Navigating Earnings Season: From Pricing With Margin

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- Earnings are coming in. Pricing is holding up, and Volumes are making a comeback.

- This combination is driving improved margins—Price AND Margin.

- Price AND Margin is producing better earnings, and that dynamic is sticky and powerful.

Welcome to the blog series “Navigating Earnings Season.” In this series, I dive into the world of earnings reports from major companies, spanning giants like JP Morgan and Pepsi, as well as niche players in various sectors. As the earnings season unfolds, these corporate outlooks offer real-world insights that often contrast sharply with the uncertainty emanating from the Federal Open Market Committee (FOMC).

Every earnings season has its own unique set of expectations and realities. Coming into this earnings season, one of the most intriguing questions was how well the consumer-facing companies would be able to maintain their pricing power. Pricing was the primary driver of the revenue equation for successful companies over the past two years or so. But the new algorithm for success is a bit more complicated than “raise prices by x.” The requirement now is maintaining or expanding pricing less aggressively and recovering lost volumes. More complicated but potentially more rewarding.

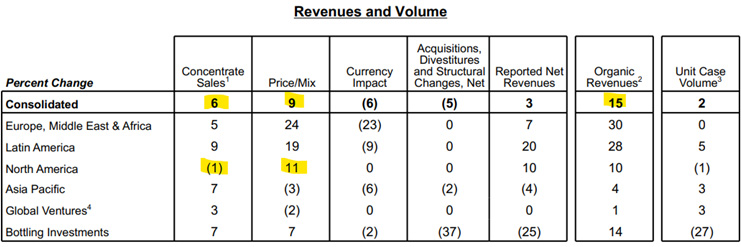

Source: Coca-Cola Second Quarter 2024 Earnings Release, 6/28/24.

Coca-Cola got the memo with a rather significant caveat. Not only did Coca-Cola increase volumes (otherwise known as concentrate sales), but pricing was also a robust 9%. Granted, much of that pricing was generated in places with inflation issues. But—putting that aside—the quarter showed the power of what happens when previous pricing power meets better volumes.

Source: Coca-Cola Second Quarter 2024 Earnings Release, 6/28/24.

The improvement in Coca-Cola’s margins was notable for a couple of reasons. Coca-Cola operates a global business that is—to a degree—at the whim of the strength or weakness of the U.S. dollar. More importantly, there was an uptick in marketing spend. After all, it is difficult to regain volumes without spending some of the pricing-generated margin dollars on marketing. As the U.S. technology platform earnings roll in, it will be interesting to see how the increased marketing spend from the consumer-facing companies has flowed through to “Big Tech.”

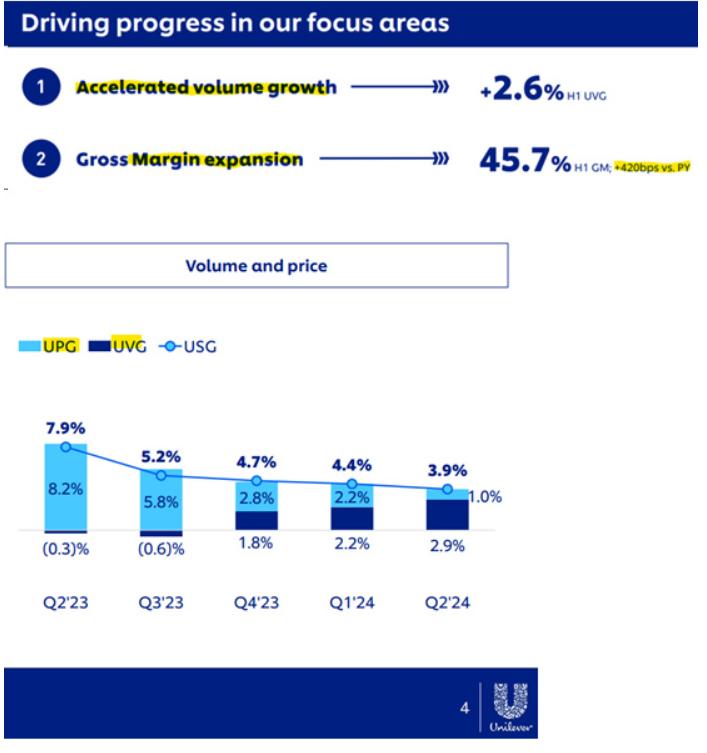

Then there is Unilever (with products from Hellmann’s to Dove soap). Volumes have begun to pick up. Pricing has held up. And margins have expanded. That is the essence of the current environment. Pricing has decelerated meaningfully—from more than 8% to 1% in a year. But that doesn’t matter for bottom-line performance. Previous pricing is today’s margin.

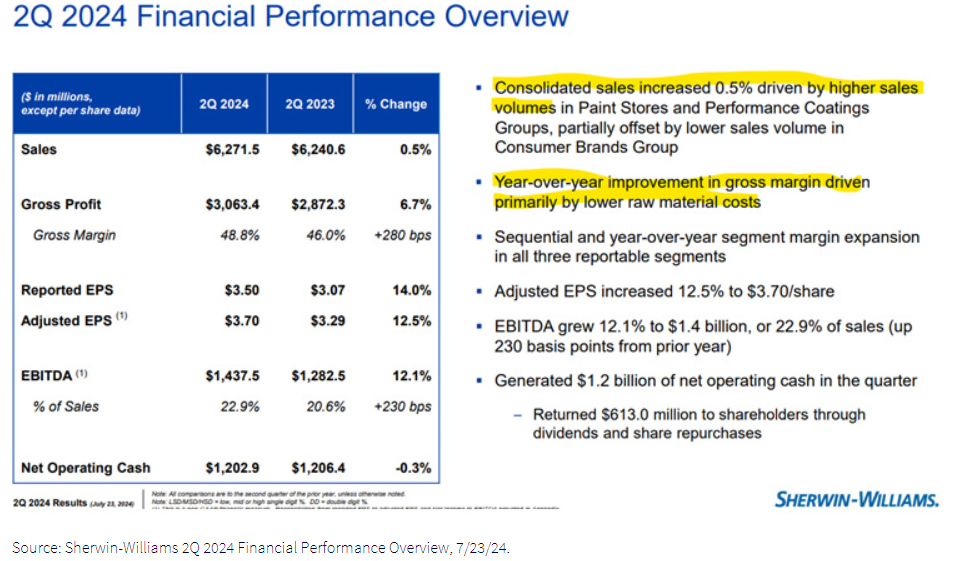

To be clear, this dynamic is not limited to a few companies selling sugary beverages, mayo and soap. The dynamic is also apparent in companies that should be facing significant headwinds. Enter Sherwin-Williams, which—given the rampant headlines surrounding the challenged housing market—should be struggling to generate worthwhile earnings reports. That is not the case.

Sherwin-Williams raised prices as its input costs increased. Then input costs went down, Sherwin-Williams held its pricing, and volumes began to creep back. And this is happening in a low-turnover housing market that has, at best, seen fits and starts. It is worth contemplating what happens if the housing market becomes a tailwind instead of a headwind.

This is why earnings season is always a bit of a “narrative” check. It is easy to get stuck on headlines about a slowing economy, a fading consumer and whatever else might arise. But those broad statements do not (necessarily) equate to the health and trajectory of corporate earnings. Sometimes, the saying “the stock market is not the economy” is worth repeating. This is one of those times.

This article originally appeared on WisdomTree's website and is reprinted on VettaFi | Advisor Perspectives with permission from the author. For more information, please visit WisdomTree.com.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

A message from Advisor Perspectives and VettaFi: Here is the latest news on the bond market, interest rates, and other fixed income sectors.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All