Global Economic Outlook: Fall Has Arrived

Fall is the time for change. The days grow short, the air turns cooler, and trees shed their foliage. This autumn, flocks of birds aren’t the only things moving south, as central banks are trying to gently push interest rates downward.

Policymakers are able to ease their stances because inflation is under better control. The drive to achieve soft landings is now focused on preserving growth and employment. The pace of interest rate reductions will be determined by regional circumstances.

Geopolitics are still top of mind. Escalating tensions in the Middle East and on the eastern borders of Europe have the potential to disrupt. The U.S. presidential election, just weeks away, could also make a mark on the global outlook.

Following are our thoughts on how major economies are faring.

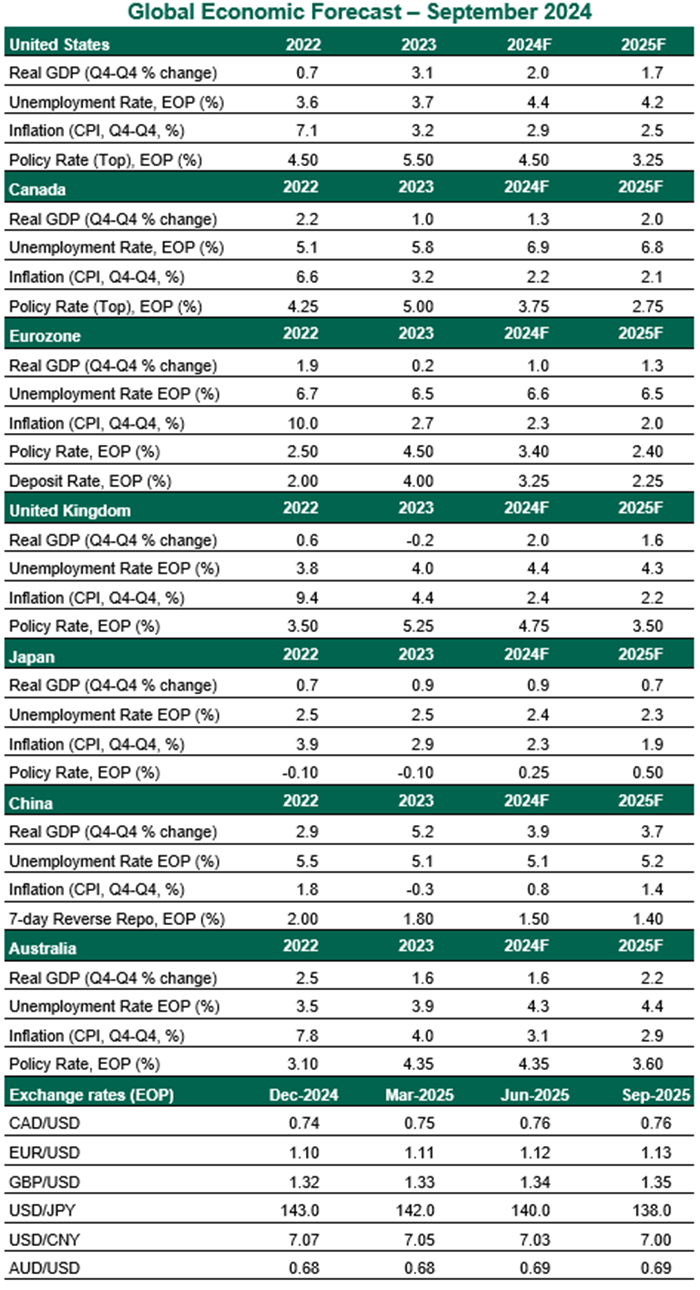

United States

- The Federal Reserve commenced its easing cycle with a 50 basis point cut, the first reduction in four years. Despite a larger than expected cut, Chair Powell stressed that this was not a distress signal, but a “commitment to not fall behind the curve.” The Fed’s Summary of Economic Projections showed 50 basis points of additional cuts in 2024 and 100 basis points in 2025, progressing toward a neutral rate just over 3%. We expect a string of 25 basis point reductions through mid-2025.

- The FOMC’s decision was supported by further progress on disinflation. Both headline and core PCE inflation remained steady at 2.5% and 2.6% year over year in August, in contrast to expectations of a small increase. Though sticky, readings of this magnitude are soft enough to justify rate cuts. A cooler labor market, reflected in lower payroll gains, a higher unemployment rate and slower turnover, also warrants easier monetary policy. That said, a soft landing is coming into view.