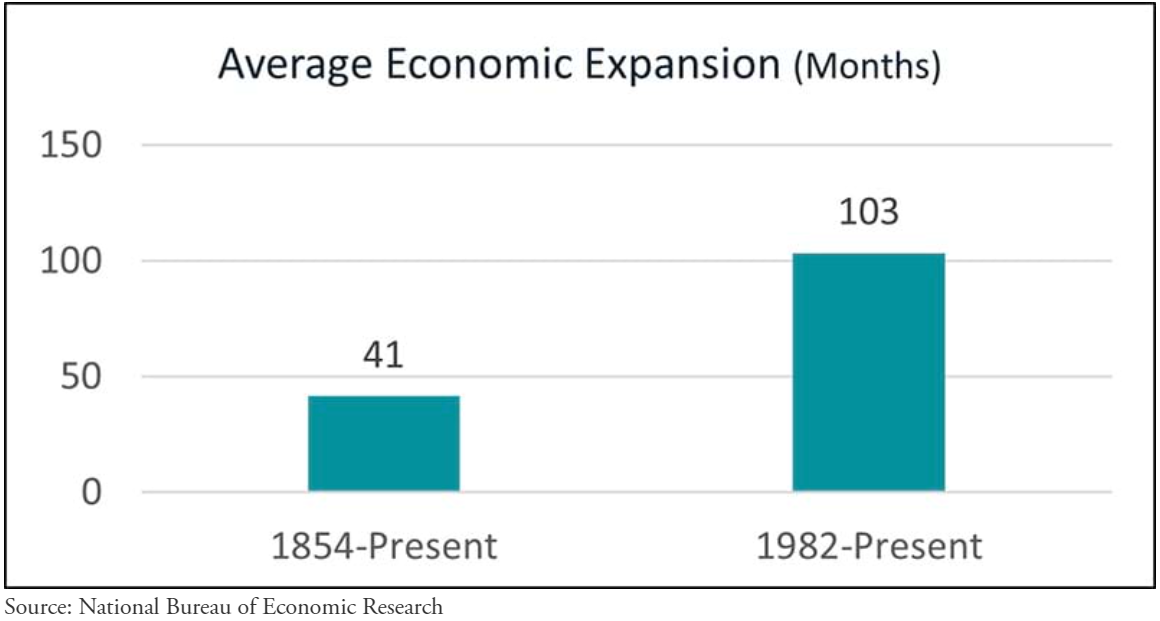

Over the past roughly 40 years, a marked change has crept into the U.S. economy: periods of economic expansion have substantially lengthened. In fact, going all the way back to 1854, the average economic expansion lasted just over 40 months, or roughly three and a half years. However, since 1982, the average economic expansion has lasted over 100 months, or more than eight and a half years. In other words, economic expansions over the past roughly 40 years have more than doubled in length!

It is also worth noting that three of the four longest economic expansions in U.S. history since 1854 all occurred after 1982, again reflecting the fact that economic expansions have significantly lengthened over the past roughly 40 years. And the most recent economic expansion from 2009-2020 was the longest on record, only to be interrupted by the exogenous Covid-19 pandemic.

Why Are Economic Cycles Lengthening?

It is hard to give a precise answer as to why economic cycles have lengthened, but we think there are several potential drivers of this change. A recent study by Deloitte provides helpful historical context for how economic cycles used to play out:

There was a time when levels of inventories…drove the economic cycle. Before the era of cheap computing power, matching inventories to future demand was fiendishly difficult. When demand fell unexpectedly…companies ended up with unwanted inventories. They slashed orders, hitting producers, and reinforcing the downturn. When companies ordered too little, they rushed to restock, fueling demand and inflation. Inventories yoyoed and so did demand.

The same study notes that the Princeton economist and former Vice Chair of the Federal Reserve Alan Blinder “has estimated that in the eight U.S. recessions between 1945 and 1982 falling inventories accounted for a remarkable 87% of the fall in GDP.” In other words, inventory cycles dominated prior economic ups and downs.

However, several structural changes have taken hold across the U.S. economy that have likely dampened the impact of inventory cycles in recent decades:

- Decline of U.S. manufacturing: The manufacturing sector in the U.S. significantly contracted due to offshoring, with manufacturing share of U.S. GDP contracting from 16% to 11% from 1997-2021.

