Everybody Wants Some: Central Banks and Bond Funds Step up Buying of Stocks

Key Points

- The stock market has broken out of its "triple top" formation, which started in 2000, yet remains reasonably valued.

- Supply within the stock market has been dwindling thanks to near-record company buybacks.

- Demand for stocks is coming from some seemingly unlikely sources: global central banks and bond mutual funds.

It's probably no surprise that a common question I hear these days is, "Has the stock market come too far too fast?" There are underlying questions as well, including "If it's not retail investors buying (they're not, at least not aggressively), who is doing the buying?"

I'll tackle a component of the latter question in today's report and focus particularly on some of the more interesting buying forces present today. In short, some of the biggest recent increase in stock buying has come from foreign central banks as well as bond mutual funds (yes, you read that right). Along with the increased demand has come decreased supply courtesy of stock buybacks.

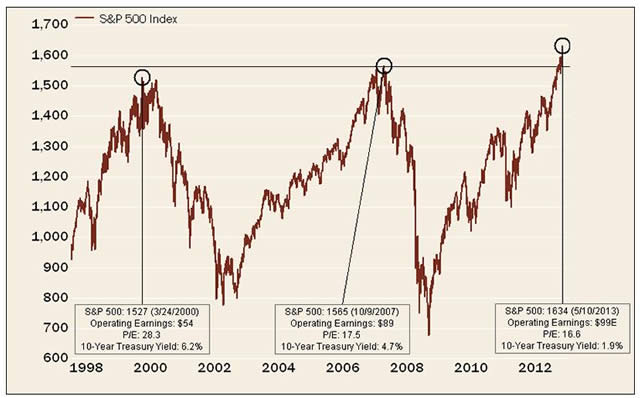

Triple top breakout

Indeed, there remain traditional supports for the market's advance, notably very strong earnings and still-reasonable valuations—this can be seen in the chart below, which shows the S&P 500® Index having broken out of the "triple top" formation. Compared to both the 2000 top and the 2007 top, earnings are notably higher, valuations more reasonable and interest rates (and inflation) much lower.

S&P breaking out

Source: FactSet, Federal Reserve, ISI Group, Standard & Poor's, as of May 10, 2013.

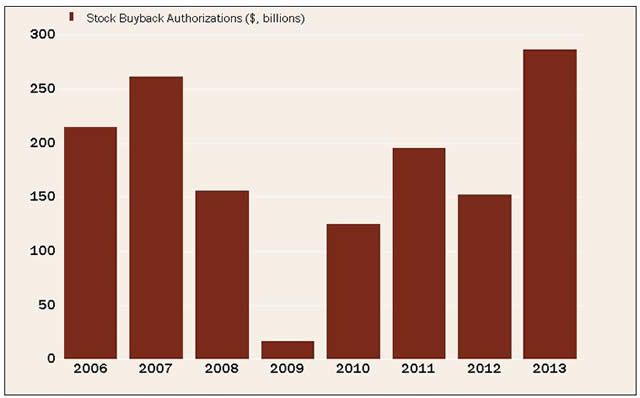

As for supply…

Supply has been dwindling, thanks to a big increase in stock buybacks. According to Birinyi Associates, there were $78.1 billion in buyback authorizations during the month of April. That brings the year-to-date total to $286 billion, the strongest start to a year in the history of their data. It's an 88% increase from the $152 billion recorded in 2012 and the 340 total authorizations this year is 26% higher than last year's 269 authorizations.

Stock buybacks surging

Source: Birinyi Associates, Inc., FactSet. Data is year-to-date through April for all periods.

The month of April was the strongest April Birinyi has ever recorded, due in large part to a $50 billion authorization by Apple (the largest ever by a company). The year is on pace to record $859 billion in authorizations, nearly in line with 2007's record $863 billion.

As for demand…

Last month, Central Bank Publications and Royal Bank of Scotland Group Plc conducted a survey of 60 central bankers. Nearly 25% of respondents said they own stock shares or plan to buy them. The Bank of Japan, featured heavily in the news recently and holder of the world's second-largest level of reserves, said it will more than double investments in stock exchange-traded funds by 2014. The Bank of Israel bought stocks for the first time last year, and the Swiss National Bank and Czech National Bank have upped their holdings to at least 10% of reserves.

Of the 60 banks surveyed, 14 said they'd already invested in stocks or would do so within five years. In fact, this is the first time ever the question about stocks has been in this annual survey.

Behind the heightened interest in stocks are growing central-bank reserves requiring increased diversification. In US dollar terms, the four largest central banks have expanded their balance sheets to more than $13 trillion, compared to only $3 trillion 10 years ago. Most central banks have had heavy and consistent reliance on fixed-income securities, but with yields low (and falling) in many countries, keeping all reserves in fixed income risks a declining value of reserves.

However, 70% of the central banks in the survey (including the US Federal Reserve) indicated that stocks remain "beyond the pale." A few central banks, including the Fed and the Bank of England, have no mandate to purchase stocks directly.

Jim O'Neill, chairman of Goldman Sachs Asset Management, weighed in: "I don't think people should worry about (central banks owning stocks). Frankly, it makes a huge amount of sense in a world of floating exchange rates and such incredible opportunity, why should central banks keep so much money in very short-term, liquid things when they're not going to ever need it?"

Should we call them "stond" funds?

The number of bond mutual funds that own or are buying stocks has surged to its highest point in 18 years, according to Morningstar (see the past 10 years in the chart below). A caveat: although the number of bond funds buying stocks is at an all-time high, the percentage has remained fairly stable relative to the number of bond funds overall.

Bond and income funds have more leeway to invest in other securities than many people might believe. The Securities and Exchange Commission does require funds to invest at least 80% of their assets in the type of assets suggested by their names; however, vaguer terms like "income" or "value" do not trigger the requirement.

Bond funds become big stock buyers

Source: FactSet, Morningstar Direct, as of December 31, 2012

Russ Wermers, an associate professor of finance at the University of Maryland, has been at the forefront of recent research on the subject. He notes that many bond-fund managers think of stocks as simply the lowest rung in a company's capital structure, below corporate bonds, preferred stock and/or other debt. As a company's bonds become more expensive (as yields decline), its stock starts to look like a better value by comparison. In that way, it can make sense for bond-fund managers to consider reaching down into stocks.

The trend is easy to understand when considering the quandary many fixed-income investors face. There's been a bull market in bonds for more than 30 years, and yields, which move in the opposite direction of prices, are near record lows.

In sum

The market has yet to attract high levels of interest from traditional individual investors, but that hasn't kept it from consistently surpassing all time highs since March. Look a little further and you'll find that keen interest in stocks has come from a couple of interesting buyers, while at the same time, supply has been dwindling thanks to near-record buybacks.

© Charles Schwab

![]()

![]()

![]()

![]()