Key Points

- US stocks continue to make new highs, yet commodities have struggled and Treasury yields remain low, albeit up from recent near-record lows. Although not the standard playbook, we remain optimistic but acknowledge an equity pullback can occur at any time.

- Manufacturing data has been soft, the employment picture is mixed, and housing continues to improve. We believe the US economy will continue on a modest upward path, with acceleration possible in the second half of the year.

- The European Central Bank (ECB) has joined the easing party, illustrating the continued disappointments coming out of the eurozone. Meanwhile, Japan may be gaining some traction from monetary easing, but we remain cautious about China.

Sell in May and go away?

Although the past three years brought economic slowdowns and meaningful market corrections, knowing exactly when to exit and re-enter the market was a difficult task. We wouldn't suggest trying to time around any possible pullback in the near-term because remember, you have to get the timing right twice (out and back in). Stocks have had a relatively uninterrupted run and investor memories of previous May pullbacks can certainly become a self-fulfilling prophecy. But we would view pullbacks as buying opportunities for investors needing to add to equity exposure. For those already fully invested, instituting a hedging strategy might be prudent.

Economic picture muddled

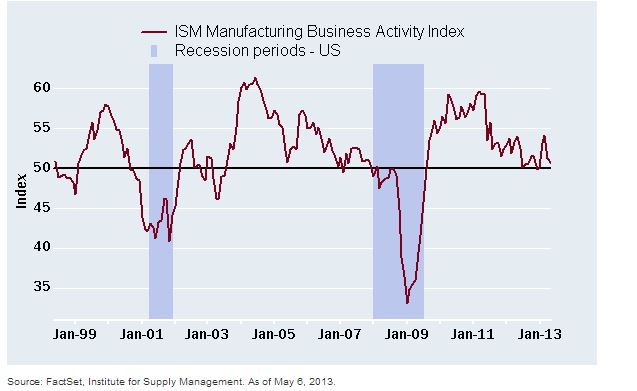

We're going through another soft patch although it's likely to be less pronounced than those in the past three years. But the weakness is not across economic sectors. Manufacturing has softened, with the Chicago PMI falling to 49 from over 52; territory depicting contraction. It joined declines in other regional surveys such as the Empire Manufacturing Index and the Philly Fed Index. The national Institute for Supply Management (ISM) Manufacturing Index told a similar story, dipping to 50.7 from 51.3, barely hanging above the dividing line of expansion and contraction.

Manufacturing soft spot?

Within the ISM report, there were conflicting signals as new orders encouragingly rose to 52.3 from 51.4, while employment disappointingly fell to 50.2 from 54.2.

The jobs picture is showing signs of life. ADP reported that private payrolls rose by a mere 119,000 in April, while the previous month was revised lower. But the broader payroll report from the Labor Department painted a more positive picture as 165,000 jobs were added in April, while the previous two readings were revised sharply higher. Additionally, the unemployment rate fell to 7.5%, the lowest since 2008. The labor force participation rate remained at 63.3%, which is the lowest level since 1979, mostly explained by demographics, but also driven lower by people dropping out of the labor pool due to weak job prospects. And, in another sign of some hits coming from the Affordable Care Act, average hours worked declined, reflecting a bias by smaller companies to shift toward part-time workers. More encouraging were initial unemployment claims, which just hit its lowest level in nearly five years.

The dominant service side of the economy is doing modestly better as the ISM Non-Manufacturing Index declined to a still decent 53.1 from 54.4; while the forward-looking new orders component stayed roughly steady at a healthy level of 54.5.