- Rise of the service economy: Capital-light services — including technology, financial services, media, consulting, and healthcare — have driven a wholesale shift in the composition of the economy, leading the services share of U.S. output to grow from 62% in 1980 to 79% in 2020, coinciding with the decline in inventory- and capital-intensive U.S. manufacturing.

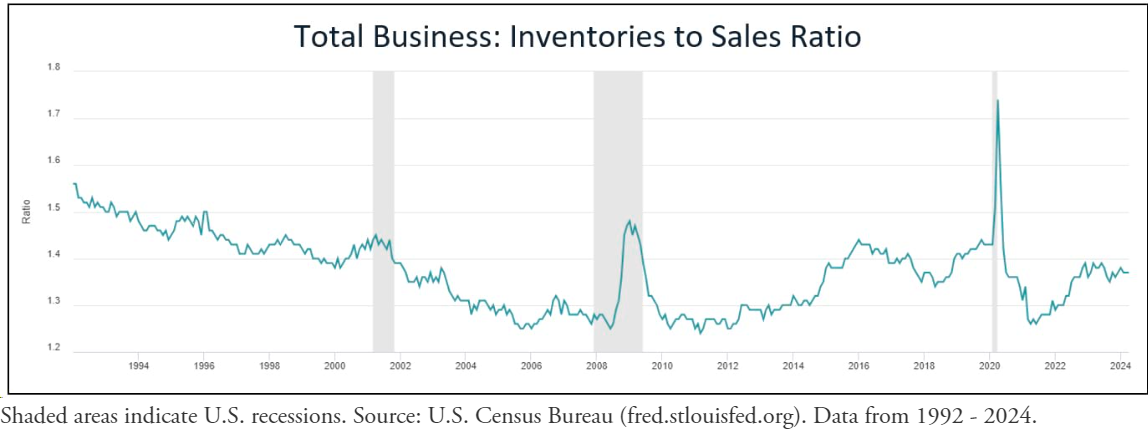

- Efficient supply chains: The combination of offshoring and extensive technological improvements allowed supply chains to move far offshore and much better balance supply with demand, leading to a multi-decade decline in inventory relative to sales as you can see in the chart below.

Persistently low inflation likely helped lengthen cycles even further. Whether due to technology-driven productivity gains, offshoring of both labor and supply chains, or weaker labor unions, lower inflation meant economic cycles could go even longer without being interrupted by higher rates to combat inflation.

So Are Inventory Cycles a Relic of the Past? Not so Fast.

Given the above structural factors, it would seem that we can look forward to long, largely uninterrupted economic cycles. However, there are at least two important caveats to point out: 1) manufacturing and related supply chains are moving closer to the U.S., and 2) technology is becoming more capital-intensive.

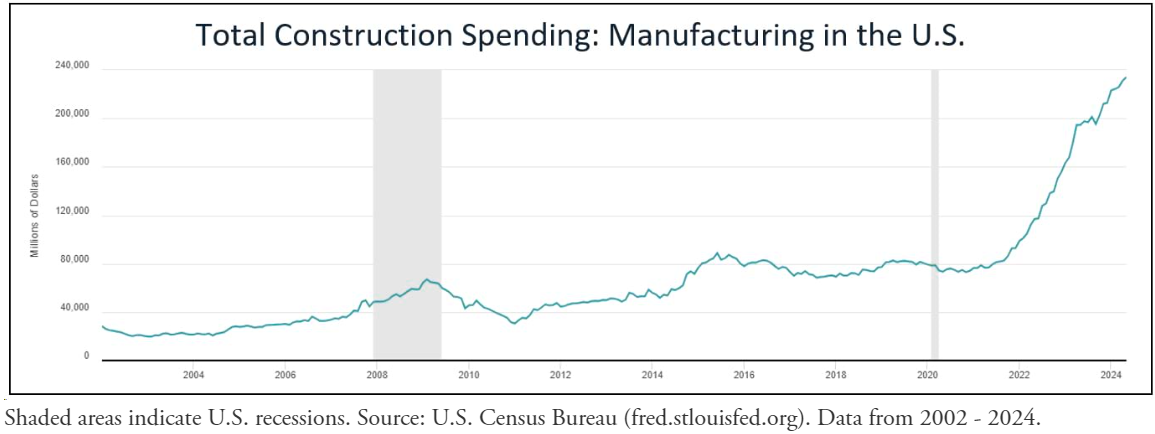

As we have discussed in prior outlooks, manufacturing is coming back to the U.S. In fact, construction spending on manufacturing has moved dramatically higher in recent years.

