Note from dshort: This is the second installment of a two-part article on P/E ratios by Ed Easterling. Ed's books, Unexpected Returns and Probable Outcomes, have our unqualified endorsement for anyone trying to understand the complex and often puzzling relationship between the economy and the market.

The previous segment identified the price-to-earnings ratio ("P/E") as a useful measure of stock market valuation. Further, it explored in detail the need to normalize the E in P/E (i.e., earnings per share — EPS) and it highlighted two of the more recognized methodologies for generating a reliable P/E.

When measured accurately, P/E is more than simply an indicator of market valuation; it is the primary driver of stock market returns. Note the distinction. P/E does more than tell us whether the market is cheap or expensive. The starting level for P/E, as well as its cycle over time, drives the returns that investors achieve.

Periods that started with low P/Es have historically generated above-average returns over longer-term investment periods. Conversely, periods starting with high P/Es lead to below-average returns. This occurs because the level of P/E impacts the yields realized from dividends and the change in P/E over an investment horizon either multiplies or mutes the ultimate investment returns. Long-term periods when P/E doubles or triples, so-called secular bull markets, deliver strong double-digit returns to investors. When P/E declines by half or more, so-called secular bear markets, stock market returns are generally well-below average.

There are two key points. P/E measures the market's valuation level. In addition, the valuation level and trend in P/E drive investor returns. That is why it is so important to understand the force that drives P/E. P/E is not a phenomenon; it is driven by fundamental economic principles.

P/E & INFLATION

Stocks are financial assets. Financial assets have value based upon their future cash flows and market interest rates (also known as the discount rate). For example, when bond yields rise, bond prices fall. The decline in price results when a higher market interest rate is applied to discount the bond's future cash flows. The primary driver of bond yields over the long-term is the inflation rate. When inflation rises, market interest rates rise (especially longer-term yields), and bond prices fall. The opposite happens when inflation declines.

That same effect impacts the stock market. As inflation rises, market rates rise, and prices fall. For stocks, this means that the price falls in relation to current-year earnings. Thus, the P/E ratio for the market declines. Higher inflation drives lower P/Es.

As the inflation rate declines toward zero, interest rates fall and P/Es rise. But then P/Es reach a peak. As the inflation rate falls into deflation, interest rates continue to fall toward zero and the related discount rate produces high values for financial assets. Yet in deflation, bonds diverge from stocks.

Bonds have fixed payments which become ever more valuable in deflation. Stocks, however, have earnings and dividends that react to deflation and decline in nominal terms. Deflation causes the reported (i.e., nominal) value of sales, costs, and profits to decline. The result is that the cash flows from stocks reflect a declining trend during deflation. The value today for a declining stream of cash flows is less than a rising stream of cash flows. When the decline increases due to greater deflation, today's value also declines. As a result, rising inflation and worsening deflation drive P/E lower, and P/E peaks when the inflation rate is near price stability.

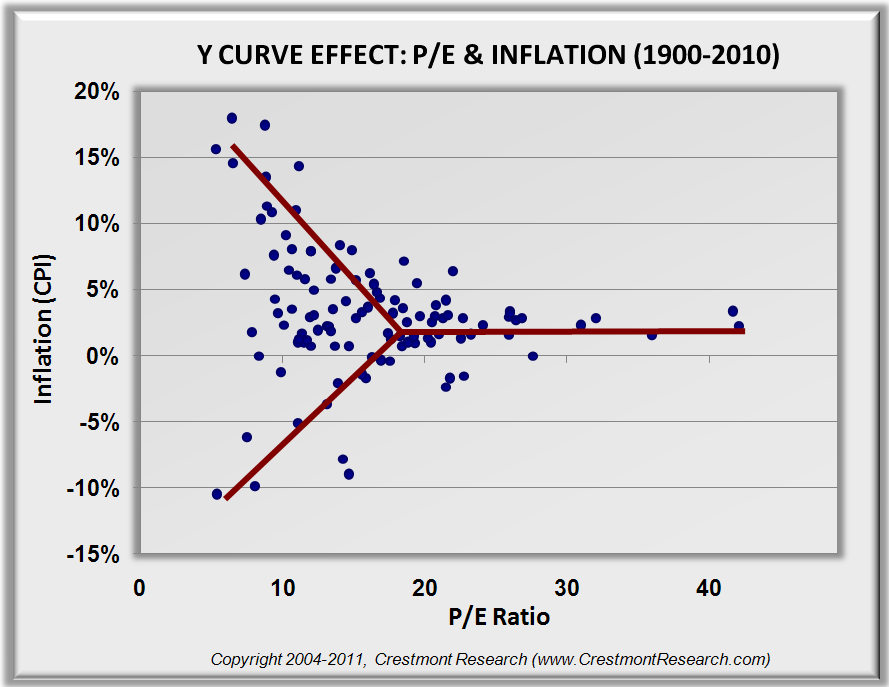

This effect not only is true in theory according to generally accepted financial and economic principles, but also it is true empirically in the data of history. This dynamic was presented graphically in Unexpected Returns (and explored in more depth in Probable Outcomes) as The Y Curve Effect. Figure 1 below presents the relationship between P/E and inflation for all years since 1900. Note the pattern of a sideways Y reflecting the expected decline in P/E as the inflation rate moves away from price stability.

Figure 1. The Y Curve Effect

To emphasize the relationships, let's walk through a series of charts developed through collaboration between Crestmont Research and dshort.com. The graphics evolve to reveal ever more insights. For the following charts, Crestmont's data has been extended back to 1871 and is developed on a monthly basis. The graphical layout and other methodologies are based upon Doug Short's work.

The main body of Figure 2 presents the long-term history for P/E on a monthly basis relative to its mean. For comparison, the chart includes both the Crestmont P/E and the Shiller P/E10. Underlying the chart is the villain to P/E, the inflation rate. The inflation rate is represented by reported CPI without adjustment.

Figure 2. P/E Relative to Its Mean & the Inflation Rate

But reported CPI can be volatile due to temporary forces that don't always reflect core financial inflation. Also, modern measures of core inflation aren't available for earlier periods. Most importantly, P/E tends to respond to expected trends more so than short-term blips. To assess trends, a multi-year average of CPI mutes the noise and reveals the underlying cycles.

Figure 3. P/E Relative to Its Mean & the Inflation Rate (3-Year)

Figure 3 presents the same information from the previous figure, except the monthly inflation data has been converted to a measure reflecting the average annual inflation rate over the trailing three years. This chart begins to show that extreme periods of inflation correspond with lower P/E, while significant deflation also corresponds with lower P/E. This is consistent with the financial principles discussed earlier as well as The Y Curve Effect.

The earlier principles indicated three major categories for the inflation rate as it relates to P/E. First, high inflation drives P/E lower. Second, low and stable inflation drives P/E higher. Third, deflation drives P/E back down from the highs of price stability. To further highlight the three categories and the effects, Figure 4 presents the inflation rate with a few adjustments to help tell its story.

Figure 4. P/E Relative to Its Mean & the Inflation Rate (Categories)

The inflation rate on the lower part of Figure 4 has been separated into the three categories: (1) inflation of more than 3%, (2) price stability between 0% and 3%, and (3) deflation. To be consistent with the display of P/E as a percentage of its mean, the inflation rate is assessed in relation to its long-term average. Finally, the variance from the mean is presented on the graph as an absolute value on an inverted scale. This means that the more that inflation deviates from the mean, whether high inflation or deflation, the greater the extension downward. In layman's terms, high inflation and deflation depress P/E; the extension downward on the graph of high inflation and deflation reflect the gravitational effect that bad inflation/deflation conditions have on P/E.

Also, the chart emphasizes the relatively rare condition of low and stable inflation (bright green) that drives P/E to higher levels. This highlights the major vulnerability for P/E today. The tectonic plates of inflation and deflation are tightly bound — either direction is a plausible course. Either one also would drive P/E lower!

Let's look again at the historical relationship between P/E and inflation. This time, the chart includes monthly data from 1871 with colors that match the categories from Figure 4. As presented in Figure 5, rotated upward versus The Y Curve in the first figure, deflation and inflation drive P/E lower and low inflation is the need to sustain higher P/Es. Figure 5 goes further and highlights P/Es journey through the tech bubble. This emphasizes the unlikely repeat anytime soon of such an irrational state and it signifies that the current P/E is on the upper floors of market valuation.

Figure 5. Correlation of P/E & the Inflation Rate

Another reality is that the stock market is entering one of those periods where reported P/E is being distorted downward (as discussed in the first segment of this article). The normalized measures reflect that P/E is relatively high, albeit relatively consistent with low and stable inflation. Nonetheless, a move away from this zone portends headwinds for the stock market. Generally, those headwinds don't just slow forward progress; they often result in volatile up and down markets. This is why investors not only need accurate measures of current conditions, but also perspective about the future. An upcoming article will use the Crestmont methodology for EPS and P/E to assess the future, a feature not available with other versions of P/E. Until then, it's probably not yet time to head for the door, but it is likely a good time to emphasize risk management and diversification.

Copyright 2011, Crestmont Research (www.CrestmontResearch.com)

Ed Easterling is the author of Probable Outcomes: Secular Stock Market Insights and award-winning Unexpected Returns: Understanding Secular Stock Market Cycles. Further, he is President of an investment management and research firm, and a Senior Fellow with the Alternative Investment Center at SMU's Cox School of Business where he previously served on the adjunct faculty and taught the course on alternative investments and hedge funds for MBA students. Mr. Easterling publishes provocative research and graphical analyses on the financial markets at www.CrestmontResearch.com.