The Current Vibe

Housing and Rents

Multiple Head Fakes

“We Want to be Absolutely Sure…”

Hurricanes and Family

In basketball and other sports, a “head fake” means the player moves their head as if they are about to turn left or right, but then doesn’t do so. This can fool an opposing player into moving the wrong way.

Head fake is a trading term, too. Some bit of information convinces investors a market is going to move a certain way. They reposition their portfolios accordingly… just in time to find out the information was wrong. Oof.

Market head fakes are sometimes intentional, as when a company tries to release news in a way that punishes short sellers. But more often, they’re just part of the fabric of the markets—a thread spun by the mythical Greek Fates which gets pulled and the tapestry that traders thought they saw changes before their eyes. No one knows the future. We can try to guess the odds but sometimes we’ll be surprised.

Today we are in another such position. Everyone thinks the Fed will cut rates next month in response to better inflation data and higher unemployment. And they might, but the market’s certainty about it is not unlike the certainty late last year that there would be six rate cuts in 2024. Those were indeed head fakes. And now…?

The Current Vibe

Going into the week, the case for a Fed loosening seemed pretty strong. Recent inflation data was starting to get within shouting distance of the Fed’s target. Unemployment hit 4.3% in July as job growth continued to soften, a 7-year high, taking out the COVID collapse. We’ve seen some short but serious market volatility episodes, suggesting Wall Street is getting more nervous. As always, you can find data points disputing all this. But that’s the current vibe.

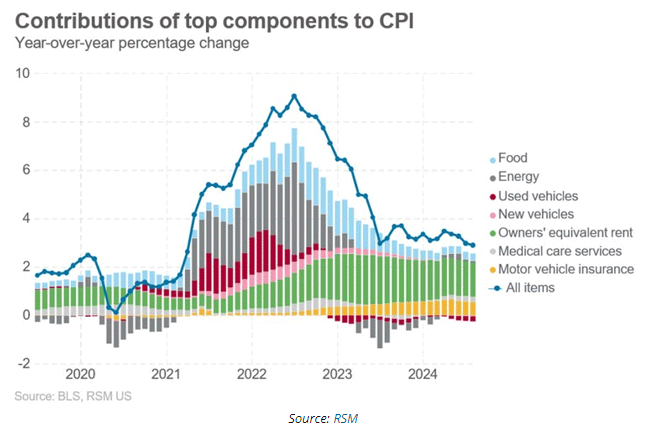

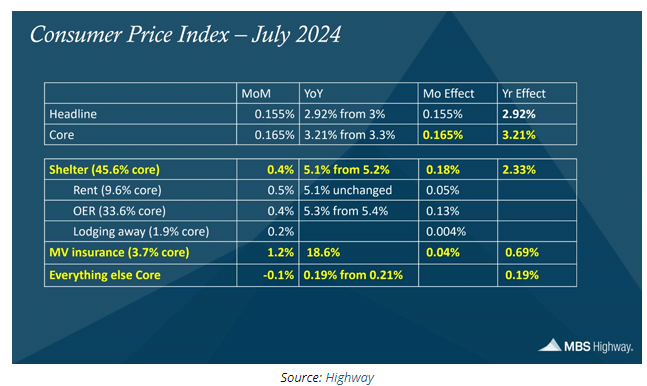

Then this week we got July data for the Producer Price Index and Consumer Price Index, both of which again looked comforting. As I said a few weeks ago (see Going, Not Gone), the remaining inflation is almost entirely in services, mainly housing but also healthcare and insurance. Goods prices are becoming disinflationary as supply chains continue unsnarling and consumer sentiment normalizes from the post-COVID enthusiasm.

This is good news overall, but I don’t want to diminish the seriousness of high housing prices. It touches almost everyone and for most is the single largest living expense. A slower growth rate helps, but the rapid increases of the last few years haven’t reversed.

There are signs of moderation, though. Zillow reported last week that one-third of apartment listings are offering “concessions” like a period of free rent, free parking, etc. That’s not the same as lower base rent, of course, but it’s a step in that direction. Zillow Chief Economist Skylar Olsen sounded optimistic.

“Rents are still growing, but it's a far cry from the steep rent hikes of two or three years ago, and renters will find sweeteners being offered by more than half of rentals in some places. A slowing job market and lower mortgage rates could mean falling rents if the current trends hold."

Both supply and demand are at work here. Many areas have seen a lot of new multifamily construction which is beginning to hit the market. And as Olsen notes, a slowing job market probably deters some people from paying higher rents. Further job weakness, and certainly an outright recession, would hit apartment demand even more.

Here’s an amazing stat from Zillow: Average multifamily rent rose a total of 22.3% from July 2020 to July 2022. Then in the next two years (July 2022-July 2024) it rose only 5.1%. That’s national data and your mileage may vary. But it seems clear the worst of the rent increases are over.

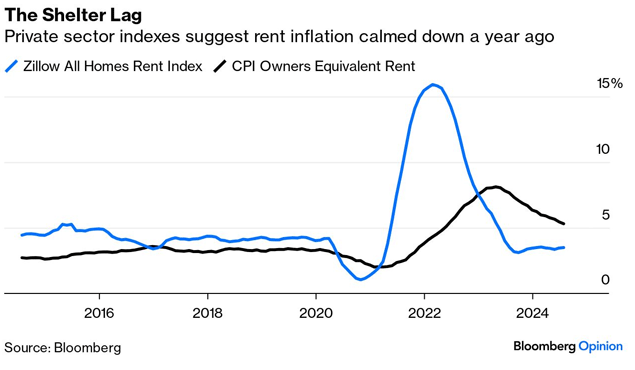

In fact, Zillow tells us this week that month-over-month and year-over-year median rent fell $30 and $25 respectively (source: US Rental Market Summary | Zillow Rental Manager). The measure of home prices used to calculate CPI, called Owners’ Equivalent Rent, says rents rose nationwide by 0.4%.

Both supply and demand are at work here. Many areas have seen a lot of new multifamily construction which is beginning to hit the market. And as Olsen notes, a slowing job market probably deters some people from paying higher rents. Further job weakness, and certainly an outright recession, would hit apartment demand even more.

Here’s an amazing stat from Zillow: Average multifamily rent rose a total of 22.3% from July 2020 to July 2022. Then in the next two years (July 2022-July 2024) it rose only 5.1%. That’s national data and your mileage may vary. But it seems clear the worst of the rent increases are over.

In fact, Zillow tells us this week that month-over-month and year-over-year median rent fell $30 and $25 respectively (source: US Rental Market Summary | Zillow Rental Manager). The measure of home prices used to calculate CPI, called Owners’ Equivalent Rent, says rents rose nationwide by 0.4%.

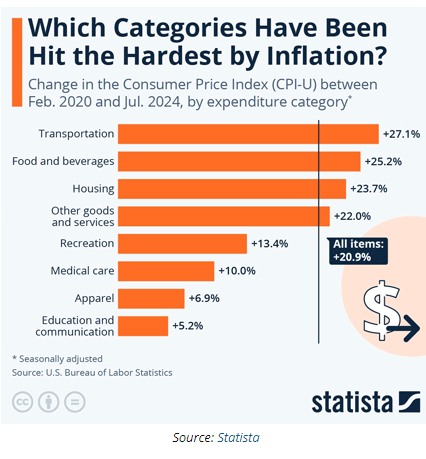

One more data point I have brought up before bears repeating. Right now there is one side of the political spectrum that argues inflation is coming down and people should be happy. And it is coming down. But small businesses still say inflation is one of their biggest problems, especially in labor costs. And consumers don't see the month-to-month changes but they do see the year-over-year changes. And they feel the changes since 2020, which this chart from Statista illustrates.

By the way, a laugh-out-loud comment on the CPI came from my friend David Bahnsen:

My favorite highlight is that “eating at home” prices are up 1% on the year, whereas restaurants are up 4.1% on the year, and I suppose that either speaks to corporate greed with restaurants but not grocers, OR people perhaps liking a professional chef’s cooking more than [a] beloved spouse’s. Eggs were up +5.5% while cereal and bakery items were down -0.5% on the year. Here, I assume it is because egg producers are greedy while cereal producers are benevolent. The only other idea I can come up with is that markets and prices are dynamic and signify lots of different time and place circumstances that politicians, all these decades later, still don’t understand.

Housing and Rents

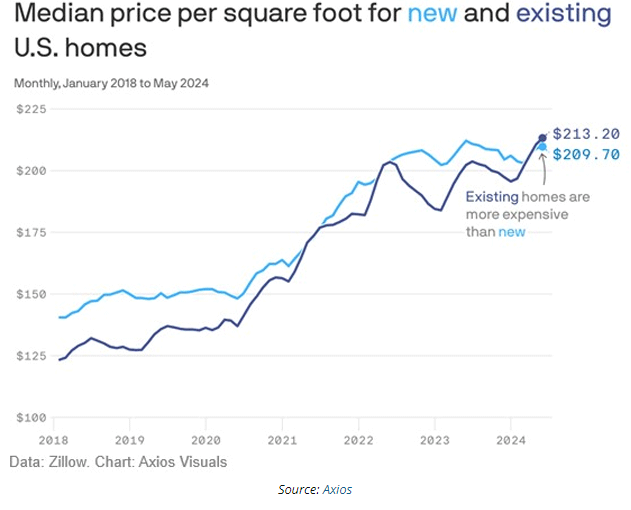

We see a different dynamic in single-family homes. High mortgage rates are still a barrier, not just for buyers but also sellers who (quite reasonably) want a premium price if they must give up their current low-rate fixed mortgage. This is keeping prices stubbornly high for existing homes. And, thanks to the NIMBY people who prevent development, existing homes are often the only option in the most desirable areas.

We have a new twist, though. The median price per square foot for new homes recently dropped below that of existing homes for the first time in years. Again, lots of local variation. But this might suggest developers are responding to demand by building smaller, more affordable homes. And note that new home prices are basically flat on the year, and not the almost 5% that is in the OER.

This will take a long time to feed into the Owners’ Equivalent Rent figures, and thus CPI. The bigger picture is that home prices are still rising faster than wages for many people. Nonetheless, it’s not quite as bad as it was.

All this points to the Fed cutting rates at the September 18 meeting. But we’ll also have another month’s worth of data by then. Could this be another head fake?

Multiple Head Fakes

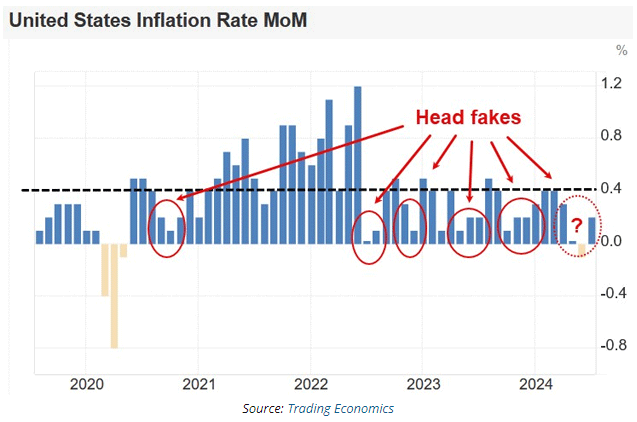

Most people look at inflation as an annual rate. The problem there is that half your data comes from 6‒12 months ago and doesn’t necessarily reflect what’s happening now. The annual rate gives last month’s data the same weight as what happened a year ago.

You can also look only at the latest month, meaning you have the freshest data. You miss some context, but this can be useful for some purposes. And right now, we have one.

The bar chart below shows month-over-month inflation for the last five years. You can see it varies a lot. The dashed line at 0.4% is my arbitrary dividing point between optimism and pessimism. Of course, any inflation is a problem. Above the line is where we should start getting very concerned, and eventually alarmed.

You can see how monthly inflation went deeply negative as COVID struck in 2020. It popped higher as stimulus funds began to boost spending. Then it fell again, rose again, and rose much more into 2022.

The red circles mark periods in this cycle when monthly inflation dropped below 0.4% for two or more consecutive months. It’s happened six times since the pandemic. In the first five instances, it moved back up to our worry line in four months, at most.

That four-month stretch in late 2023 precipitated the wide assumption of several rate cuts this year, and then great disappointment when it didn’t happen.

This is what I mean by “head fake.” We have multiple recent examples of CPI seeming to moderate, only to head higher again.

Will this time be different? Maybe. The April-July moderation does indeed look better than the others. The last 0.5% print was almost a year ago. We have a month of actual disinflation plus two more mild increases. It really does look good.

But a skilled player’s head fakes always look good. And this economy is definitely a skilled player. One of my old mentors repeatedly told me that the market will do whatever it can to cause traders to lose the most money they can.

“We Want to be Absolutely Sure…”

The next CPI report, covering August, comes out on September 11, a week before the FOMC announcement. It will show one of two things:

- A fifth straight month of mild inflation, something we haven’t seen since 2020; or

- A pop higher, suggesting the recent data may be another head fake.

The FOMC looks at a lot of other data. But the members also know CPI readings affect inflation expectations. A hotter CPI would certainly concern them.

Back in March, as the last head fake became evident, I quoted Atlanta Fed President Raphael Bostic (see Higher for Longer?). At the time he was unconvinced inflation was in the range to justify rate cuts. He also raised another point that’s worth repeating now. Here it is again (emphasis mine).

“As my staff and I have talked to business decision-makers in recent weeks, the theme we've heard rings of expectant optimism. Despite business activity broadly moderating, firms are not distressed. Instead, many executives tell us they are on pause, ready to deploy assets and ramp up hiring when the time is right.

“I asked one gathering of business leaders if they were ready to pounce at the first hint of an interest rate cut. The response was an overwhelming ‘yes.’

“If that scenario were to unfold on a large scale, it holds the potential to unleash a burst of new demand that could reverse the progress toward rebalancing supply and demand. That would create upward pressure on prices. This threat of what I'll call pent-up exuberance is a new upside risk that I think bears scrutiny in coming months.”

Again, that was Bostic speaking last March. Now, with four months of softer inflation, markets are convinced rate cuts are imminent. Do we see the kind of “pent-up exuberance” he feared?

Here’s one. The NFIB Small Business Optimism Index rose in July to its highest reading since February 2022. Small business owners still describe inflation as their top challenge. But they’re also confident enough to invest in inventory, make capital outlays, and raise selling prices.

That’s only one data point, and it’s from survey data with all the usual limitations. But just looking around, it’s not hard to find people who are pretty excited about rate cuts. Markets certainly are.

Bostic is paying attention. He said this week he wants to see “a little more data” to be sure inflation is heading toward their target before he will support lower rates. He specifically noted this:

“We want to be absolutely sure… It would be really bad if we started cutting rates, and we had to turn around and raise them again.”

Bostic said that before the latest CPI data, so maybe he’s more confident now. “Absolutely sure” is a high bar. I think he’s telling us not to assume rate cuts are a done deal.

There’s another question: Even if they do cut rates next month, what will be the effect? Their tighter policy took a long time to cool the economy. It’s fair to wonder how long looser policy will take to stimulate it.

Keep in mind that the federal funds rate isn’t the Fed’s only tool. Balance sheet activity is equally and maybe more important. Quantitative tightening (QT) is still happening, at a reduced pace of $45 billion a month, or $540 billion yearly. My friends at Gavekal estimate the Fed will need about two more years of QT at this pace to restore reserve assets to their desired level. It might be as little as 17 months under different assumptions. The QT schedule could change any time, of course. But continuing to shrink the balance sheet certainly reduces the stimulative effects of rate cuts.

Employment data is important, too. It is the other half of the Fed’s dual mandate. Their duty is to maintain price stability and full employment. Other than housing, price stability seems nearly if not already in hand. Full employment was at hand but is now starting to slip away.

But here again, the unemployment rate isn’t the only benchmark. It has been rising but mainly due to workforce growth, not job losses. The workforce can’t grow indefinitely and could even shrink, which would bring the unemployment rate back down. Many employers still report great difficulty finding help. That could change in a severe recession scenario that slashes consumer demand. Hopefully we can avoid that.

From the FOMC’s perspective, I think inflation data is far more important than jobs data right now, unless the jobs data gets a lot worse. The next touchstones are the PCE release on August 30 and CPI on September 11. In between will be the August jobs report on September 6.

Keep in mind, too, the data-dependent Fed doesn’t want to surprise markets. They say they haven’t made up their minds and I believe them. But they’ll start forming conclusions as the meeting draws near. If they start to believe the markets are getting it wrong, they’ll find ways to “guide” our thinking.

Another reason to think about a head fake is that even if we do get a rate cut in September, and another one later this year, it will still have the fed fund rate at 5%. The two-year note has been bouncing around 4%. The one-year is at roughly 4.5%. Let's think about that for a second.

Even if the Fed gives us six rate cuts over the next 24 months, you would be somewhat better off simply rolling your cash over in three-month T-bills. The bond market appears to me to be pricing in a recession. And one that will give us more than six rate cuts.

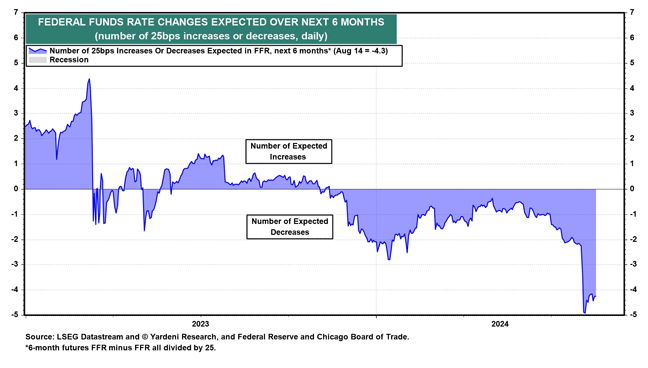

Ed Yardeni offers this observation: The market is expecting 4‒5 rate cuts over the next six months.

Quoting:

“We continue to expect the Fed will cut the federal funds rate (FFR) by 25bps in September. That may be their only cut this year, too. Market expectations for 100+ bps of rate cuts over the next 6 months are overdone, as they were at the start of the year (chart). We remain in the one-and-done camp for the remainder of 2024.”

Consumer spending is solid. Continuing unemployment claims are down somewhat. Earnings season supports the thesis that the consumer is alive and well. And while illegal immigration is a controversial topic, I don't think it's all that radical to suggest that immigrants of any type have to eat food, have shelter, clothing, and other components of consumer spending. The source of that income really doesn't even matter—it is getting spent.

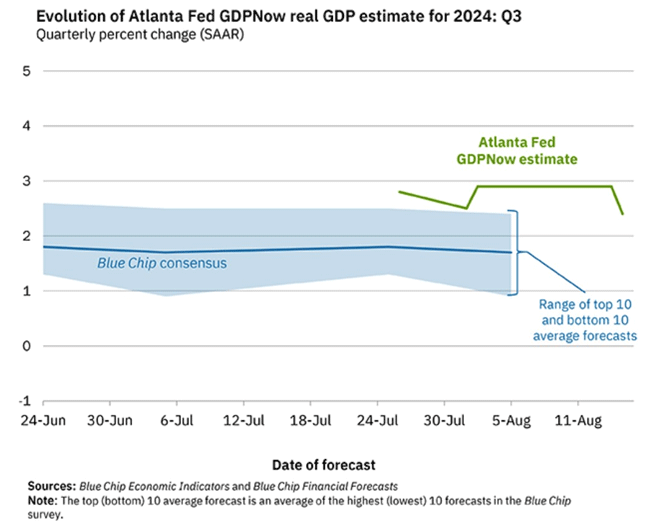

The recession keeps getting postponed. Third-quarter GDP looks likely to be over 2%. The Atlanta Fed GDPNow is 2.4%. The New York Fed’s is 2.2%. That’s not shabby.

A 2% GDP with inflation maybe going closer to 2% in the first quarter might indeed justify fed funds going to 4% during the second quarter. But to 3% which would justify the current 2-year rate? Either inflation has to go a lot lower or GDP goes lower or both.

Since I said earlier this year there would likely be no rate cuts this year, it seems only fair for the market to punish my hubris by giving us a rate cut in September. I am sure it is nothing personal. But a lot of traders are on the other side of that boat. It wouldn’t be the first head fake this cycle. Just saying…

Hurricanes and Family

I was in New York for a pressure-packed three days this week, only to get a text from United Airlines offering to let me postpone my flight for one day as there was “weather” in the Puerto Rico area. A quick look did confirm that a hurricane was due to hit about the time my flight was supposed to land. Having done this drill before, I decided that discretion was the better part of valor and rather than being stuck in New Jersey overnight, I extended my stay and flew home to beautiful skies on Thursday.

While I was sitting on the plane I got a text from my daughter Amanda telling me that her twin sister Abbi was on the treadmill at 5:00 am and had a seizure, fell and hit her head and they had to revive her before taking her to the hospital. They moved her to a major hospital in Tulsa, put her in the ICU, did a scan and found a tumor, and she is in a medically induced coma as I write. There is a solid family network around her and I assume we will know more in the next few days but this is not what any parent wants to hear.

And with that, I will hit the send button.

Your pretty sure inflation is not the most important thing on my mind right now analyst,

John Mauldin

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Mauldin Economics

Read more commentaries by Mauldin Economics