This increase is likely driven by a raft of recent legislation, namely the Inflation Reduction Act, the CHIPS Act, and the Infrastructure Investment and Jobs Act. These pieces of legislation offer a range of subsidies and incentives for companies investing in domestic infrastructure, semiconductor production, alternative energy, and other key sectors of the domestic economy. A resurgence in domestic manufacturing could at least partially reverse the decades-long de-industrialization of the U.S. economy, thus making inventory cycles more relevant again.

Meanwhile, supply chains are also coming closer to the U.S., as the Covid-19 pandemic and related supply chain disruptions forced many industries to reconsider how they supplied goods. As a result, Mexico has surpassed China as the number one trading partner of the U.S.

The technology industry is also shifting to a more capital-intensive model. Cloud growth has been driving higher capital expenditures (CapEx) among technology companies for years, and the recent surge in spending related to artificial intelligence (AI) means even more data centers are being built in the United States. As a reflection of this shift, Alphabet, Amazon, Meta, and Microsoft have all announced they will increase CapEx from roughly $120 billion in 2023 to what we estimate to be roughly $180 billion in 2024, a 50% increase in just one year starting from an already staggeringly high base.

This spending boom is enabling a massive increase in production of highly specialized semiconductors used for intensive AI computing. Nvidia alone is expected to generate over $160 billion of revenue in calendar year 2024 versus just under $17 billion of revenue in calendar year 2020, a nearly ten-fold increase in four years. While there are clearly massive secular trends driving this growth, semiconductors are a manufacturing-intensive and notoriously cyclical sector with epic inventory swings.

It is also worth noting that inflation may be higher going forward, as near-shoring of supply chains and strengthening labor unions offset some of the tailwinds that enabled low inflation for so long. This could force the Fed to step in more forcefully to periodically raise interest rates, cool down demand, and stave off persistent inflation, as happened with the current interest rate hike cycle starting in March 2022.

The resurgence of U.S. manufacturing, near-shoring of supply chains, and the increasingly capital-intensive nature of the technology sector likely will have favorable implications for the U.S., helping restore manufacturing jobs lost over prior decades (nearly 5 million net jobs lost from 1997-2021) and bolstering supply chains. However, the swing back to inventory- and capital-intensive economic activity could mean that economic cycles over the next couple of decades see more volatility than those of the past four decades.

Back to the Future?

Inventory corrections long played a key role in the U.S. economic cycle, helping enforce a regular cadence of expansion followed by recession in less than four years on average. However, the decline of manufacturing, the offshoring of supply chains, and a shift to a more service-based economy over the past roughly 40 years appear to have reduced the impact of inventory cycles, resulting in longer economic expansions lasting over eight years on average since 1982. The return of domestic manufacturing, near-shoring of supply chains, and increasingly capital-intensive nature of technology companies may reverse some of the key trends that smoothed out the economic cycle in recent years, leading to more cyclicality going forward. Higher inflation going forward could also force the Fed to more consistently raise rates to combat price hikes. In some ways, the economy of the future may look more like that of the past.

Our Approach: Quality Growth

Our approach to equity investing continues to center on owning a concentrated portfolio of quality growth businesses. We define quality growth businesses as companies with three key characteristics: 1) a durable competitive advantage, 2) ability to reinvest to drive attractive growth, and 3) solid management. When we find these businesses at attractive valuations, we seek to purchase them and own them until either the valuation becomes untenable, a better opportunity arises, and/or we decide our initial thesis was incorrect. Over time, we believe this strategy should provide compelling returns, regardless of the nature of the business cycle.

Importantly, we believe rising AI demand is a sustainable trend that has multiple downstream impacts, including continued growth in cloud computing and increased semiconductor demand. We own the key hyperscale cloud providers, all of which also own other dominant and fast-growing technology businesses. And we are playing the semiconductor boom in what we believe to be a more defensive manner, owning key competitors of Nvidia that offer comparable performance at lower prices and highly dominant companies farther up the value chain that help manufacture semiconductors. We also own a critical producer of high-bandwidth memory that works with Nvidia chips to process data more rapidly. We remain vigilant of an ultimate semiconductor correction once the current initial spending spree subsides and believe our semiconductor exposure should provide relative protection during an eventual correction.

