For years, the emphasis within fixed income investing has been to seek security-specific alpha in an illiquid bond market where no single security significantly impacts portfolio returns. This was likely due to the favorable secular macro backdrop of falling interest rates. But as we have experienced in recent years, that macro backdrop has changed, and so too should fixed income investing.

The bulk of fixed income returns can be explained through two macro drivers: credit exposure and interest rates exposure. For each of these return drivers, investors must make critical decisions around allocation (how much exposure) and selection (how you get those exposures), depending on the macro backdrop.

When underlying cash flows (profits in the case of corporate bonds) are improving and spreads are wide, investors should want higher credit allocations. And when they are falling, and spreads are tight, lower allocations. Similarly, investors should want lower interest rate allocations (duration) when interest rates are rising (when growth and/or inflation are accelerating) and higher allocations when interest rates are falling.

Today’s fixed income investors are faced with two dilemmas:

-

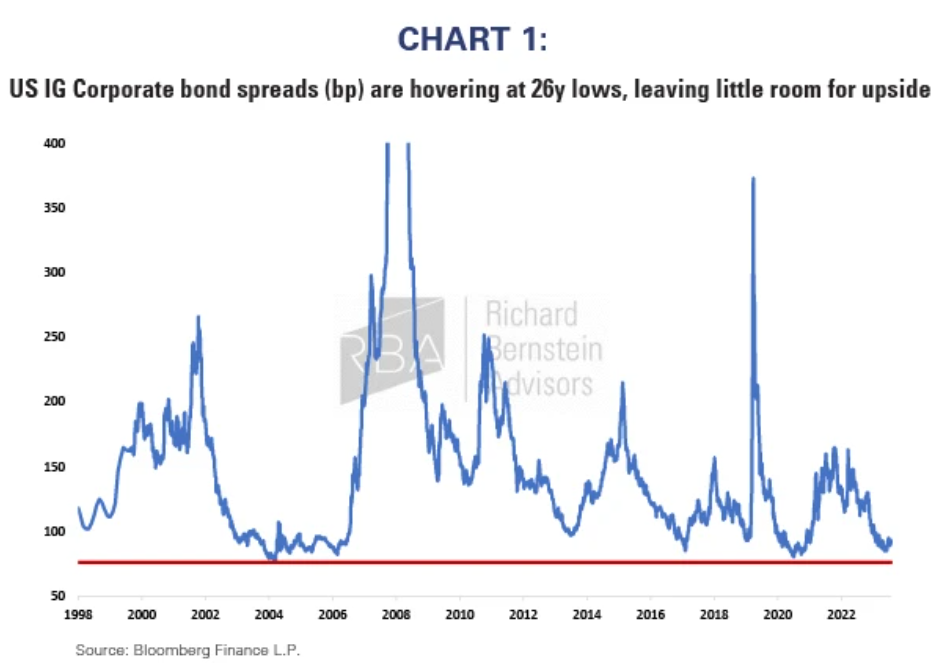

Because corporate profit growth has been so strong, fixed rate corporate bond spreads are historically tight, which creates little opportunity from an overweight allocation. (Chart 1)

-

Interest rates may be rangebound due to (1) unclear economic growth, (2) a potential Fed cutting cycle and (3) structurally sticky inflation. (Chart 2)

Until this dynamic changes, traditional allocation opportunities within fixed income appear somewhat limited. So, what is an investor to do? This is where selection comes into play. Through the optimization of interest rate and credit risk, as well as by leveraging investments outside the conventional Bloomberg Aggregate Index, we have identified three attractive ways to take advantage of credit and duration selection opportunities:

-

Gain exposure to healthy corporate profit growth and higher yields through BBB CLOs. BBB CLOs have default risk of single-A corporates but are relatively cheap and deliver the potential for both income and price appreciation.

-

Get interest rate exposure where income is highest. By owning the long end and the short end (the two highest yielding parts of the treasury curve) simultaneously, we can maximize yield without taking too much or too little duration.

-

Position for further curve steepening. We believe yield curve normalization over time will generate alpha – either as the Fed cuts interest rates, sending the curve steeper – or as inflation accelerates, sending the curve steeper. By owning steepeners through Exchange Traded Funds (“ETFs”) that utilize options, we can also capture an increase in volatility.

Today is a time where emphasizing selection within fixed income is necessary to capture alpha. Eventually, when spreads widen and economic growth begins to break one way or the other, we anticipate that our return will increasingly stem from sector allocation decisions. Until that time, however, fixed income portfolios need to be nimble and creative to weather what could be a tricky second half of 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors