Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article original appeared on Doug Short’s site, www.dshort.com. It is a must-read follow-on to a two-part series by Ed Easterling. It discusses the ability of the Crestmont methodology for P/E and EPS, unlike other methods, to provide forward-looking insights for investors. Here are links to the previous articles: P/E: So Many Choices, Part I and Part II.

Ed's books, Unexpected Returns and Probable Outcomes, have Doug’s unqualified endorsement for anyone trying to understand the complex and often puzzling relationship between the economy and the market.

When you embark on a trip toward a desired destination, it is important to know your starting point and the path that you will take. For every investor, the destination is financial success. Wouldn't it be helpful to have a financial planning GPS, especially one with updates about market corrections to help you detour around the snarl? The reality, however, is that no such magic device exists and investment success requires old fashioned discipline and judgment.

Discipline starts with an assessment of the environment and a map of the journey. Ptolemy, a famous cartographer and astronomer almost 2000 years ago, drew horizontal and vertical lines around the globe to enable seafarers to navigate unknown waters using tools of the time. He created the parameters and framework that enabled ship captains to see their futures on the horizon. They no longer were destined to follow a path of hope; they could have strategies that empowered direction with insight.

The principles

Conventional wisdom holds that long-term forecasts of the stock market must be impossible because "even its short-term predictability is challenging." If you can't reasonably know what will happen next week or next year, how on earth are you to know what will happen next decade?

Well, there's a simple lesson from the forest. There are many factors that impact the growth of trees each year: rain, sun, temperature, and a host of other conditions.

Well, there's a simple lesson from the forest. There are many factors that impact the growth of trees each year: rain, sun, temperature, and a host of other conditions.

Ask any forester; all of those conditions make it impossible to accurately predict tree growth for any given year. Yet ask that same forester about the next decade and she will reach for the historical tables. They provide standards for tree growth over long-term decades. When a tree is ultimately cut and its rings are measured, the year-to-year variances average out to prove the reliability of the historical tables.

But every tree does not grow at the same rate under all conditions. The universal "average" is a fallacy. For example, trees of the same species grow at slower rates when confronted with altitude, colder temperatures, and reduced rainfall. Likewise for the stock market, it does not generate the mythical 10% average return under all conditions. There are fundamental principles and factors that cause stock market returns.

Stocks are instruments of ownership in companies that generate profits over time. Stocks are financial assets that have value because of future cash flows in the form of dividends and earnings. Today's value for a stock, and the stock market overall, is driven by future earnings growth and market rates of return.

It's almost that simple: if you can assess the likely growth rate for earnings and have an estimate for market rates of return, then forecasting the future of stock market returns is clearly on the horizon.

EPS growth

Earnings growth is driven by economic growth. Both factors have their own cycle. The economy, as measured by gross domestic product ("GDP"), fluctuates every decade or so through expansions and recessions. Earnings growth, almost like a moon around a planet, fluctuates around the economy's course. Profit margins expand, bringing the responses of competition and production, only to be followed by excesses in both that contract margins to rebalance conditions. But balance rarely occurs. It remains an occasional crossing point for ever repeating cycles. That's why investors need tools to assess the overall trend, lest they be destined to zig and zag aimlessly without a compass to help them focus on the horizon.

Therefore, to estimate future stock market returns, investors need measures of earnings growth and market valuation levels (as measured by the price-to-earnings ratio, "P/E"). The Crestmont methodology for earnings per share ("EPS") and P/E provides a tool not only to evaluate historical trends and results, but also to assess the course of the market and its future on the horizon. Crestmont's EPS and P/E are based upon regressions and relationships between historical EPS and GDP. Thus, with future estimates of GDP, Crestmont's methodology provides forecasts of EPS.

[dshort note: for more details, see P/E: So Many Choices, Part I posted on April 26.]

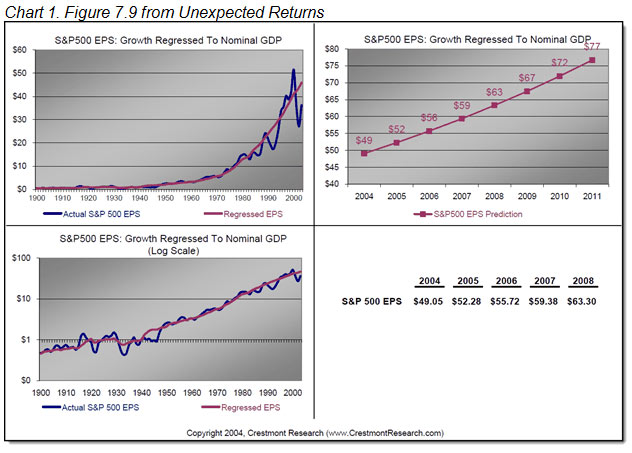

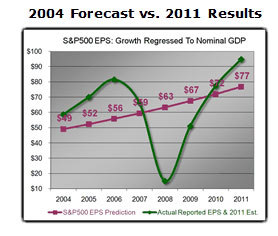

For example, when the methodology was discussed in Unexpected Returns (written in 2004 and published in 2005), Figure 7.9 provided a prediction for EPS through 2011 (presented as Chart 1 below). It was based upon a forecast for GDP that extended then-recent history into the future.

Note the upper-right graph; it provides an estimate for EPS from 2004 through 2011. It's ironic that we can now look back from the final year of a seven year old forecast to assess its credibility.

By 2006, the Wall Street pundits were laughing at the laggard line in Figure 7.9 as S&P 500 companies posted profits of more than $81 per share (compared to $56 on the chart). Their forecasts expected $100 per share within two years. It was as though the gravitational force of the business cycle had been conquered. The pundits led investors to see the Crestmont forecast as the old blue earth from outer space orbit, a remnant so far away that it was no longer relevant.

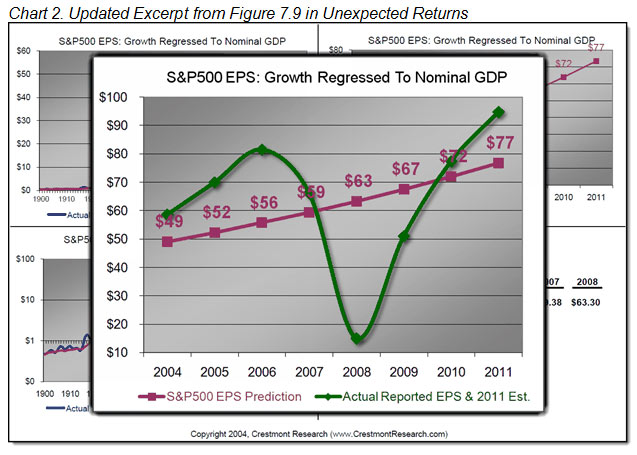

Two years later, the view for the trend line forecast had shifted — this time the pundits looked upward to see it (like the diver reaching for the water's surface). Chart 2 (below) presents the forecast chart from Unexpected Returns with an overlay of actual history through 2010 and the current forecast for 2011.

The pink line is the published forecast from 2004; the green line reflects what actually happened. It is very typical that the actual course of EPS, based upon many decades of history, zigs and zags around the natural course. Once again — today — the view is shifting and hope springs eternal on Wall Street. Reported EPS has surged past the base trend line ... and the current forecast by S&P calls for $99 in 2012. Maybe this time will be different (but I wouldn't bet on it!).

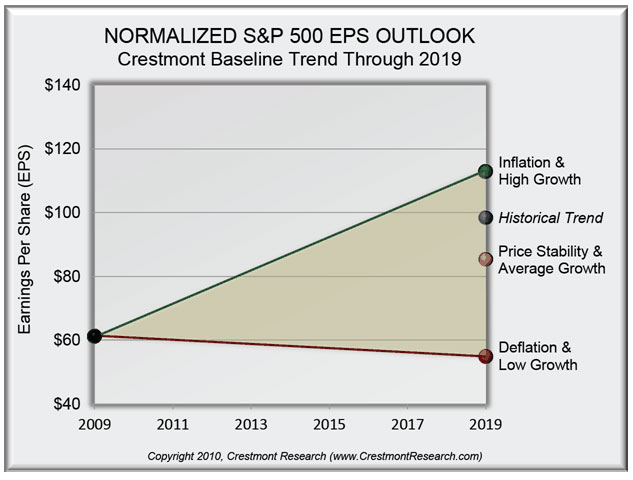

Subsequent to 2004, the forecast for future Crestmont EPS downshifted slightly (as did the trend line for some of the recent years). The earlier forecast for EPS was based upon historically average GDP growth. But the economy in the 2000s fell short, even before the recession of 2008. As a result, the current outlook is a combination of continuing the slow-growth trend and restoring the historical average. That's why economic growth is Major Uncertainty #1 in Probable Outcomes.

Nonetheless, the range in Chart 3 fairly well frames the baseline course for the rest of this decade. The actual path, however, likely will stray wildly; but, the natural line that drives market valuation tracks within the channel.

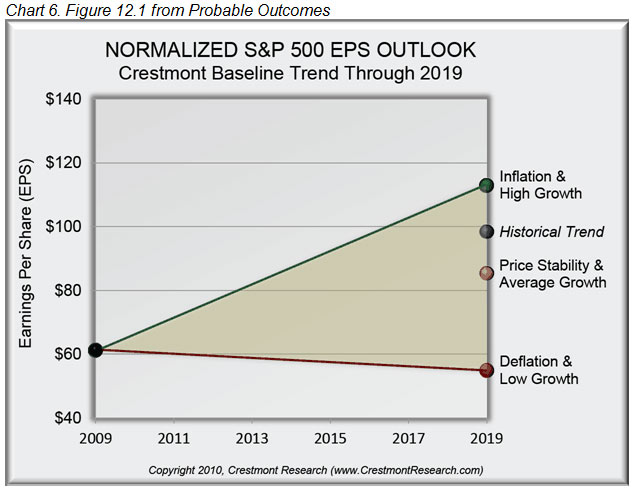

Chart 3. Figure 12.1 from Probable Outcomes

The shaded triangle reflects the results under various assumptions. The upper boundary line represents the most optimistic assumption for nominal EPS growth. This includes 4% real economic growth and rising inflation. The lower boundary represents the least favorable assumptions: 2% real economic growth and deflation. The most likely result will occur within the field. Two points are included on the right side for 2009. The first relates to historical growth and average inflation; the second is average growth and low inflation.

Most importantly, the shaded "field" is where the earnings game will be played. It can serve as a compass for EPS to keep in perspective the normal business cycle as well as the over-extrapolated forecasts from manic analysts. For example, as of today, currently reported EPS and forecasts for the next two years exceed the top boundary. Profit margins are high. Within the next few years, the power of the business cycle will realign EPS growth back to its natural course. Don't be surprised, by the way, if reported EPS dips below the lower boundary — the magnitude of swings in EPS from the business cycle are dramatic. That is why a normalized measure for EPS, especially one that is forward looking, is so important to investors.

P/E multiple

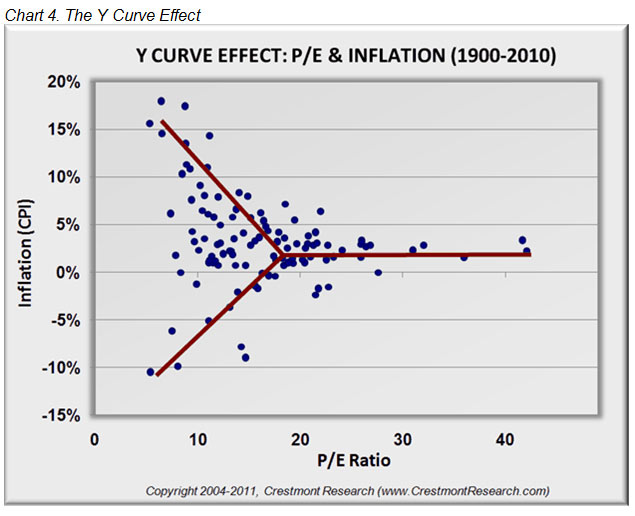

The price-to-earnings ratio ("P/E") is the major multiplier of stock market returns over time. Sometimes, however, the multiplication is a fraction rather than a whole number. When P/E rises over time, the increase in the multiple exponentially drives returns. This creates periods of above-average returns — the secular bull markets. Conversely, a decline in P/E over time offsets earnings growth and leads to periods of below-average returns — the secular bear markets. P/E, therefore, is a major factor for the ultimate course of the stock market.

P/E does not follow a random course; it is driven by the trend and level of the inflation rate. Chart 4 reflects the relationship of P/E and inflation. Periods of higher inflation or deflation drive P/E lower and periods of price stability (i.e., low and stable inflation) drive P/E higher.

[dshort note: for more details, see P/E: So Many Choices, Part II posted on April 27.]

This is important because it provides the framework to understand that P/E is not a random variable, but rather one that is subject to fundamental forces and principles. The change in P/E over time is not only one of the three components of stock market returns (dividends and earnings growth are the other two), it has the most significant effect on the variability of returns over decade-long periods.

P/E is not only driven by inflation, it is also driven by the long-term growth rate of earnings. Earnings growth over the long-term is driven by economic growth. Historically, real economic growth has been relatively constant across the decades averaging near 3%. As a result, P/E progressed from highs to lows based upon the inflation rate.

The range of highs and lows, from just over 20 to just under 10, was determined by the 3% economic growth constant. Had economic growth been lower, then the range and average P/E would have been lower. This paragraph cannot be emphasized enough — the implication is a game changer for P/E if the long-term future reflects lower economic growth.

The 2000s brought a period of economic surprise. The growth rate was not 3%. Conventional wisdom, based upon excessive leverage and unsurpassed American consumerism, holds that economic growth surged forward unsustainably. Supposedly, the U.S. is now expected to atone for that binge with a decade or more of slower growth.

But, real GDP growth in the 2000s was only 1.8%. Even before the 2008 recession, cumulative GDP was chugging along at 2.6% annually and did not exceed 2.7% annually during that decade. Therefore, and this is a major unknown, the economy may be positioned for a restorative above-average decade ... or it could have downshifted to a new lower level. This emphasizes why future economic growth is Major Uncertainty #1 in Probable Outcomes.

A 4% decade would simply get the economy back on track for its 3% trek. If the new economy provides only 2% growth, however, the impact is a downshift in the range for P/E. Note in Chart 5 that the inflation rate will continue to determine the position within the range, but the growth rate determines the level of lows and highs.

Chart 5. P/E Drivers: The Inflation Rate & The Growth Rate

Outcomes on the horizon

Most people expect P/E to measure current valuation and to show historical patterns. But more features are available from some versions of P/E. The methodology behind the Crestmont P/E enables investors to anticipate the future. It may not precisely predict the market ten years away, but it frames within a relatively tight range the likely outcome. One component from determining the Crestmont P/E is a means to assess the future trend line for EPS using estimates of future economic growth (GDP).

GDP growth over this decade, albeit somewhat uncertain, is highly likely to average within a fairly narrow range between 2% and 4% annually. The higher value of 4% reflects growth reverting to its long-term average. The lower value of 2% indicates significant drags on the economy. With population growth near 1%, even just a little productivity drives economic growth to 2%. Most pessimists predict between 2% and 2.5%. Most optimists hope for 3.5% or slightly higher. If you poll your favorite economists, the high odds-on range for average economic growth will almost certainly be 2% to 4%.

The other major factor for estimating stock market returns is a reasonable estimate for P/E in the future. From earlier principles, the primary driver for P/E is the inflation rate. Although the range of outlooks for inflation can be quite broad, there are three primary categories of outlooks. The first is higher inflation, the second is price stability (i.e., low inflation), and the third is deflation. For each category, there is an estimated P/E using The Y Curve and historical data.

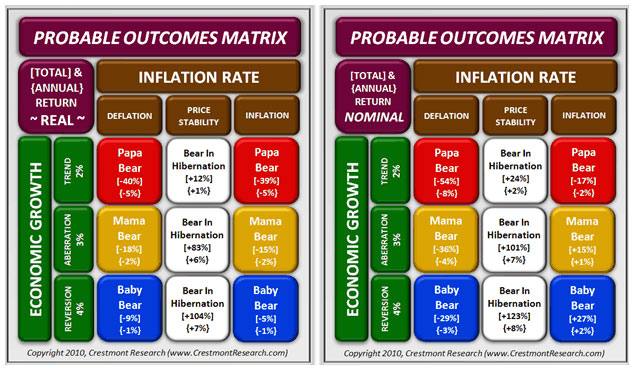

For ease of reference, Chart 6 repeats the earlier Chart 3 (which presents the range of EPS based upon various scenarios for GDP growth). Therefore, with three scenarios for economic growth and three scenarios for the inflation rate, there are nine composite scenarios for stock market outcomes. When the scenarios for P/E (from Chart 5) are applied to the scenarios for EPS (in Chart 6), and dividend yields are added to the results, the result is the Probable Outcomes Matrix in Chart 7!

Chart 7. Probable Outcomes Matrix: Real & Nominal Returns

This identifies the two major factors that drive stock market returns over the long-term. Certainly there are numerous other factors that impact these two, but the ultimate value of the stock market (i.e., the value of its cash flows), is determined by the growth in cash flows and the discount rate applied to those cash flows. The cash flows of companies emanate from earnings, which for the stock market overall is driven by economic growth. The discount rate, as reflected in P/E, is driven by the inflation rate.

These scenarios are useful in several ways. First, they frame the range of probable outcomes. That helps investors to structure their portfolios and financial plans. Although the scenarios reflect what is likely, they also tell us what isn't likely. For example, an average or better stock market return (i.e., the famous 10%) is highly unlikely for this decade (without another bubble of course). As investors consider various investments for diversification, alternatives with solid 6%, 7%, 8%, etc. return profiles can be quite attractive.

Some investors are afraid to miss the next secular bull market (longing for the 1980s and '90s again) and thus often shun such investments. They see them as anchors that compromise stock market portfolios. Yet in secular bear market periods, like today, those "anchors" may turn out to be engines!

With the right tools and reasonable assumptions, the future of stock market returns is on the horizon and visible to investors. There's no reason that anyone should look back in 2019 and say "who knew?" as savings underperform or dwindle. Institutional investors, especially, risk great burden if they rely upon unrealistic assumptions for returns. Early recognition, whether individuals or institutions, can enable smaller solutions in advance rather than major reactions in crisis.

Copyright 2011, Crestmont Research (www.CrestmontResearch.com)

Ed Easterling is the author of recently-released Probable Outcomes: Secular Stock Market Insights and award-winning Unexpected Returns: Understanding Secular Stock Market Cycles. Further, he is President of an investment management and research firm, and a Senior Fellow with the Alternative Investment Center at SMU's Cox School of Business where he previously served on the adjunct faculty and taught the course on alternative investments and hedge funds for MBA students. Mr. Easterling publishes provocative research and graphical analyses on the financial markets at www.CrestmontResearch.com.

Read more articles by Ed Easterling

Well, there's a simple lesson from the forest. There are many factors that impact the growth of trees each year: rain, sun, temperature, and a host of other conditions.

Well, there's a simple lesson from the forest. There are many factors that impact the growth of trees each year: rain, sun, temperature, and a host of other conditions.