We thank you for your continued confidence in our management.

John Osterweis, Founder, Chairman & Co-Chief Investment Officer – Core Equity

Gregory Hermanski, Co-Chief Investment Officer – Core Equity

Nael Fakhry, Co-Chief Investment Officer – Core Equity

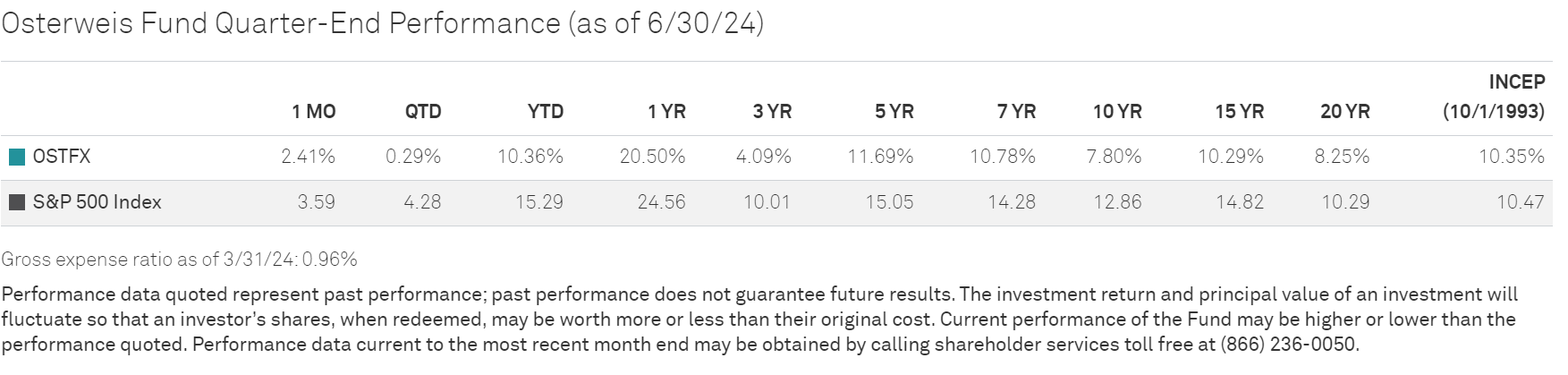

Rates of return for periods greater than one year are annualized.

Where applicable, charts illustrating the performance of a hypothetical $10,000 investment made at a Fund’s inception assume the reinvestment of dividends and capital gains, but do not reflect the effect of any applicable sales charge or redemption fees. Such charts do not imply any future performance. During the period noted, fee waivers or expense reimbursements were in effect for the Osterweis Fund.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large cap U.S. stock market performance. The index does not incur expenses, is not available for investment, and includes the reinvestment of dividends.

References to specific companies, market sectors, or investment themes herein do not constitute recommendations to buy or sell any particular securities.

There can be no assurance that any specific security, strategy, or product referenced directly or indirectly in this commentary will be profitable in the future or suitable for your financial circumstances. Due to various factors, including changes to market conditions and/or applicable laws, this content may no longer reflect our current advice or opinion. You should not assume any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from Osterweis Capital Management.

Complete holdings of all Osterweis mutual funds (“Funds”) are generally available ten business days following quarter end. Holdings and sector allocations may change at any time due to ongoing portfolio management. Fund holdings as of the most recent quarter end are available here: Osterweis Fund

As of 6/30/24, the Osterweis Fund did not hold positions in Nvidia or Meta.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period.

The Osterweis Funds are available by prospectus only. The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The summary and statutory prospectuses contain this and other important information about the Funds. You may obtain a summary or statutory prospectus by calling toll free at (866) 236-0050, or by visiting www.osterweis.com/statpro. Please read the prospectus carefully before investing to ensure the Fund is appropriate for your goals and risk tolerance.

Mutual fund investing involves risk. Principal loss is possible.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

Opinions expressed are those of the author, are subject to change at any time, are not guaranteed and should not be considered investment advice.

Osterweis Capital Management is the adviser to the Osterweis Funds, which are distributed by Quasar Distributors, LLC. [OCMI-570877-2024-07-10]

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All