Moody’s Friday downgrade of the U.S. credit rating may not seem particularly earthshaking, given that Fitch and Standard & Poor’s had gotten there quite a while ago. Still, it’s an important reminder that the quintessential “risk-free” rate may not be quite so risk free. Just a smidge of perceived risk in U.S. Treasuries can put upward pressure on interest rates—particularly longer-maturity Treasuries. While there are a host of arguments as to why this may be so, perhaps the most obvious has been somewhat overlooked—the credit term premium. Time exacerbates credit risk. Today, for example, AAA U.S. industrials have nearly a zero spread to U.S. Treasuries for six-month maturities, but about 50bps spread for 10-year maturities, according to Bloomberg. What might this mean for the Treasuries themselves? A whiff of credit risk may steepen the U.S. Treasury curve—with a larger spread between the 10-year Treasury and the Fed Funds Rate.

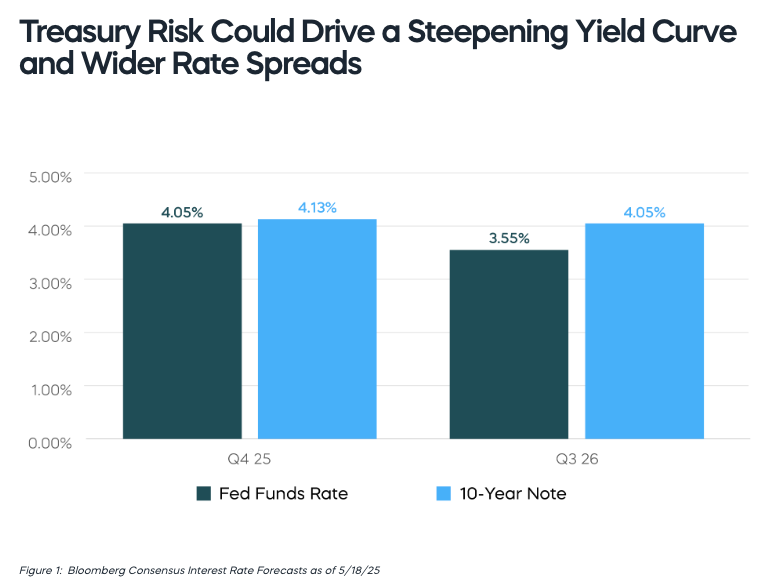

Even before the Moody’s downgrade, consensus forecasts indicated perhaps too flat of a yield curve. While 50bps of cuts both this year and next may be reasonable forecasts for the Fed Funds Rate, the historical average real yield on the 10-year Treasury of around 2.5% suggests a nominal yield more in the 4.5% range—and that’s if inflation gets down to 2%. Add that smidge of credit risk into the mix (oh, and maybe a little tariff-driven inflation) and a 4% 10-Year Treasury yield sounds a bit light.