For the past several years, I have written extensively about the Fed’s dangerous efforts to drive interest rates low enough to stimulate a stronger recovery. As a consequence, large and small investors have been compelled to go out on the risk curve in a desperate search for higher yield.

Lured by almost irresistible double-digit yields in 2012 and early 2013, investors dived into mortgage REITs with abandon. Having discussed the serious risks of equity REITs in my previous article , now is a good time to examine whether mortgage REITs pose similar risks for the unwary.

Essentials about mortgage REITs

What are the key considerations to assess when deciding whether to buy, sell or hold any of the larger mortgage REITs? Most analysts and investment advisers believe that future changes in interest rates are the most important factors. An example of this obsession with interest rates can be viewed in a January 2015 analysis by Nomura Securities.

Are these analysts right or are there more important considerations that investors usually overlook?

Let’s start with the basics. Mortgage REITs hold residential mortgage-backed securities (RMBS), and finance them primarily through short-term repurchase agreements. These REITs have benefited directly from the Fed’s policy of keeping short-term interest rates very low. Their income is derived from the positive spread between the cost of their short-term borrowing and the cash flows that are provided by the longer-term RMBS.

How can mortgage REITs throw off double-digit dividend yields in our low-interest-rate environment? It is really simple – very high leverage. Those REITs that invest primarily in Fannie Mae or Freddie Mac RMBS have debt-to-equity ratios of 6-to-1 or higher.

Because the REIT is able to buy RMBS tranches that total many times its equity through borrowing, the dividend that this leverage throws off to investors is magnified. So a dividend yield of 12-18% seems too good to pass up for many investors.

However, leverage is a double-edged sword. When their cost of funds rose, as it did after Chairman Bernanke’s taper speech in May 2013, this dramatically cut REIT earnings and forced most of them to sharply reduce their dividend. Some of the most highly leveraged REITs faced margin calls from their lenders because of the drop in the value of their RMBS collateral. They were forced to sell some of their RMBS holdings to meet those margin demands.

A second factor that has been almost totally disregarded is the serious delinquency problem with their mortgage portfolios. This is especially true with American Capital Agency (AGNC), Two Harbors Investment (TWO) and Invesco Mortgage Capital (IVR).

Non-agency mortgage-backed securities

Non-agency mortgage-backed securities hold mortgages that are not guaranteed by Fannie Mae or Freddie Mac nor insured by the Federal Housing Administration (FHA). Nearly all of them were originated prior to early 2007 when the sub-prime mortgage market collapsed.

The vast majority of those still outstanding today were issued during the bubble years of 2005-2007, when underwriting standards totally disappeared. Many of their mortgages required little or no down payment. Borrowers could often qualify with debt-to-income ratios (DTI) of 50% or more, which was not acceptable in prior years. Low-documentation mortgages that became known as “liar loans” enabled rampant fraud.

Two Harbors Investment Corporation

Let’s take a look at the portfolio of one of the large mortgage REITs that is loaded with these non-guaranteed RMBS – Two Harbors Investment Corp. (NYSE: TWO)

As described in its 2014 10-K report filed with the SEC, this REIT allocated roughly $3.04 billion to non-guaranteed RMBS. That was a 10% increase over 2013. More than 85% of them were originated in 2006 or later.

In this 10-K report, I also discovered that $1.82 billion of these mortgages were sub-prime loans – 77% of the entire non-guaranteed portfolio. Here is the stunner: more than 13% of all the non-agency loans were considered so bad that they did not have any rating at all. Two years earlier, only 5% of these mortgages were unrated.

Because of the high delinquency/default rate on these sub-prime loans, this REIT was able to buy the entire non-guaranteed RMBS portfolio at a substantial discount. They paid an average of only 59% of the par value. That sounds like opportunistic investing, right?

It isn’t that simple. To comprehend the risks of default in any RMBS piece (known as a tranche), you have to find out as much as possible about the characteristics of the mortgages housed in it.

Let me give you an example. The 10-K report reveals that more than 26% of all the non-guaranteed mortgages in this portfolio were seriously delinquent by 60 days or more. That should not come as a big surprise. What does this mean for investors who own shares of TWO?

In previous articles, I have discussed in detail the downgrades of non-agency RMBS that Standard & Poor’s (S&P) announced in August 2012. S&P admitted it had badly underestimated the percentage of delinquent loans and modified loans it expected to ultimately default.

