Understanding the Potential Effects of Tax Policy on Corporate Earnings

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- Corporate tax rate changes, like the 2017 TCJA, significantly boosted corporate earnings, especially for small-cap companies reliant on domestic revenue.

- Sectors such as Communication Services and Information Technology have reduced their tax burdens since the TCJA, but small-cap sectors like Communication Services and Health Care could see double-digit earnings declines under a 28% tax rate.

- A 25% corporate tax rate would lead to modest earnings declines, but a 28% rate would have a much larger negative impact, with small-cap companies particularly vulnerable due to their domestic focus.

Corporate tax rate policy is a routine hot-button issue during every presidential election cycle, and this year’s campaign is no different.

Shortly after the 2016 election, we attempted to model the impact of former President Trump’s flagship Tax Cuts and Jobs Act (TCJA) on corporate earnings. Unsurprisingly, we determined that reduced tax rates would provide a meaningful boost for corporate profits via reduced effective tax rates.

Our analysis also determined that small-cap companies inherently benefited more due to revenue source composition or, more simply, a “tax geography” effect. Moving down the size spectrum, smaller companies benefit more from reduced U.S. corporate tax rates due to greater reliability on domestic revenues than larger, multinational companies.

Eight years later, markets must contend with the possibility of an opposite, business-unfriendly scenario: the potential for corporate tax rate increases pledged by Democratic candidate and current Vice President Kamala Harris.

Harris is currently proposing a 28% federal corporate tax rate to replace the nominal 21% enacted by the 2017 TCJA. To demonstrate the impact this could have on earnings, we’ve updated our original 2016 model with 25% and 28% baseline assumptions to identify a range of potential outcomes for U.S. equity indexes.

Changes in U.S. Corporate Activity and Tax Environment since 2016

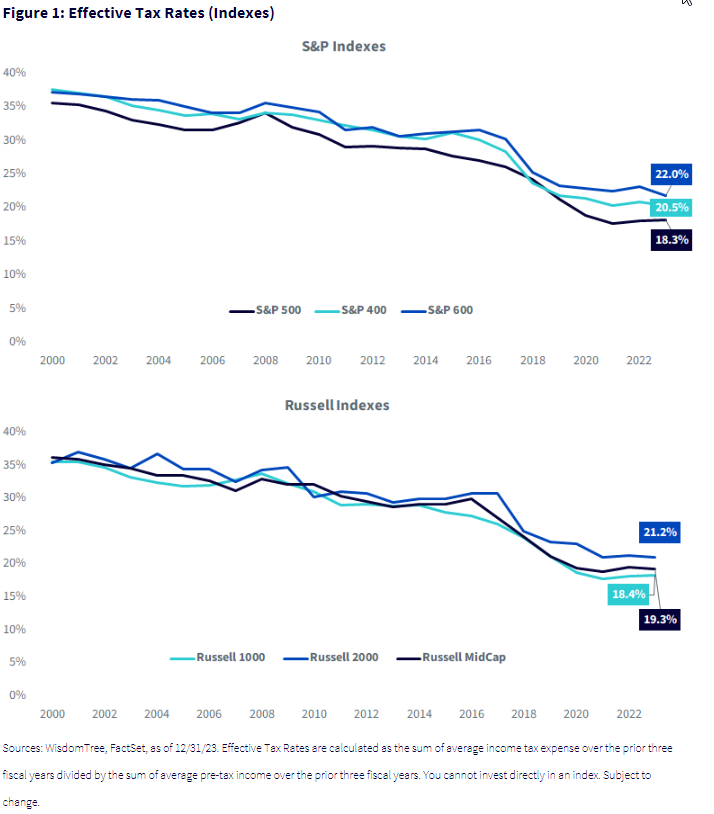

Prior to its passage, most U.S. companies paid about 25%–30% effective tax rates.

Today, however, that range has been meaningfully narrowed and reduced. The effective tax rate for large-, mid- and small-cap U.S. equity segments ranges between 18% and 22%, which is around or below the nominal rate of 21%.

