General Douglas MacArthur once remarked that “rules are mostly made to be broken.” He was at odds with U.S. President Harry Truman over the conduct of the Korean War, feeling that the restrictions placed on his forces weren’t supportive of success.

Governments use fiscal rules to limit government deficits, restrain borrowing and safeguard debt sustainability. But there are significant questions over whether they are supportive of economic success.

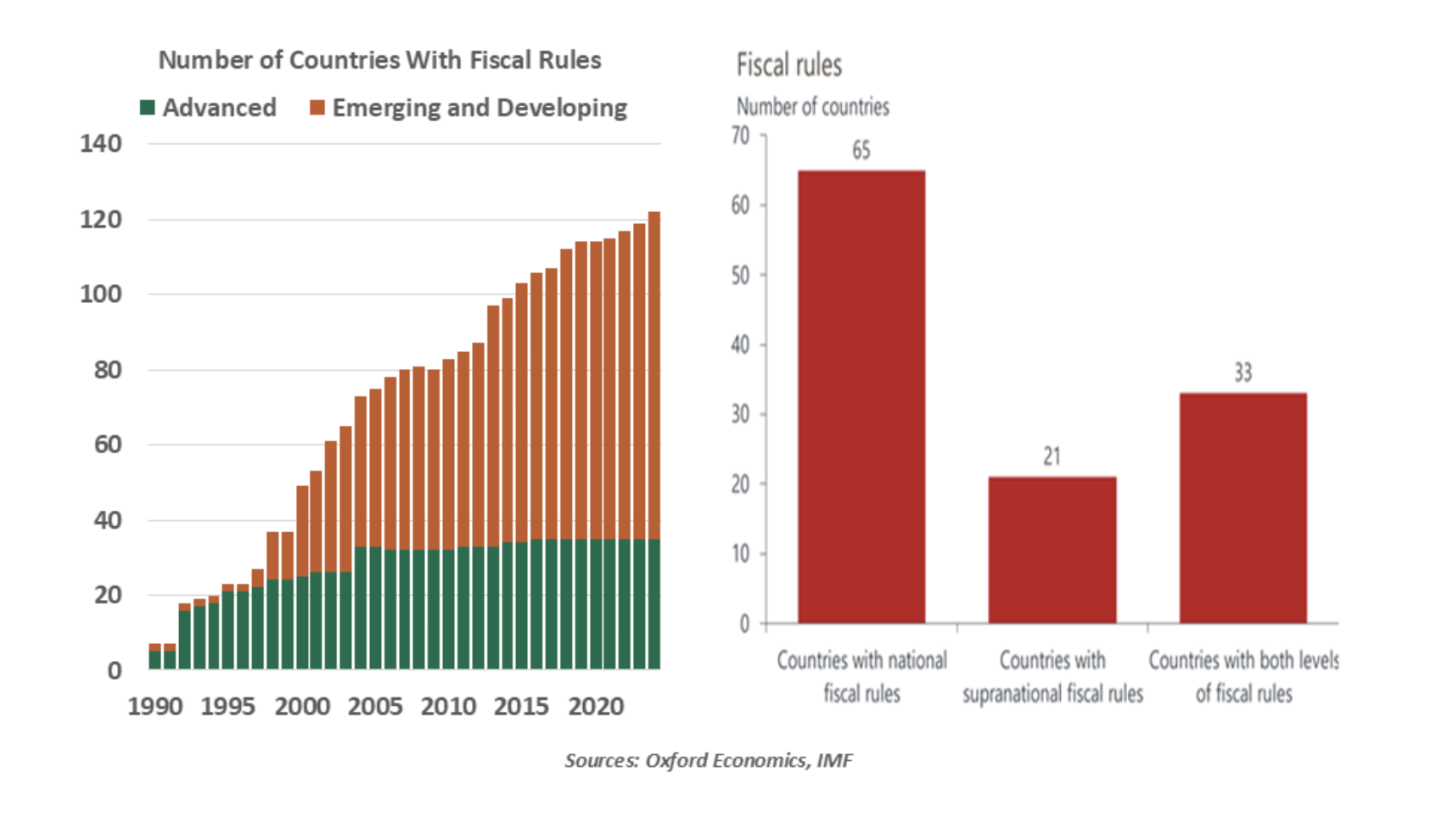

Advanced and emerging economies alike have steadily expanded their use of fiscal rules. More than 120 countries currently operate under them, compared with only a handful in the early 1990s.

