Key Points

- With stocks hitting their highest levels in over five years, we may finally be seeing the long-awaited shifting of investor attitudes toward equities that could bring a lot of cash into the market. However, we don't believe attitudes change on a dime and there are plenty of potential bumps in the road.

- The debt ceiling debate was pushed into at least May but with the spending sequesters scheduled to take affect next month, rankling in Washington seems sure to continue. A debate of sorts also appears to be growing at the Fed as they begin to contemplate exit strategies in the face of some improvement in economic conditions.

- Europe has made enough progress that we are upgrading our investment outlook, while also watching Japan's ability to further weaken the yen. China should bounce in the near-term but risks are elevated and we are growing more concerned.

January started off the year with a bang as stocks hit their highest levels since 2007. Combined with some calming of macro headwinds, including the fiscal cliff, European debt crisis, Mideast violence, etc., conditions have triggered the start of some sidelined cash moving into equities. We've seen some nascent signs of this as flows into equity funds in January are estimated to be up over $30 billion according to the Investment Company Institute (ICI) and ISI Group. These are the best monthly inflows since before the financial crisis. While certainly not enough to call it a trend, it is a start, and with stocks continuing to move higher, the long-awaited shift in investor attitudes may be occurring.

Will new highs push investors into stocks?

Source: FactSet, Standard & Poor's. As of Jan. 25, 2013.

If this shift were to take hold, we believe it could lead to further gains in stocks as investor money that has continued to flood into fixed income and cash vehicles begins to shift more toward the equity markets. However, even though this is a change we have been anticipating, we don't believe investor sentiment will turn on a dime and there will undoubtedly be bumps along the way. In fact, after the recent run, optimism as measured by a variety of sentiment indices, has moved toward historical highs. According to Ned Davis Research's Crowd Sentiment Poll, sentiment has reached the extreme optimism zone, which is typically a contradictory indicator, meaning the possibility of a near term pullback is elevated.

Economy and earnings picture…average.

With fourth quarter 2012 earnings season now largely complete, the results were fairly positive. The beat rate (percentage of companies reporting better-than-expected earnings) was largely inline with historical averages while commentary surrounding the announcements continued to be mostly guarded, with many companies expressing the ubiquitous "cautious optimism" as they looked into the future.

And that sentiment appears supported by the incoming economic data. Retail sales results from the all-important December time period showed a nice 0.6% rise in sales ex-autos and gas; indicating that consumers appear to be willing to continue to spend, even in the face of the impending fiscal cliff. However, although the tax part of the cliff was largely avoided, payroll taxes were increased by 2.1%, which equates to roughly $1,000 for every $50,000 in income up to $113,700. Additionally, income taxes did go up on upper income earners. According to the Bureau of Labor Statistics, and pointed out by our friends at Bank Credit Analyst, the top 20% of earners account for 40% of total consumption, suggesting the consumer could be impacted more than is currently believed. As a result, we recently downgraded the consumer discretionary sector (see Schwab Sector Views for more info.)

But there are some offsets for the consumer and we don't believe the economy is in for a sharp reduction in growth. Home sales and prices continue to improve, which help in a variety of ways, including construction, consumer confidence, job growth, the ability of jobseekers to move, etc. Interestingly, existing home sales were down 1% in the most recent reading but it appears that is due to a lack of inventory—quite a change from the past several years. In fact, at the current rate of sales, the inventory of existing homes available for sale is only 4.4 months, the lowest level since 2005.

There was also some concern over the -0.1% gross domestic product (GDP) growth rate posted for the fourth quarter. Although certainly not a forward-looking number, slipping back into contraction is definitely not what investors were expecting. However, the internals of the number actually paint a significantly better picture as much of the decline was attributed to government spending falling 6.6%, subtracting 1.3 points from growth; and inventory contraction, which subtracted 1.3 points from growth, but it may help to support the economy in the future. Encouragingly, residential investment jumped 15.3%, equipment and software spending was up 12.4%, and the all important personal consumption spending number was up 2.2%—all supportive of a growing economy despite the headline number.

We've also seen the job market continuing to improve, with jobless claims recently hitting their lowest level in five years. And while this could be partially attributed to relatively mild weather, it is still encouraging. Further confirmation of the continued improvement in the jobs market came from the Labor Report, which showed 157,000 jobs were added in January, while the previous two months were revised higher by 127,000 jobs, although the unemployment rate did tick up to 7.9%.

