Volatility Cocktail

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThought to ponder…

“It’s one thing to not be overwhelmed by obstacles, or discouraged or upset by them. This is something that few are able to do. But after you have controlled your emotions, and you can see objectively and stand steadily, the next step becomes possible: a mental flip, so you’re looking not at the obstacle but at the opportunity within it.”

-- Ryan Holiday, "The Obstacle Is the Way"

The View from 30,000 feet

Putting it all together

- Looking past November is like peering into a thick fog. Things we know:

- Between now and the election the Fed will be cutting rates.

- The economy is currently humming along at or above potential growth.

- There are signs that the labor markets are deteriorating faster than the Fed was anticipating, while disinflationary forces seem rooted, allowing the Fed to lean dovish.

- Things we don’t know:

- The Fed’s forecast past election. This is because depending on who wins the election, Federal Reserve Policy may need to be very different.

- This dynamic has created a very short-sighted Fed, who continues to focus on the next piece of data being released rather than venturing to put forward a forecast, creating the potential for extreme bouts of volatility surrounded economic data releases.

- We remain constructive on risk-assets but are becoming more guarded based on deteriorating labor markets, stretched consumer and potential for election uncertainty sending money to the sidelines to wait out the outcome. Compounding our increased attentiveness to risk are seasonal patterns which indicate we are entering the most tricky time of the year.

Reviewing the Fed’s yardstick

- The Fed updates their Summary of Economic Projections four times a year. The last update was in June, when they projected at the end of 2024 the Unemployment Rate was going to be 4.0% and Core PCE was going to be 2.6%. The two combining to result in a Fed Funds Rate of 5.1%. With the release of Friday’s Core PCE, we are now are at the projection Core PCE at yearend and +0.3% over on the Unemployment Rate, which is above their peak 2025 projection and for the cycle.

- If we were to hold the Fed to their projections, the appropriate Fed Funds rate today would be somewhere significantly south of 5.1%, suggesting rates should be moving lower, likely by 50 basis point in September.

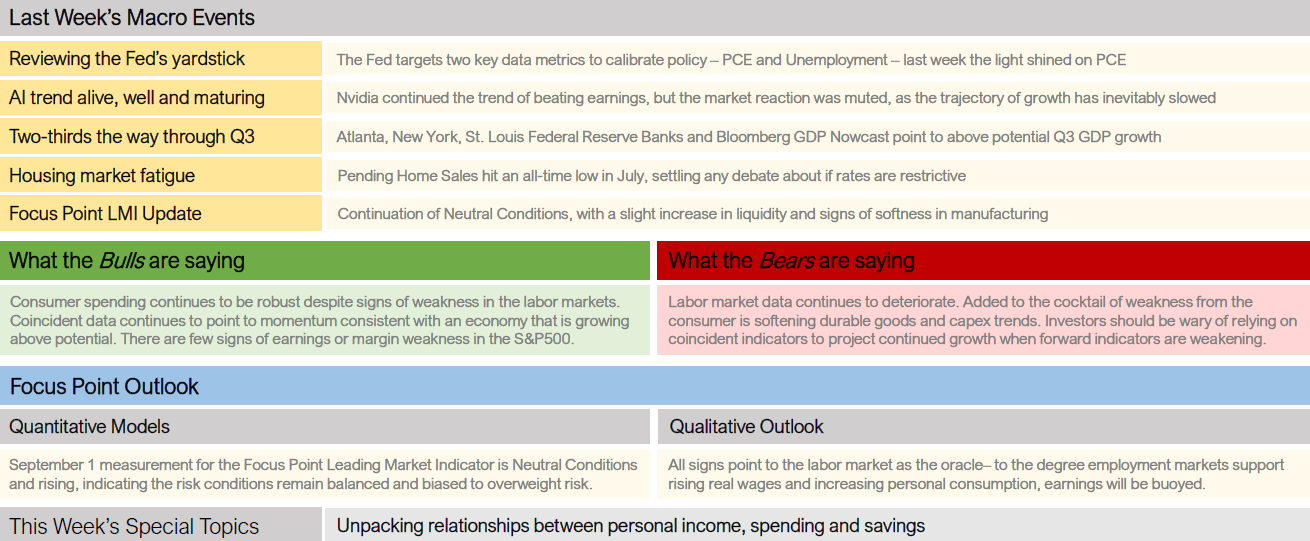

- Because PCE can be mostly constructed using components of CPI and PPI released earlier in the month, no one was surprised to see the PCE level. However, what was surprising was consumer spending and consumption data released that indicated Q3 is on track to print above potential GDP.

AI trend alive, well and maturing

- The markets went to the doctor and had a check-up on the AI story on Wednesday night when Nvidia reported. Although Nvidia beat numbers across the board, the paltry 122% growth over the last year was not enough to satisfy investor lusts, who have gotten used to seeing over 200% year-over-year growth reported each quarter.

- Despite the muted market response to Nvidia’s earnings, the projections for growth for AI infrastructure continues to be insatiable, all be at a slower pace. According to S&P Global:

- Global AI spending will grow nearly 30% a year through 2028. Between now and then, AI spending will grow from 6% of global IT spending to 14% of global IT spending.

- Hyperscaler spending on AI equipment was recently revised from roughly 30% a year to over 40% a year.

- With increased competition and the hyperscalers working to create chipsets of their own, it’s inevitable that Nvidia’s torrid pace of growth will slow, but the expansion of the AI movement is nothing short of alive and well.

Two-thirds the way through Q3

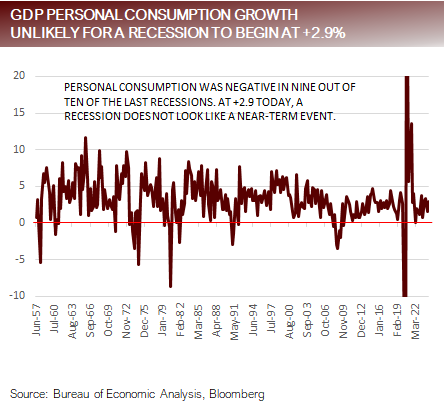

- Looking at the four GDP Nowcast measures we follow as signals of coincident indicators, there are few signs of a recession in Q3. Two-thirds of the way through Q3 GDP Nowcast models are consistent and all show above potential growth:

- Atlanta Fed +2.5%

- New York Fed +2.5%

- St. Louis Fed +2.1%

- Bloomberg +2.5%

- GDP Nowcast model are far from perfect. For example, the average difference in actual GDP versus average projections of the four models over the last four quarters underestimated the GDP growth rate by 1.0%.

- The Conference Board Coincident Composite and Dallas Fed Weekly Economic Index are two other measurement of real-time activity that also indicate above trend potential growth.

Housing Market Fatigue

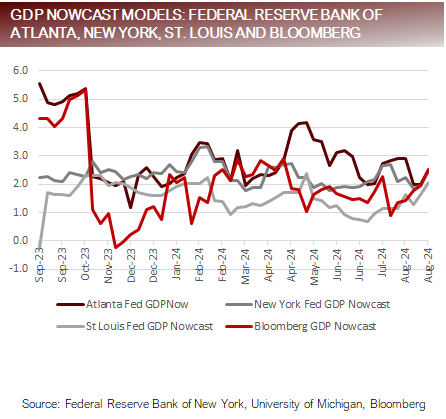

- Pending Home Sales fell last month to an all-time low, while inventory continued to climb and is now at its highest levels since 2020, with active listings up 36.6% year-over-year.

- Active listings are now about 900k, which is off the low in 2022 of about 350k, but still well below the average level in the three years prior to the pandemic, where active listings averaged about 1.2m this time of the year.

- The combination of weak pending home sales and rising inventories is beginning to indicate over supply setting up lower prices, but there is a wildcard – pent-up demand.

- There is tight relationship between Pending Home Sales and mortgage rates. Mortgage rates have already backed off highs near 8.0% to 6.8%. As rates went up, the real deterioration in demand picked up around 5.5%, so we anticipate that demand will start to build again if rates fall below 6.0%, which looks like could happen by mid-2025.

Focus Point LMI Update

- The Focus Point Leading Market Indicator continued to point towards Neutral Conditions for the month of September.

- Important highlights from the Indicator internals include:

- Improving liquidity conditions as Bank Credit of All Commercial Banks, a data series published in the Federal Reserves H8 release, showed momentum in bank lending that began in June.

- The Fed telegraphing that interest rates will begin easing, reflects positively in our Liquidity indicator.

Weakness in the manufacturing sector is intensifying with softness in Durable Goods Orders, Capex Orders and ISM Manufacturing data.

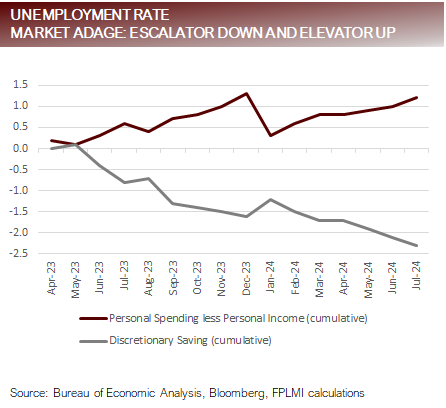

Unpacking relationships between personal income, spending and savings

- Last week’s release of Personal Income and Personal Spending combines with trends in Savings to paint a potentially negative story.

- Personal Income is up about 3.5% in the last 16 months, while at the same time Personal Spending is up a little over 4.5%.

The difference means spending is out pacing income growth. The deficit is coming out of savings. - Savings as a Percent of Disposable Income has fallen in the last 16 months by over 2.0% and is now approaching the post-pandemic lows that were supported by government transfer payments in June of 2022.

- Rising delinquencies tangentially point to rising spending and falling savings taking a toll on consumers. The $64 thousand question is how much longer this dynamic can persist without paying the piper?

For more news, information, and analysis, visit VettaFi | ETF Trends.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected]

Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any

express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied. FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All