Why had its estimations turned out to be much too optimistic? It had not given sufficient weight to the extent a property with a first lien was underwater.

That was a shocking admission. For several years there has been compelling evidence that underwater loans defaulted more frequently than those by borrowers who still had equity left in their home. I discussed this credible evidence in articles published as early as 2011. They included an important Federal Reserve Board (FRB) study that showed that defaults increased directly in proportion to the degree to which a property was underwater.

S&P carefully described its revised assumptions concerning the likelihood of default for loans not guaranteed by Fannie Mae, Freddie Mac or insured by the FHA (all known as non-agency). It is worth repeating here. For mortgages that were either 90+ days delinquent or with a notice-of-default (NOD) already recorded, S&P expected 100% of them would end up in default. Not most of them … all of them!

It gets worse. A couple of years ago, I talked on the phone with a spokesperson for S&P who told me unequivocally that for underwater loans where the loan-to-value ratio (LTV) was greater than 120%, they now assumed that 100% of these mortgages would also eventually end up in default.

Investors who purchased REITs that held non-agency mortgage-backed securities – or are considering doing so – need to understand the implications of S&P’s admission.

Two Harbor’s 2014 10-K report explained that 35% of all the mortgages in their non-Agency RMBS portfolios were originated in the states of California and Florida. Because these two states suffered some of the worst plunges in home prices after the bubble collapsed, it is no stretch to assume that the vast majority of these properties have LTVs higher than 120%. An additional 13% were in New York and New Jersey, which were also hard hit by the crash.

This serious delinquency percentage would be much higher were it not for the huge number of these mortgages that have been modified.

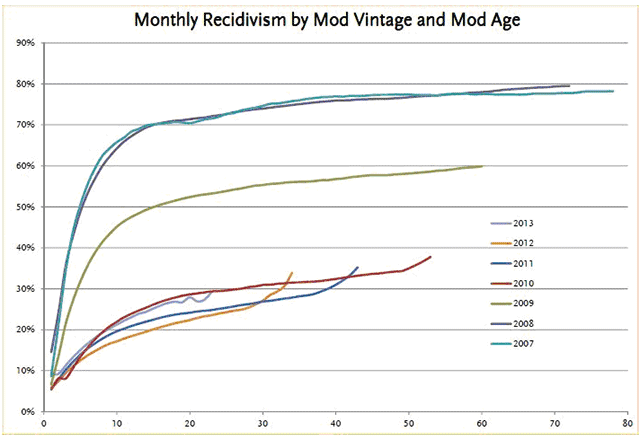

According to data-provider TCW, more than 47% of all non-guaranteed sub-prime mortgages have been modified by servicing banks as of February 2015. Why is this a problem for Two Harbors? Don’t mortgage modifications help reduce foreclosures? Take a careful look at this next chart from TCW.

Let me explain this shocking graph. For those borrowers whose loans were modified right after the housing market collapsed – 2007 and 2008 – nearly 80% have already re-defaulted. Those mortgages modified in 2010 and 2011 are seeing re-default percentages approaching 40%. Even the most recent modifications in 2013 have re-default rates of 30% and are clearly climbing higher.

Why are re-default rates so high? If you were in the homeowners’ shoes, wouldn’t you consider re-defaulting? Think about it. Most of their homes are badly underwater because the loans were originated during the bubble years. Since these are not mortgages guaranteed by Fannie Mae or Freddie Mac, they cannot refinance under the government’s HARP program. So any modification obtained did not reduce their monthly payments very much.

Those homeowners with modified mortgages also know that servicing banks have sharply curtailed foreclosure activity, so the consequences of re-defaulting are minimal. The temptation to re-default is irresistible.

Hence, it is reasonable and even prudent to expect that huge numbers of the modified mortgages in their non-guaranteed portfolio will re-default.

Let me explain one more key problem for Two Harbors not mentioned in the 10-K report. The banks servicing these mortgages have agreements requiring them to advance principal and interest payments to the investors for loans that are delinquent. The banks will get reimbursed when the house is eventually foreclosed. But there is an escape clause that enables the banks to avoid forwarding payments if they believe it is likely that they will not be fully reimbursed after foreclosure. The servicer determines how likely this is.

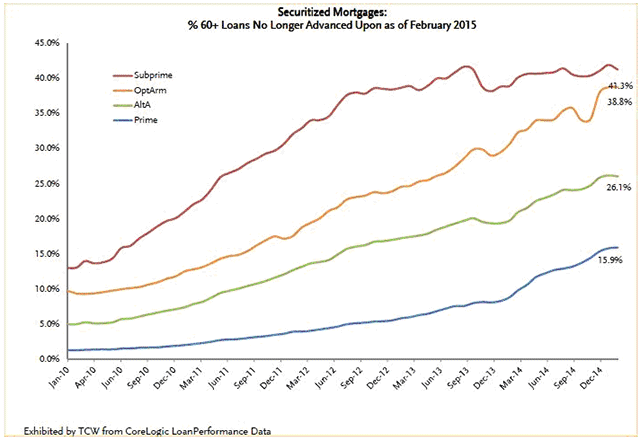

This next chart from TCW clearly lays out the scope of the problem. It shows the percentage of non-guaranteed loans delinquent by 60 or more days where the servicing bank has stopped advancing the mortgage payment to the investor.

For more than 41% of all non-guaranteed sub-prime mortgages delinquent by 60 days or more as of February 2015, the servicers were no longer advancing mortgage payments. Even worse, the percentage of delinquent prime mortgages whose payments are no longer being advanced has tripled in the last two years to nearly 16%. Almost all of these prime mortgages are jumbo loans whose amounts are too large to qualify for Fannie Mae or Freddie Mac guarantees. It is very likely that the delinquent portfolio of Two Harbors is in a very similar situation.

The consensus is that servicing banks can play this game of kick-the-can-down-the-road for the millions of seriously delinquent borrowers indefinitely. But it would be a huge mistake for advisors and their clients to make this assumption.

When mortgage servicers finally start to either foreclose on these properties or complete short sales in earnest, losses to Two Harbor and other mortgage REITs that own these non-guaranteed mortgages will soar.

What about the earnings picture for TWO? Net earnings per share plunged from $1.65 per share in 2013 to $.46 last year. Its dividend has been slashed several times since 2012, but the 2014 dividend payout still far exceeded last year’s income. With its cash flow in serious trouble, the shares of TWO could plunge substantially lower in the next couple of years.

American Capital Agency

American Capital Agency (AGNC) is the second largest mortgage REIT. Their assets grew tremendously between 2011 and mid-2013 as investors poured into this REIT in search of higher yields.

Because few investors or their advisors are aware of the risks to which they are exposed from AGNC, let’s turn to their 2014 10-K Annual Report.

The assets in their portfolio are an unusual mix. Two-thirds of the entire $51.6 billion fixed-rate Agency MBS portfolio consisted of Fannie Mae and Freddie Mac mortgages with balances that averaged $97,000 or of refinanced mortgages issued under the government’s HARP program.

This HARP refinance program is a serious problem. Although HARP began in 2009, the refinancing totals were quite disappointing until the government came out with its HARP II program in December 2011. HARP II was designed to encourage underwater borrowers to refinance. Until then, having an underwater property had precluded them from refinancing.

Unfortunately, HARP II has shown that the government has learned nothing from the post-bubble housing crash. This program completely discarded any sensible underwriting standards.

Under the HARP II eligibility rules, there were no limits as to how far underwater a home could be. Like the bubble-era “no-documentation” mortgages, the borrower did not have to verify that they had any income. Amazingly, there was no requirement that the applicant be employed. Reminiscent of the bubble-era madness, the designers of HARP II also permitted underwater investment property and second homes to be refinanced.

Knowing what happened during the lunacy of 2004-2007, what lender concerned with repayment of the mortgages would offer terms like these?

In the 10-K report, AGNC stated that the average LTV of its HARP portfolio was 116%. This meant that the average outstanding loan balance was far higher than the current value of the property. I have shown hard evidence that the chances of a borrower defaulting rises steadily as the home becomes more underwater. Remember what I said earlier about S&P’s latest default assumption about underwater loans. If we apply that to the billions of dollars held by AGNC in underwater HARP mortgages, nearly all of them will eventually default.