Adding rules illustrates policymakers' desire to impose discipline on a process that is intrinsically vulnerable to political wills. Governments often exhibit a bias toward higher spending and borrowing. The benefits of public expenditure are immediate and visible, while the costs only become evident over the longer term. Fiscal rules seek to counter this tendency by placing limits on government accounts.

These constraints can take a number of forms, each targeting a different aspect of fiscal policy. They include rules governing budget deficits, debt levels, spending growth and revenue allocation. In theory, these measures help governments maintain sustainable finances, retain credibility and reassure investors.

Examples can be found across both advanced economies and emerging markets (EMs). The U.K. operates under rolling fiscal mandates that require public debt as a share of gross domestic product (GDP) to fall over a specified horizon while aiming to balance day-to-day spending and revenues. Switzerland's “debt brake” links spending to cyclically adjusted revenues, earning that country a reputation as one of the world’s most fiscally prudent. Australia follows a medium-term fiscal strategy focused on achieving budget balance over the economic cycle and stabilizing public debt. The eurozone's Stability and Growth Pact sets benchmark limits of budget deficits equal to 3% of GDP and public debt of 60% of GDP. The U.S. does not have a comprehensive national fiscal rule, but it does have a debt ceiling that attempts to impose limits on government borrowing.

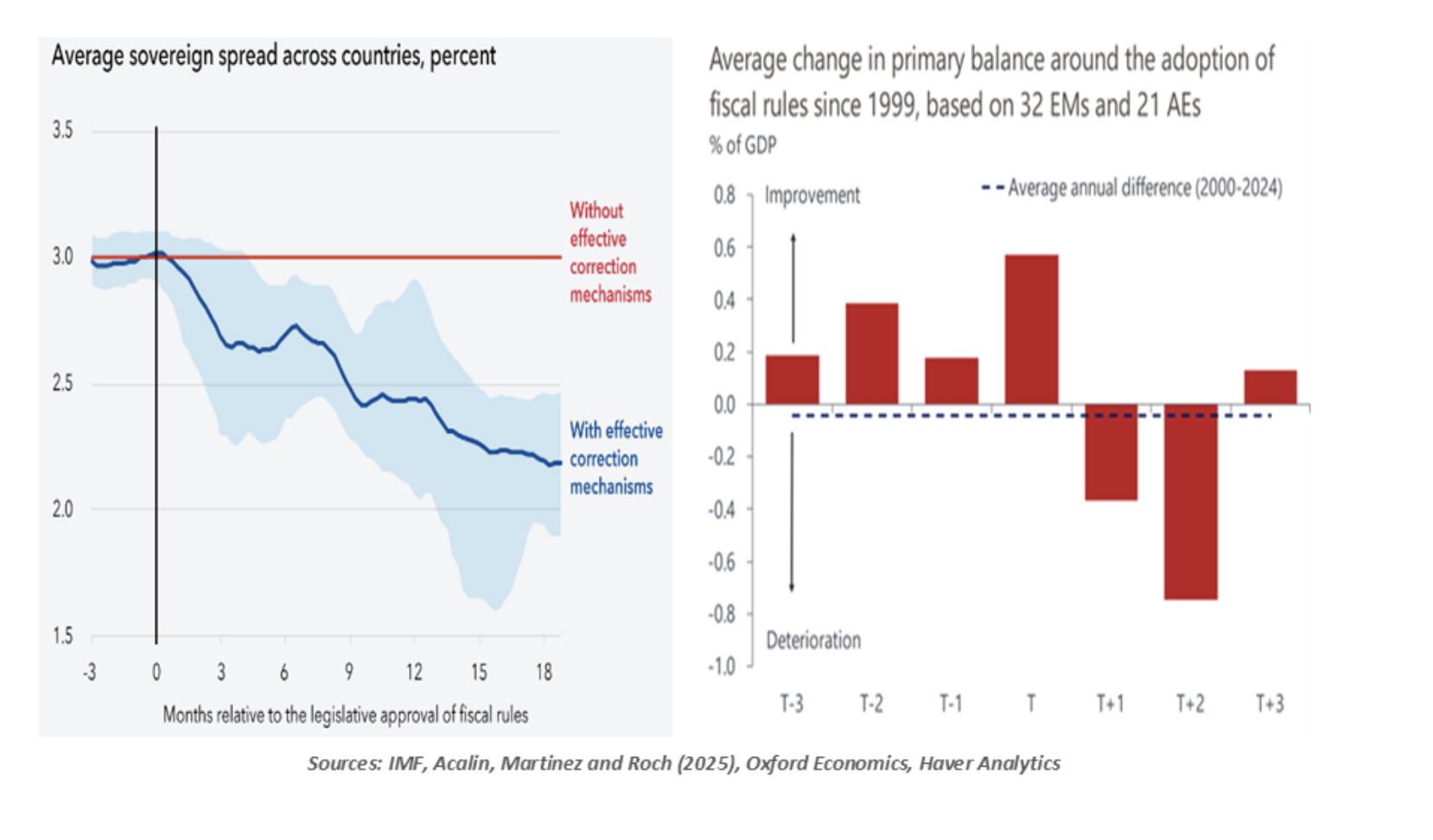

Credible rules can help reduce borrowing costs by increasing confidence in the future path of public finances. Research indicates that countries adopting them see their borrowing costs fall by around 0.3 percentage points within six months and 0.75 percentage points within a year compared with peers lacking effective fiscal rules.

Yet countries do not always adhere to the fiscal rules that they have established. According to the International Monetary Fund (IMF), countries have complied with their fiscal rules only around 60% of the time over the past two decades. Governments often improve their fiscal position in the run-up to adopting a rule, but struggle to sustain those gains thereafter. Oxford Economics finds that primary balances improve by 1.1% of GDP in the three years leading to adoption, only to deteriorate by an equivalent amount over the following two years.

Fiscal rules are popular, compliance less so.

See more: Fiscal Dominance Is Here

One reason fiscal frameworks fall short is that governments facing uncomfortable constraints frequently possess the power to loosen them. Deficit limits are suspended, debt targets are deferred, escape clauses are invoked, accounting treatments are adjusted, and off-budget entities are used to assume liabilities that would otherwise appear on the public balance sheet.

U.S. policymakers work around fiscal constraints through temporary provisions, sunset clauses, and other legislative devices. Six eurozone member states are currently subject to the Excessive Deficit Procedure, while countries such as France and Italy have faced the process multiple times. Yet enforcement has been limited, with meaningful penalties never imposed for fiscal slippage.

While one could argue that the world has experienced two once-in-a-generation shocks since 2008, significantly reducing fiscal space, noncompliance with fiscal rules was already widespread before the pandemic. The crisis merely widened deviations from established fiscal targets in places like the eurozone. The IMF highlights that more than two-thirds of countries have revised their rules since the pandemic, without any improvement in compliance.

When fiscal rules fall short, bond markets can prove more effective at imposing discipline, often swiftly and painfully. The United Kingdom's 2022 "mini-budget" fiasco offers a powerful example that drove gilt yields higher and sterling lower, forcing a rapid policy reversal.

Markets punish fiscal indiscipline faster than rules do.

Sustainable public finances support long-term growth, while excessive debt can crowd out private investment, raise future tax burdens and leave governments vulnerable to shifts in market sentiment. Rising public debt diverts resources toward interest payments, leaving less funding available for high-multiplier investments such as infrastructure. Restraint during good times builds the buffers that allow governments to respond more forcefully when recessions arrive.

Yet discipline must be balanced against flexibility. Governments that shift too rapidly toward fiscal consolidation while economies remain fragile risk slowing recoveries and exacerbating economic weakness. Governments are in the best position to make long-term investments in economic infrastructure, which may be difficult to accommodate under fiscal rules.

Douglas MacArthur was ultimately relieved of his command for failing to comply with presidential directives. The consequences for countries that fail to comply with fiscal rules remain to be seen.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Northern Trust

More Market Indicators Topics >