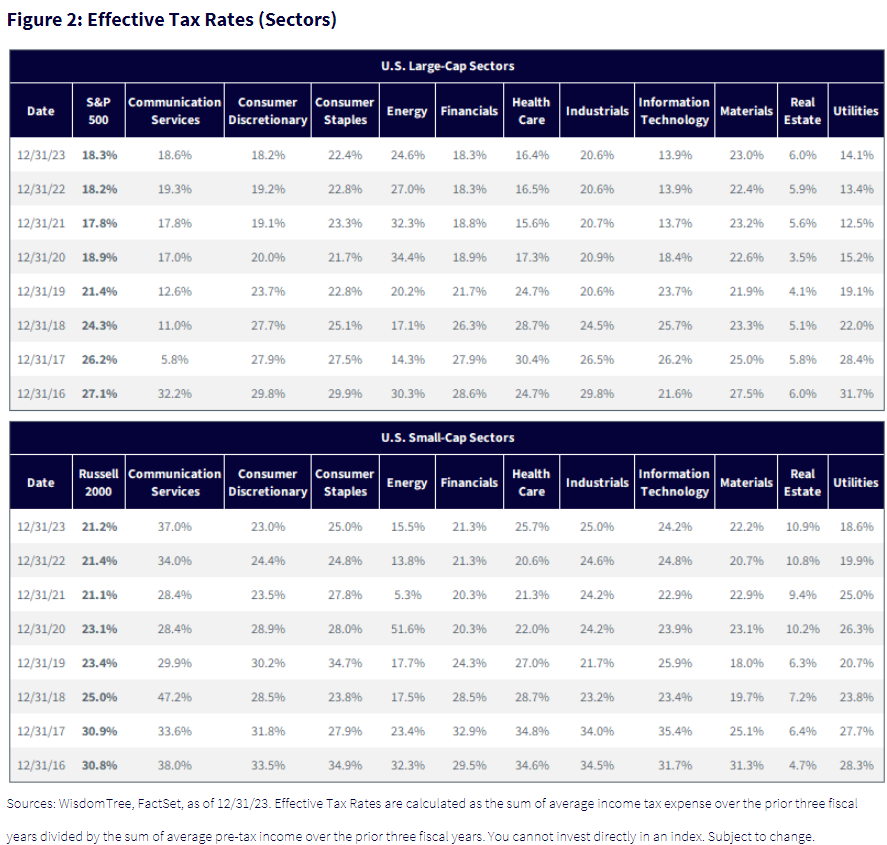

Effective tax rates at the sector level mostly coincide with the decline in rates at the index level as well. Communication Services, Consumer Discretionary, Financials and Industrials have all reduced their tax burdens over time. Information Technology, the largest sector by weight in the S&P 500 Index, remarkably pays less than 14% of its pretax income.

Small caps have benefited from the changing tax paradigm as well. Today, the Russell 2000 pays approximately the nominal 21% tax rate, down from about 31% in 2016, with a sector mix that resembles the trends in the large-cap space.

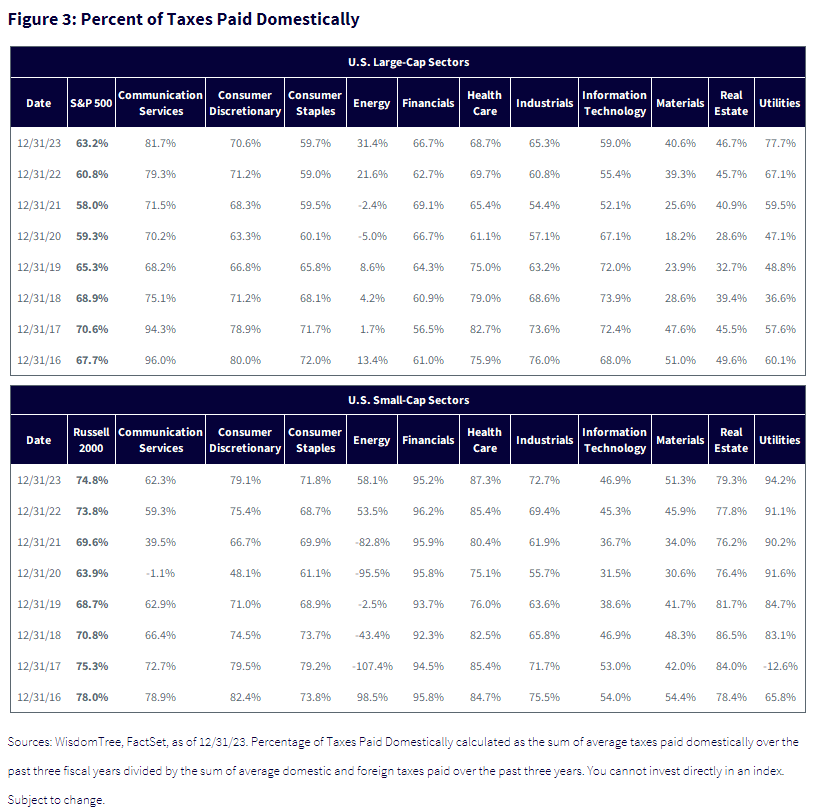

One important caveat, however, relates to non-tax-related changes in the U.S. business environment that have indirectly assisted corporate efforts to avoid taxes since 2016.

The aggregate percentage of taxes paid domestically for the S&P 500 has shrunk to about 63%, down from about two-thirds, reflecting greater geographic revenue diversification among large-cap companies. Several sectors contributed to this shift with individual reductions greater than 10%, while other domestic-reliant groups, like Utilities and Financials, offset the declines with notable increases in their share of taxes paid domestically.

The net effect, however, is a declining domestic tax liability among U.S. large caps, which inherently reduces the sensitivity of their earnings to changes in corporate tax policy.

The same trend is evident, albeit less pronounced, within small caps. Unsurprisingly, the domestic tax shares are a bit noisier at the sector level, but the index-level decline coincides with the large-cap trend in a similar magnitude.

Though small caps still pay 75% of their taxes domestically, any continuation of this downward trend would be advantageous amid the possibility of higher corporate tax rates, as the negative impact on earnings may be mitigated.

Earnings Implications under a Higher Tax Regime

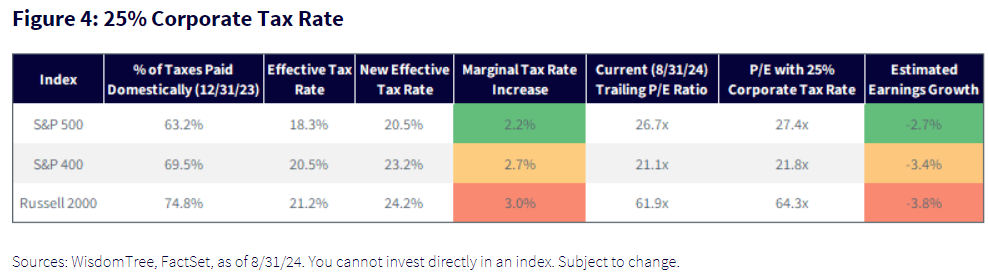

Using trailing three-year averages of effective tax rates and the portion of taxes paid domestically, we anticipate relatively modest impacts to corporate earnings under a 25% statute, with a more pronounced burden at 28%.

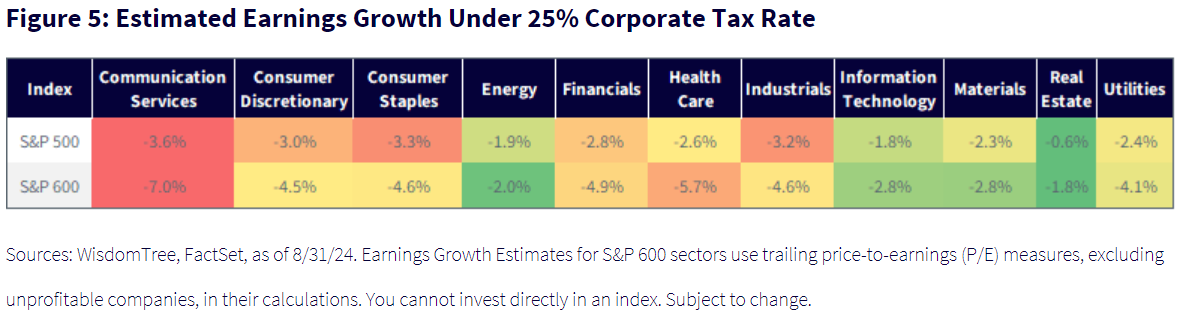

Under a 25% rate, we expect that the marginal increase in the effective tax rate would be between 2% and 3%, with small-cap companies faring worse than mid-caps and large caps. Using August price-to-earnings multiples and holding prices constant, we’d expect prevailing valuations to modestly expand, coinciding with a 3%–4% decline in earnings. Once again, large-cap earnings would likely fare better than small-cap earnings.

At the sector level, Communication Services would suffer the worst earnings declines, while Information Technology, Energy and Real Estate would be least affected. Declines for most other sectors are relatively in line with index-level forecasts.