As with other mortgage REITs, AGNC’s income is derived from the spread between their cost of funds and the yield on their MBS portfolio. Since 2011, their average cost of funds has steadily risen while the average earnings on their portfolio has been declining. This has resulted in a steady drop in their net interest spread. Net earnings per share declined every year since 2010 and 2014 saw a loss of $0.72 per share. Similar to Two Harbors, the dividend payout of $2.61 per share put a severe squeeze on its cash position.

What has compounded American Capital’s problems is how highly leveraged they are. The 10-K report stated that its average debt-to-income ratio in 2014 was seven to one. This high leverage has forced them to reduce their portfolio from $85 billion in 2012 to $56 billion at the end of last year.

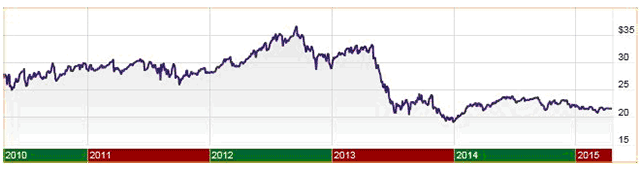

Take a good look at AGNC’s five-year price chart.

Source: scottrade.com

The shares have declined from a high of 36 in the fall of 2012 to a little more than 21 on April 24 of this year. Given all the problems I have discussed, it could head much lower.

Invesco Mortgage Capital

Let’s examine one more large-mortgage REIT – Invesco Mortgage Capital (IVR).

The 2014 10-K report provides some very troublesome details about its RMBS holdings. Their portfolio now consists of agency-guaranteed RMBS, non-Agency RMBS, commercial mortgage-backed securities (CMBS), and whole residential loans.

As with Two Harbors and American Capital Agency, Invesco has a multi-billion dollar non-agency RMBS portfolio. One-third of its $3 billion non-agency portfolio consists of mortgage loans that were re-securitized between 2010 and 2012. You might think that these were not dangerous holdings. Here is the problem with them: every one of these re-securitized mortgages was originated in the three bubble years 2005-2007. Without question, the vast majority of these properties are now underwater.

Making matters worse, Invesco held nearly $700 million in bubble-era alt-A mortgages. These are mortgages originated in 2005-2007, which were terribly underwritten – with little or no documentation of income and debt-to-income ratios (DTI) of up to 50%. Furthermore, there is very reliable evidence showing massive lying on their mortgage applications, which asserted that they intended to live in the home. Investors who lied have had much higher delinquency rates than actual owner-occupants.

The most recent figures we have – from early 2013 – revealed that more than 30% of these bubble era Alt A mortgages were either seriously delinquent or in foreclosure. This delinquency rate would be much higher now if 22% of alt-A mortgages had not been modified.

Finally, the 10-K report revealed that Invesco owned roughly $570 million of RMBS tranches holding prime jumbo mortgages originated during these three bubble years. The latest figures available – early 2013 – showed delinquency rates of 17-19%. Like other bubble-era loans, the delinquency rate on these jumbo mortgages would have been much higher had many of them not been modified.

The geographical concentration of Invesco’s non-agency portfolio is even worse than that of Two Harbors. Nearly half of all the non-agency securitized mortgages were originated in California and Florida. Again, this means that the vast majority of them are collateralizing badly underwater properties.

Similar to the other mortgage REITs, Invesco is highly leveraged. The 10-K Report revealed that the debt-to-equity ratio was seven to one. Their liquidity position has deteriorated badly over the last three years. Cash and equivalents declined to a mere $164 million at the end of 2014. Because of the large net loss last year, they were able to pay out the annual dividend of $1.95 per share only by borrowing more than $1.2 billion.

Similar to AGNC, Invesco’s share price has not fared well in the last few years. It declined from a high of 24 in early 2011 to a little more than 15 on April 24. Given the serious problems with its non-agency portfolio, it could plunge much further.

Conclusion

Although analysts have paid little attention to these key fundamentals of the mortgage REITs, I am confident that the fundamentals and not interest rates will determine the long-term direction of mortgage-REIT share prices.

Is the yield that these mortgage REITs offer worth the extensive credit risks that your wealthy investor clients clearly face?

Given the serious problems facing the mortgage REITs, the prudent course of action is to sell them now. Exit doors are often narrow during a major decline. The safest course is to get out early.

Keith Jurow is a real estate analyst and former author of Minyanville’s Housing Market Report. His new report – Capital Preservation Real Estate Report – launched a little more than a year ago.

Read more articles by Keith Jurow