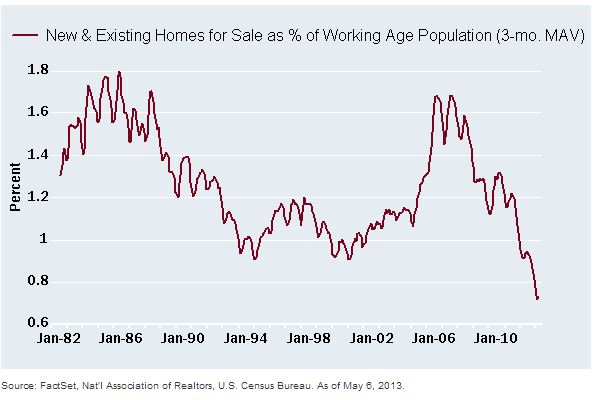

One of the biggest supports to the economy this year continues to be housing, with the S&P/Case-Shiller Index showing prices rose 9.3% in February, which was the biggest gain in almost seven years. And, all 20 cities measured within the index are now experiencing price increases. With the colder-than-usual spring through much of the county potentially impacting activity, we look for continued improvements, although record-low inventories may cause some lumpiness in the rate of sales growth.

Housing inventories are at record low

Housing, combined with a strong stock market, has led to household net worth likely hitting an all-time high as of the first quarter, which should help. Increasing consumer demand, aided by lower energy and other commodity prices, would put more pressure on companies to invest in capital improvements and increase the hiring rate; a situation we believe will develop in the second half of the year.

Missing both sides of the dual mandate?

The Federal Reserve is now facing deflation fears, meaning neither of the Fed's mandates (inflation or jobs) is near the Fed's thresholds. As a result, it continues its extremely accommodative monetary policy, pegging target rates near zero and continuing to buy $85 billion per month in mortgage-backed and Treasury securities. The Fed also added a slightly more dovish tint to its statement by noting it could adjust the amount of purchases both down or up as needed. There continues to be an apparent "Bernanke put" of sorts on the stock market that has at least temporarily benefitted investors. As they say, "Don't fight the Fed."

Politics lessening impact

The fighting in Washington has calmed and policy risk has lessened for the markets. We continue to believe the payroll tax increase has now been absorbed in the economy, while spending cuts continue to filter through, dragging down economic growth. And, while other issues have dominated discussion as of late, the economy will likely move to the front again as the debt ceiling and next year's budget debates begin. The Affordable Care Act continues to draw derision from many that could force changes that would impact the economy. The hit and uncertainty is particularly troublesome for smaller companies.

Global data mixed

The United States isn't alone as global data is also giving mixed signals. Commodity prices of industrial raw materials have declined this year, raising doubts about global growth. However, the story is complicated by rising supplies in recent years and China slowing at the margin. Currencies of commodity-oriented countries such as Canada and Australia have also started to weaken.

Negatively, the global manufacturing purchasing managers index (PMI) fell 0.7 points in April to 50.5; however the share of countries posting gains increased, suggesting a soft patch, rather than a renewed downtrend.

Global growth trend uncertain

Stock and debt markets have taken the "glass half full" view, enhanced by the flood of central bank liquidity. Relative to six months ago, the Bank of Japan is a new, and very large, addition to global liquidity. This liquidity will boost many assets, but the trends and catalysts across countries and companies create divergent investment opportunities.

Is Europe confined to depression?

The timing for economic recovery in the eurozone has been pushed out, with the recent negative data including:

- Weak credit, with loans to non-financial corporations down 1.3% in March and loans to households up a weak 0.4% relative to a year ago.

- The unemployment rate for the eurozone as a whole is at a record 12.1%, with significantly higher readings among the peripheral countries.

- Inflation softened to 1.2% in April, prompting the investors to weigh the prospect of deflation.

However, not everything is negative and the eurozone is getting a double dose of relief, both in terms of monetary policy easing and a smaller fiscal drag.

- The European Central Bank (ECB) cut the benchmark interest rate, and non-standard additional measures are being considered.

- The fiscal drag in 2013 will likely be less severe than in 2012. In May, the European Commission granted France and Spain two more years to cut public deficits to below 3% of GDP.

There have been other notable headlines that could boost Europe's outlook:

- Germany announced a plan to boost investment in smaller companies in Spain.

- Germany's Finance Minister Schaeuble signaled a softened stance towards a banking union, saying it was a "priority project" and vowed to proceed "quickly."

- Demand for credit for working capital purposes recently increased for the first time since 2011, according to the ECB, a signal that companies may have more confidence about demand rebounding.

Negative stories about the eurozone abound, but investors may want to consider the story less told, which is that progress, albeit slow, is being made. Structural reforms such as increasing labor market flexibility have started, and the benefits will accrue over time. Earnings and valuations for eurozone stocks are still depressed, and a fair amount of bad news has likely already been priced in. Despite 54% of the STOXX Europe 600 Index companies missing first quarter earnings estimates, stocks rose 0.9% on average the first day of reporting, according to Bloomberg data through May 7.

Seeing results in Japan

Japan is the relative bright spot globally and while the focus has been on the effect of the Bank of Japan's (BoJ) actions on the yen, we may be entering a second phase for stocks, driven by benefits for the real economy and corporate profits.

One underappreciated fact about Japan is that consumers are 60% of the economy. Just like the Fed's QE, an aim of the BoJ's asset purchases is to encourage investors to move into riskier assets. The rise in stock and property prices results in a wealth effect, which can improve confidence, spending, profits and jobs in a positive virtuous cycle. Consumer spending has responded, rising 5.2% in March; the highest year-on-year growth in nine years. Excluding the effects of a tax increase in 1997 and the 2011 earthquake, sales at large retailers posted the biggest gain in 20 years, rising 2.4% according to the Financial Times.

Japanese consumer spending responding

Earnings estimates for the Nikkei 225 Index continue to rise; forecasted to increase 16% in fiscal year 2013 and another 19% in 2014, according to the Bloomberg consensus.

There are risks to the BoJ's policy, particularly as a weaker yen raises the prices of imports such as energy and food, which could crimp both consumer spending and corporate profits, and the dramatic moves in the yen and Japanese stocks are subject to reversals. However, stocks could benefit over a multi-year period, giving us the phrase "Don't fight the BoJ." Hedging the decline in the yen may become less important going forward if the yen finds a level of stability.

China tightening?

The softening in China's first quarter GDP raised the question of whether fiscal stimulus may be forthcoming. However, in a way, we're seeing fiscal tightening in China. The country's new leadership is on a campaign to reduce inequality and broaden wealth distribution, both for individuals and corporations, sacrificing near-term growth for reforms and structural rebalancing.

- On the corporate side, new Premier Li said that all companies should compete on level ground, suggesting that preferential policies are gradually rolled back for state-owned enterprises.

- Fiscal tightening is evident in the government's frugality and anti-corruption campaign, reducing spending on luxury goods, restaurants and other related businesses.

The yuan has garnered attention as the currency received a boost from exporters evading capital controls to bring money into China, expecting the yuan to continue to rise. Elsewhere, the government said it will crackdown on these exporters, as well as provide a plan for yuan convertibility this year, as a part currency and interest rate reforms.

Investor sentiment could get a boost as global stock index developers are considering adding China's domestic stock market as investable, raising China's index weight. Targeted fiscal stimulus is also possible, which could include spending on migrants if residency reform is undertaken, as well as spending on infrastructure.

However, we've noted our concern about the sustainability of China's debt-fueled growth, and believe China-related investments will encounter difficulty until investors have confidence about where and how China's economy stabilizes. Read more in our article "Avoid China – Subprime-Like Bubble Brewing", as well as related topics at www.schwab.com/oninternational.

So what?

Trying to time the market is always a difficult proposition and this time is no different. We continue to believe that the US equity market is an attractive place to be although elevated optimistic sentiment suggests a pullback could occur at any time. More adventurous investors may look to Europe to try to take advantage of some attractive valuations.

© Charles Schwab

![]()

![]()

![]()

![]()