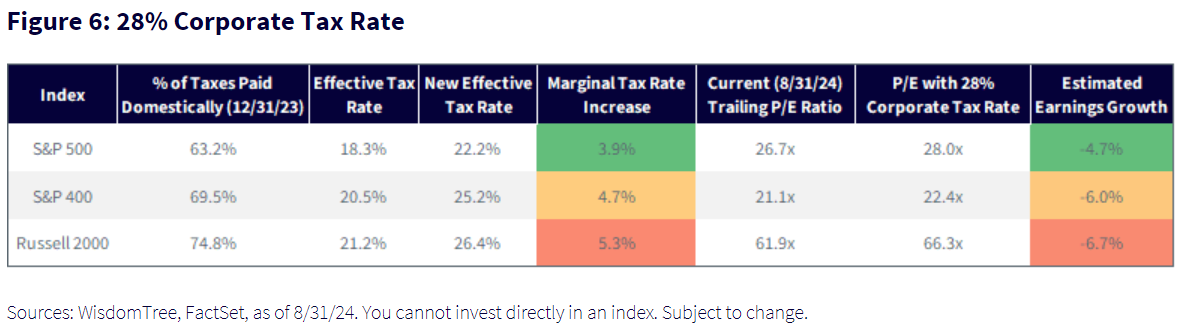

At 28%, however, the effects would be more significant. Under this scenario, we’d anticipate index earnings declines of 5%–7%, which become gradually worse as we move down the size spectrum. This is where smaller companies’ greater reliance on domestic business, compared to larger companies, could become a headwind in a tax hike environment.

An increase to 28% could increase the marginal effective tax rate by 4%–5% for the main U.S. equity indexes, which would likely sour equity sentiment as the burden becomes more challenging to overcome.

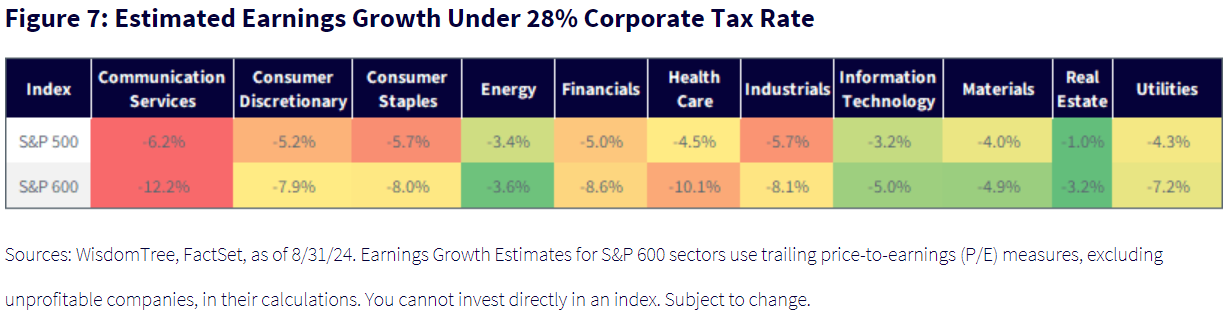

At the sector level, the effects are naturally greater under a 28% statute, with most large-cap sectors comfortably in our anticipated index-level range.

Small-cap sectors, however, illustrate the burden more clearly. We project that Communication Services and Health Care would hit double-digit earnings declines, while four other sectors would lose approximately 8% in profits. That means that about half of small-cap sectors would be expected to have earnings decline by 8% in this scenario.

Conclusion: 28% Is More Painful Than 25%

As markets wait for November’s election, they will constantly evaluate the potential for these tax proposals to come to fruition and the ensuing impact on earnings. As of now, it’s anyone’s guess as to what is likely, what is improbable and what is merely posturing and campaignspeak.

While an increase in the corporate tax rate to 25% would not be business-friendly, we do not think it would have a sizable negative impact on U.S. corporate activity and, therefore, equity market sentiment. A 28% rate, however, is the greater downside risk, in our view. In this scenario, it may force businesses to find creative ways to legally avoid tax liabilities or further globalize their revenue streams for tax advantages.

In the final two months before U.S. voters head to the polls, we will be eagerly watching market activity for tax policy insights and responses.

This article originally appeared on WisdomTree's website and is reprinted on VettaFi | Advisor Perspectives with permission from the author. For more information, please visit WisdomTree.com.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All