There is also a bit of concern surrounding the manufacturing sector as recent regional surveys have been mixed at best. Attention will now be focused on the national readings and they are increasingly important, especially for manufacturing, since it's been one of the major factors helping to lead the US expansion as of late. And there is some encouraging news on that front as the Institute for Supply Management's Manufacturing Index surprisingly moved to 53.1 in January from 50.2. And we are also encouraged that the Index of Leading Economic Indicators surprised on the upside by rising 0.5%.

Leading Indicators continue to indicate growth

Source: FactSet, U.S. Conference Board. As of Jan. 25, 2013.

The Fed debates next steps, while slow "progress" is made in Washington

The most recent Fed meeting left policy unchanged but we are hearing more comments by Fed officials about how they will begin to normalize monetary policy in the face of improving economic data. Given that inflation remains tame for at least the time being (core CPI was only up 1.9% year-over-year in December), they appear to have some flexibility in gradually exiting their current quantitative easing programs, giving the market ample time to adjust. It still appears that Chairman Bernanke is determined to avoid a move that may end up derailing the recovery. He has noted before that mistakes have been made historically by the Fed and other central banks when they've exited accommodative positions prematurely, resulting in hard-fought progress being unwound.

And hard fighting is what we are looking for in Washington as we approach the new March 1st deadline on the spending sequestrations as well as the new fiscal budget. The cobbling together of an agreement to avoid the brunt of the fiscal cliff and push the debt ceiling debate off until May, these are still simply kick-the-can "solutions," when what the country really needs is a credible solution addressing spending and entitlement growth, while also having a plan to remove impediments to economic growth.

An upgraded view on the Eurozone

As noted, some calming of the eurozone debt crisis appears to be contributing to the increasing confidence among investors, after seeing outbreaks wreak havoc with confidence and markets for several years. Things appeared to turn when European Central Bank (ECB) President Mario Draghi uttered the famous words "do whatever it takes" to preserve the euro in July 2012; and put in place a conditional bond purchase program two weeks later.

Although no action has been taken, as no country has asked for assistance, credit markets have thawed. The ECB's safety net has given markets confidence that if yields spike, the ECB will be ready to buy government bonds, therefore bringing yields back down. Indeed, it appears talk is cheap but valuable—the mere existence of a credible lender of last resort has restored confidence.

Despite the well-known negatives, positive developments are the eurozone's largely untold story. Labor reforms have reduced unit labor costs in Spain, Greece and Ireland, improving competitiveness. As such, manufacturers such as Peugeot, Ford and Renault have discussed expanding or maintaining factories in Spain while closing elsewhere. Current account deficits in the periphery are shrinking; and adjusting for cyclical factors, most peripheral countries are expected to have primary budget surpluses (fiscal surplus before interest expense) in 2013 according to the International Monetary Fund (IMF).

January brought potential relief for Europe's credit crunch, because Basel III capital requirements for banks were delayed by four years. The rules will be less strict when they do take effect and can be considered a de facto easing of monetary conditions. We still believe banks need additional capital and will deleverage, but less urgently. Meanwhile, credit markets have opened for banks, corporations and peripheral governments, with strong demand for new issuance in 2013, potentially reducing the economic headwind from lackluster bank credit. Demand is coming from investors searching for yield, potentially shifting away from safe havens. The improved sentiment has extended to currencies as well, with the safe-haven Swiss franc finally weakening in 2013 and the euro has risen against most currencies.

Despite expectations the eurozone recession will continue in coming months with downside risks, there is the possibility the economic drag in 2013 will be less severe than in 2012. The eurozone composite PMI is in contraction territory, but has risen for three straight months—contracting at a slower pace, and the Bloomberg consensus estimate is for eurozone GDP growth to improve to -0.1% in 2013 from -0.4% in 2012. The biggest fiscal adjustments have likely already occurred, while future adjustments may be smaller in comparison. Policymakers are starting to appreciate the fallacy of austerity—that overly harsh austerity only makes matters worse, resulting in a negatively reinforcing spiral. As a result, deficit-reduction goals are being extended to more realistic timeframes. Lastly, global growth is improving, which is likely to accrue to Europe's benefit as well.

