Key Points

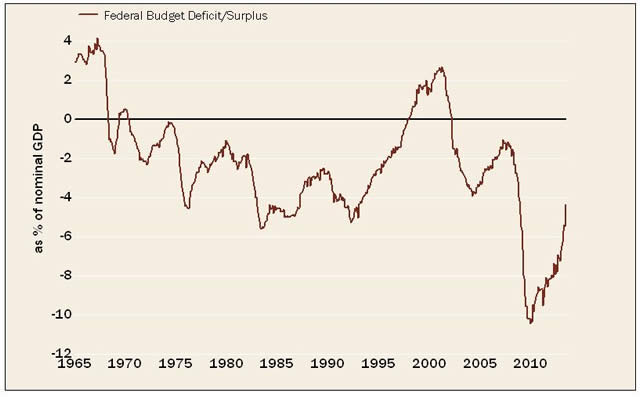

- The budget deficit has been cut by more than half…from over 10% of GDP to less than 5% today.

- June saw a budget surplus!

- The health of the private sector (given its deleveraging since 2007) more than offsets the drag from public sector deleveraging.

Here is a story still under-told. The US federal budget deficit is plunging. It's been in a steady decline for over four years; but the pace at which it's improving has really picked up in the past year, particularly last month. About two-thirds of the improvement has come from the spending side, with the remainder on the revenue (tax receipts) side.

Deficit's Been Cut in Half

Source: FactSet, US Treasury Department, as of June 30, 2013.

Source: FactSet, US Treasury Department, as of June 30, 2013.

Powerful trend

Ned Davis Research put together a great update on the trends underlying the deficit last month and I have filled in the blanks now that we have June's readings. Before I get to the details, it's notable that the government ran a $117 billion surplus in June. Many commentators have dismissed this reading because of large profits from Fannie Mae and Freddie Mac. But those accounted for only $66 billion; which means even excluding that figure, we're still looking at a surplus of $51 billion.

In June, the 12-month total of federal receipts increased 13.4%; the fastest pace since mid-2006, and nearly double the average annual 6.8% gain. The main sources of improvement included individual and corporate income tax receipts, as well as employment taxes. Corporate income tax receipts increased 23.6% on a year-over-year trend basis, and accounted for 10% of total government, near its highest share since early 2009. Individual income taxes rose 13.8%, while employment tax receipts rose 9.7%, surpassing the prior peak in mid-2006. The latter reflects the increase in payroll taxes at the start of this year, and the steady increase in nonfarm payrolls- up 5.1%, or 6.582 million jobs, since reaching a trough in early-2010.

The 12-month total of federal outlays declined 6.0% in June from a year ago; contrary to an average annual 7.9% gain. Income security outlays fell 3.6% on a year-over-year trend basis; as fewer people relied on the government for social assistance and emergency unemployment benefits began to phase out. Defense outlays declined 5.0%; the most since data started in 1995, as the United States wound down its wars. The decline also partly reflects the reduction in the defense budget as part of the sequester. Finally, net interest fell 5.9% from a year ago; the most since mid-2010.

Spending Down, Revenues Up

Source: Bureau of Economic Analyis, FactSet, US Treasury Department, as of June 30, 2013.

As a share of gross domestic product (GDP), government outlays fell to 23.3% in this year's first quarter; from a peak of 25.6% in the third quarter of 2010; but remain well above the historical average of 19.7%. Revenue increased to 18.4% of GDP in this year's first quarter; from 15.8% in the third quarter of 2009; in line with its historical average of 18.0%.

Longer-term sources of improvement (highlights from Seeking Alpha):

- New spending legislation has been dead-on-arrival due to DC gridlock.

The sequester has reduced spending in certain areas or kept it from increasing in others.

- Unemployment insurance payouts have fallen as seven million fewer people are recipients vs. the high.

- The economy has been steadily (albeit slowly) improving, generating seven million new jobs, an almost $2 trillion increase in personal income, and about a one-third organic increase (i.e., unrelated to higher tax rates) in personal income tax receipts.

- Higher taxes on upper-income taxpayers has caused many to accelerate income and capital gains realizations

- Corporate profits are up 65% from the low; while taxes paid have more than doubled from $122 billion in 2009 to $272 billion in the past 12 months.

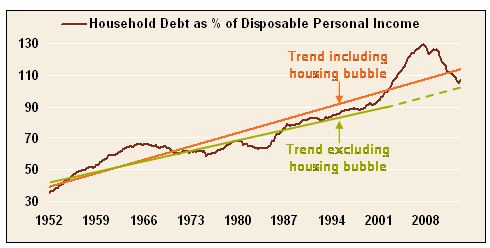

Private power

The resilience of the private sector during the public sector's retrenchment has been notable; not least due to the era of deleveraging forced upon it during the global financial crisis that erupted in 2008. Since a high of nearly 130% of disposable personal income in the third quarter of 2007, household debt has moved to its recent low of 105% as of the fourth quarter of 2012. That is now well below the long-term trendline; and is even flirting with the ex-bubble trendline.

Household Debt Way Down

Source: FactSet, Federal Reserve, as of March 31, 2013.

In sum

Much has been said about the "new normal" rate of economic growth; sometimes referred to as "stall speed" growth. But that's inclusive of government. Less noted is the "old normal" rate of growth by the private sector. Since the recession ended in June 2009, the overall average rate of growth of US real gross domestic product (GDP) is a relatively paltry 2.1%. However, excluding the government (federal, state and local) sector, the average pace of real GDP has been 3.1% over the same period. It shows that the government can and should continue to deleverage without tanking the economy, thanks to the relatively healthy private sector. This is encouraging; especially since the government sectors deleveraging is already paying deficit dividends.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab