Thought to ponder…

“What’s ironic (or perhaps natural) is that research tells us that we judge people in areas where we’re vulnerable to shame, especially picking folks who are doing worse than we’re doing. If I feel good about my parenting, I have no interest in judging other people’s choices. If I feel good about my body, I don’t go around making fun of other people’s weight or appearance. We’re hard on each other because we’re using each other as a launching pad out of our own perceived shaming deficiency.”

-Brené Brown, Daring Greatly

The View from 30,000 feet

Putting it all together

- After market expectations spiked to nearly five interest rate cuts in 2024 based on disappointing labor market report early in the month, reassuring data in the form of Retail Sales and Unemployment Claims have quelled market Markets have eased expectations for interest rate cuts, pricing closer to four cuts as of the end of last week. Given that there are only three meetings between now and the end of the year, that would suggest one supersized 50 basis point cut, which underscores market nervousness about employment.

- The consensus view is that Fed policy is restrictive, and the Fed will embark on an interest rate cutting campaign beginning in September. The central question is the move to normalization going to be a recalibration of rates to neutral or does it need to be a more aggressive shift towards accommodation to head off a looming non-linear slowdown brewing in the labor markets?

- We’re in the “need to see the whites of their eyes” Meaning, that for us to be convinced that the U.S. is going to move into a recession we are looking for continued weakening in leading economic data combined with validation from coincident data to support a view that significant market downside has a high probability.

- As for Fed policy, we are not quite as exuberant as the market view and circle back to the June Federal Reserve Summary of Economic Projections, noting that the 2025 yearend estimates were Unemployment of 2%, Core PCE of 2.3% and Fed Funds of 4.1%. Currently Unemployment is 4.3%, the August 30 Core PCE Projection is 2.7% and Fed Funds Upper Bound is 5.5%. This puts the Fed in a tough spot because Unemployment is already through their target, but Core PCE has some ground to make up, suggesting the Fed will likely move but may move cautiously.

NFIB Small Business survey results

- The biggest take-aways from the NFIB Small Business Survey last week were:

- Fewer businesses raised prices in July, with 22% reporting higher prices, down 5 points than June, with plans to raise prices in the future also decreasing.

- Compensation increases were also less frequent, with 33% of businesses raising wages, 5 points lower than June.

- Meanwhile, Future Sales Expectations increased 4 points to the highest level in 2024.

- The NFIB Small Business Uncertainty Index surged to 90.0, the highest level since the depths of 2020.

- The details of the report support a narrative that inflationary pressures are easing, growth expectations are holding up, but businesses are anxious about conditions These conditions support the market view that the Fed will begin cutting rates in September.

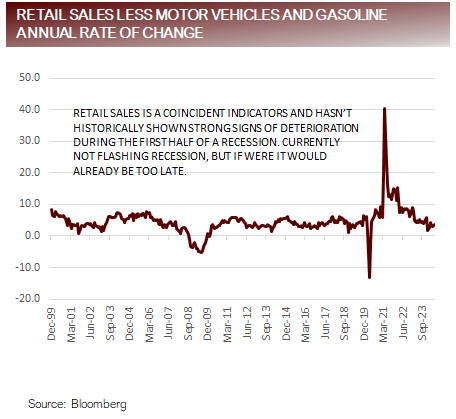

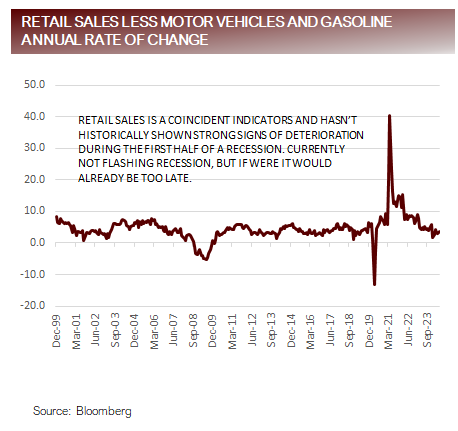

Retail Sales surprise on the upside

- Retail Sales absolutely crushed expectations, rising by 1.0% versus the median survey of 4%. As many data releases since the pandemic have done, the change was outside the range of Bloomberg surveyed economist expectations.

- Much of the spike in Retail Sales was driven by the resolution of the software problems at auto dealerships caused by the cyberattack the previous month, increased nominal sales due to higher gasoline prices and back to school spending. Stripping out the volatile components by looking at the Retail Sales Control Group, the data were a little less eye popping, coming in at 0.3% versus an estimate of 1%, and actually in the economist’s range of estimates.

- The stock market response to Retail Sales was the real story of the data release. The S&P500 popped 1.61%, and Consumer Discretionary rose 3.19% on the day, the largest one-day gain for the sector in 2024.

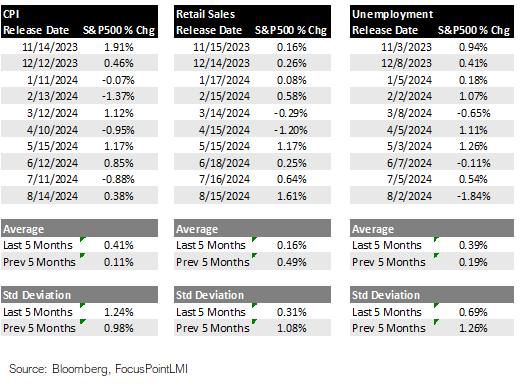

Growth data takes over the podium

- The tables to right show the data release dates and daily performance for CPI, Retail Sales and Unemployment. Some key points to note:

- Market volatility related to inflation data has cooled. In the last five months the average size of the daily change of the S&P500 and volatility of the S&P500 has decreased on CPI days relative to the previous five months

- Market volatility related to growth data has increased. In the past five months market volatility on data release dates for Retail Sales and Unemployment have moved two to three times higher.

- Market reactions, measured by the daily moves in the S&P500 on release dates, looks like a shadow of Fed remarks, tracking the shift in Fed rhetoric towards concern about growth versus inflation.

Searching for signs of a material slowing in the coincident hard data

- Evaluating key measures of coincident data, there are few signals of a material slowdown brewing. This can be deceptive because coincident data is merely a snapshot of current conditions. However, a falloff in coincident data acts as a validation to signals contained in leading indicators. Given that many of the leading indicators have been less accurate than normal this cycle, due to the size of fiscal and monetary policies and programs and unusual inflationary impacts, there is an increased reliance and importance for coincident data as a validating tool. Below is a short list of the coincident data we monitor, for signals of material weakness. There has yet to be a breakdown in coincident data.

- GDPNow (Atlanta Fed ,NY Fed, St. Louis Fed, Bloomberg)

- Dallas Fed Weekly Activity Index

- Conference Board Coincident Indicators

- Retail Sales

- U.S. Port Activity

- S&P500 Earnings Revisions Trends

- S&P500 Operating Margin Trends

For more news, information, and analysis, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by VettaFi