Risk may arise from the upcoming Italian election on February 24-25, as new leadership could shift to anti-austerity, anti-reform in nature, and undo progress. Despite the likelihood for drama due to the re-emergence of former Prime Minister Berlusconi, we believe the most likely outcome is a fragmented vote that will need a coalition, resulting in stalemate and little change to policy. Additionally, Cyprus' stalled bailout could raise concerns if it results in another debt "haircut," but we think this is unlikely.

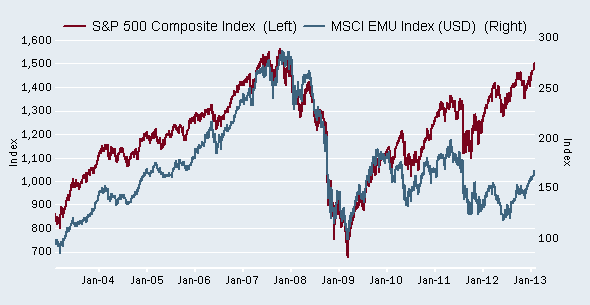

Eurozone stocks have underperformed

Source: FactSet, Standard & Poor's, MSCI. As of Jan. 29, 2013.

Our sentiment toward the eurozone has improved with the thawing in credit markets, potential credit crunch relief, reduced global uncertainty and possible reacceleration in growth in the eurozone, as well as still-depressed earnings and valuations; and we believe the time is right to move to a positive view on European equities. There are still downside risks, but they don't appear to outweigh the potential upside.

Don't fight the Bank of Japan?

A majority of Japanese equities' past underperformance has been correlated with yen strength. According to BCA Research, from 2002 to late 2012, the Nikkei 225 Index in US dollar terms generated returns fairly close to the S&P 500 Index and there is a high inverse correlation between the yen and the Nikkei's relative performance.

Japanese stock performance inverse to yen

Source: FactSet, Nikkei Stock Exchange, MSCI, Reuters. As of Jan. 29, 2013.

* Indexed to 100 as of Jan. 29, 2003. A larger (smaller) number above 1 denotes greater outperformance (underperformance) of the Nikkei relative to the EAFE Index.

Despite entrenched headwinds for the Japanese economy and its corporations, equity investor sentiment has improved. The shift appears due to the economic policies ushered in by Japan's new Prime Minister Shinzo Abe. A weaker yen forms the basis for his policies, dubbed "Abenomics." As such, the yen has weakened dramatically, falling 12% relative to the US dollar since elections were called on November 14, while the Nikkei 225 Index has risen 13% in yen terms and 9% in US dollar terms.

The BoJ meeting on January 22 was somewhat disappointing, because while the BoJ adopted "open-ended QE" and a 2% inflation target, additions to the asset purchase plan were tabled for a year. Regardless, yen pessimism and stock optimism quickly returned after a three-day reprieve.

The view is that January's meeting may be the first step in a more aggressive campaign yet to come after new governors are put in place in April. However, this view is nearly consensus, and thus somewhat dangerous, but we also believe that it's hard to fight. If the BoJ convinces markets it will do "whatever it takes" to weaken the yen, it may become self-fulfilling. If the BoJ stays aggressive, Japanese stocks are likely to benefit from a declining yen, giving us the mantra "don't fight the BoJ." However, relative dollar strength would reduce returns for US investors and investors may want to consider hedging currency exposure.

China's recovery excites, for now

China's economy is rebounding, led by infrastructure spending. However, China's recovery has been accompanied by a surge in speculative debt from the shadow banking sector that has similarities to the subprime credit bubble in the United States, as we detail in our article. As a result, China's risk profile is increasing and the economy is becoming more vulnerable, with risks increasing over the next three years.

Chinese-related investments could continue to benefit from the economic turnaround in the near term. However, longer-term investors may want to consider beginning to re-orient international exposure away from China and toward developed markets.

Important Disclosures

The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The MSCI EMU (European Economic and Monetary Union) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of countries within EMU. The MSCI EMU Index consists of the following 11 developed market country indices: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal, and Spain.

The S&P 500 Composite Index® is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

Manufacturing Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Japan Nikkei 225 Index is a price-weighted index comprised of Japan's top 225 blue-chip companies on the Tokyo Stock Exchange.

Ned Davis Research (NDR) Crowd Sentiment Poll® shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

Past performance is no guarantee of future results.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. This report is for informational purposes only and is not a solicitation or a recommendation that any particular investor should purchase or sell any particular security. Schwab does not assess the suitability or the potential value of any particular investment. All expressions of opinions are subject to change without notice.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab