Western economies are inching towards soft landings, and their central banks are reducing interest rates. These developments will be helpful to economies in the Asia-Pacific (APAC) region as they conclude 2024 and look forward to next year. However, the outlook for China remains a central concern.

Exports are doing the heavy lifting as domestic activity in many APAC economies has been constrained by tight monetary conditions or low confidence. Regional inflation has come under control, which should allow some central banks to join the global transition towards easing. Japan and Australia are two exceptions: The former is normalizing through policy tightening, while the latter awaits clearer signals of durable disinflation.

Rising protectionism, the outcome of the U.S. election and China’s stimulus strategy are the themes that will be most impactful for regional markets in the months ahead.

Following are our views on how major APAC markets are poised to perform during the balance of 2024.

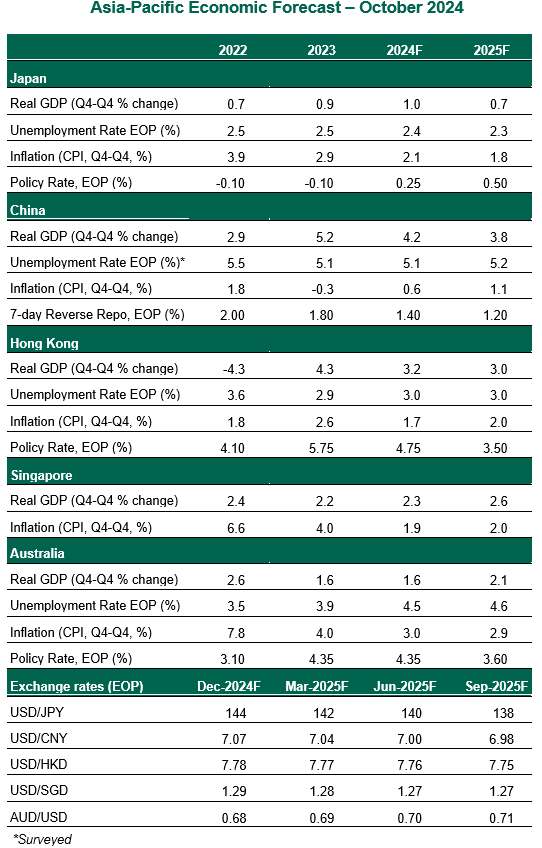

Japan

- Japan’s economy bounced back in the second quarter with real gross domestic product (GDP) growth of 2.9% annualized, following a 2.4% contraction in the first three months of the year. Signs of passthrough from strong wage negotiation to consumer spending are starting to appear, as private consumption turned up for the first time in five quarters. Business investment increased, led by normalization of auto production. Exports moderated last month, but are likely to remain healthy. A modest expansion led by higher incomes and consumption is our base case for the Japanese economy. Japan’s new prime minister Ishiba has pledged to follow the Kishida administration's economic policy, for now.

- The Bank of Japan (BoJ) kept its policy rate at 0.25% at the September meeting. The central bank appears to be in no rush to hike again, following the financial market turmoil after its hawkish tilt in July. Dovish signals were evident in recent BoJ communications. We continue to think that the central bank will stay on hold for the remainder of the year, and foresee only one hike in 2025.

China

- The Chinese economy is stumbling amid further loss of momentum. Consumer spending continues to disappoint amid low confidence. The rate of expansion in infrastructure and manufacturing investment has softened. At the heart of China’s economic woes remains the real estate sector downturn. A slowing economy is deepening a deflationary loop, with consumer price inflation only slightly above zero and producer prices deep into deflation. Only exports remain a bright spot, but rising protectionism could worsen overcapacity problems and make deflationary pressures more acute.

- The disappointing news on almost all fronts has forced policymakers to turn the tap on more stimulus. However, the scale and composition of easing was still not comparable to that of 2008 or 2016. Recent policy measures included cuts to policy rates, reserve requirement ratios, mortgage rates and one-off cash handouts to the poor. While these measures were cheered by China’s stock markets, the growth picture will not brighten materially without substantial assistance for domestic demand.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust