Key Points

- Manufacturing/energy renaissance in the United States is a long-term theme; not a short-term trade … but it's underway

- The list of companies "reshoring" to the United States are powerful and growing

- Can the United States become a global exporting powerhouse?

Since I began chronicling, several years ago, the manufacturing and energy "renaissance" the United States is beginning to enjoy, I am regularly asked for an update. In fact, when I was recently in London for a week of client and media events, it was the hottest topic of discussion. Before I get to the latest details, let me remind readers that this theme is just that- a theme; and a long-term one at that. It is not a short-term investment or trading idea.

Given the latest reading on manufacturing from the ISM survey, which was weak, I thought it was a good time for an update on whether the longer-term themes remain intact. In short, I believe they do.

AMCHAM epiphany

As a reminder, I became very enthusiastic about the notion of manufacturing business coming back to the United States from China and other emerging economies as a result of conversations I had at two AMCHAM (American Chamber of Commerce) events in Beijing and Shanghai about six years ago. At each event, at which I did the keynote talk, I had several members approach me to suggest I keep my eyes and ears open to some budding trends they were seeing in China - notably that conditions were changing such that they were considering moving some or all of their China-based business back to the United States.

The key reasons this "manufacturing renaissance" has begun to unfold are numerous and include:

- Restrained US labor costs

- Emerging economies' accelerating wage increases

- Abundant US energy/low natural gas prices

- US labor market stability/flexibility

- US rule of law

- US economic/accounting transparency

- Better US demographics relative to many emerging economies

- Deep/liquid US capital markets

- Well-developed US infrastructure

- Better inventory control in US

- Eurozone/China economic uncertainty

Boston Consulting Group (BCG) has been at the forefront of researching the theme; starting with their initial report in 2011 titled Made in America, Again. Last year, BCG followed up with US Manufacturing Nears the Tipping Point.

In the latter report, BCG highlighted seven industry groups accounting for two-thirds of US imports from China that are nearing the point where it will be more economical to manufacture some goods in the United States. Combined with higher exports, this could result in the addition of two-to-three million jobs and $100 billion in annual output in this decade. The seven industries are:

- Transportation goods

- Computers and electronics

- Fabricated metals

- Machinery

- Plastics and rubber

- Appliances and electrical equipment

- Furniture

Drilling down further, I'm often asked for specific examples of companies that are making the shift and/or considering it, so I've been collecting data (thank you ISI and Cornerstone) and can share a list of companies that have either moved some business back to the United States from overseas; or in the case of foreign companies, are setting up shop in the United States. The list includes companies that have announced they are planning to move business back to the United States. These by no means constitute investment recommendations.

- Caterpillar

- Electrolux

- Apple

- Nissan

- Boeing

- KitchenAid

- NCR

- GE

- Bison

- Yamaha

- US Steel

- Siemens

- Ford

- Emerson

- Continental AG

- Volkswagen

- Airbus

- Chevron Phillips

- Maserati

- Samsung

- Exxon

- Toyota

- Michelin

- Lenovo

- Honda

- Smith Electric

- Otis Elevator

- Kia

- GM

- Stanley Furniture

- Intel

- Rolls-Royce

- Timken

- Whirlpool

- Starbucks

- Master Lock

- Huntsman

- Dow Chemical

Reshoring

In addition to BCG, The Hackett Group has done several surveys on the manufacturing renaissance theme and concludes that "reshoring" is expected to become more viable with each passing year. This is largely thanks to the rapidly shrinking "total landed cost gap of manufacturing offshore." The cost gap between the United States and China has shrunk by nearly 50% since 2004, and stands at about 16% today. This trend is largely driven by rising labor costs in China, as well as rising fuel prices globally, which affects shipping costs.

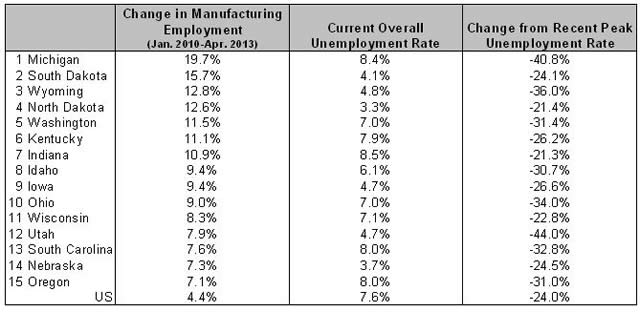

We can see the effects of the better manufacturing landscape at the state level most clearly. The table below highlights the top 15 most manufacturing-oriented states and their growth in manufacturing employment.

Source: Cornerstone Macro LP, Department of Labor, FactSet, as of April 30, 2013. US data as of May 31, 2013.

In fact, even though manufacturing has taken a hit in the past few months; notably with the ISM Manufacturing Survey dipping below the expansion-contraction line of 50 last month, the longer-term trends are encouraging.

The US manufacturing sector is actually the most profitable and productive of any time since World War II (WWII). In fact, as you can see below, manufacturing has grown as a percentage of US gross domestic product (GDP) for three years in a row-- the first feat of its kind in the post-WWII era.

Manufacturing's first "triple"

Source: Bureau of Economic Analysis, FactSet, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2013 © Ned Davis Research, Inc. All rights reserved.), as of December 31, 2012.

May the force be with US

And the United States is setting itself up to be a bigger global export force. In a report last year in The American Interest, Tyler Cowen, a professor of economics at George Mason University notes that "American manufacturing employment has been badly hurt by the mobility of capital seeking lower production costs abroad, but the growing wealth of foreign populations in rising economies is creating new demand for imports, including imports US workers can supply.Where are these exports likely to come from? Cowen cites three forces likely to combine to make the United States an "export powerhouse:"

1) Artificial intelligence (AI) and computing power are the future, or even the present, for much of manufacturing. The next steps in the AI revolution will revolutionize production in one sector after another. Computing power solves more problems each year, including manufacturing problems.

Key point: The more the world relies on smart machines, the more domestic wage rates become irrelevant to export prowess. That will help the wealthier countries, most of all the United States. This logic works on both sides. The United States is using less labor in manufacturing, but China is, too, even as its manufacturing output is rising.

The fact that Chinese manufacturing employment is falling along with ours means that both our higher wages and their lower wages are becoming less relevant for the location of manufacturing decisions. The less manufacturing has to do with labor costs and relative wage levels, the greater the comparative advantage of the United States.

2) Recent discoveries of very large shale oil and natural gas deposits in the United States may mean we are the "new Saudi Arabia of energy markets." The United States has new fossil fuel discoveries to draw upon- enough to fuel this country for decades- and there is plenty of foreign demand for those resources.

From the International Energy Agency (IEA) last month: "The supply shock created by a surge in North American oil production will be as transformative to the market over the next five years as was the rise of Chinese demand over the last 15."

3) Demand from the rapidly developing countries- and not just or even mainly demand for fossil fuel- is escalating sharply. As the developing world becomes wealthier, demand for US exports will grow. Indeed, of the wealthy nations, the United States is likely to be one of the best at capturing those growing markets.

The bottom line is that the manufacturing and energy renaissance in the United States is a long-term story; not a short-term trade … but it has legs. It should ultimately benefit our economy in multiple ways, including: keeping inflation low, boosting capital/infrastructure spending, improving job growth, lowering the trade deficit, and improving national security/geopolitical landscape.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab