Key Points

- After a great year for equity markets in 2013, investors are looking to next year and wondering whether there will be a "payback" coming. We believe there are important lessons to be learned from the past year and that the economy appears to be gaining momentum as we head into 2014.

- History isn't a big help with regard to the Fed winding down its asset purchase program, which is likely to be a dominant story throughout 2014. And although the recent budget agreement is a small plus, 2014 is also an election year which means political bickering will continue to be ever present.

- European equities still look attractive, but deflation concerns are likely to force the European Central Bank's hand even more and a policy mistake is possible. Likewise, Japan is entering a critical period in its nascent recovery, which makes us cautious; although we are warming to China in light of their proposed structural changes.

NOTE: Due to the upcoming holidays, the next scheduled Schwab Market Perspective is January 17, 2014.

This space is usually dedicated to our most current views of the market and the economy and what we believe investors' response should be. In this issue, however, we thought it would be a good chance to take a step back and see where we've come from in 2013 and, more importantly, where we may be headed in 2014.

Where we've been

Equities have had another stellar year in 2013, with major indices posting gains of over 20%. Most interesting may be to watch investors' reactions to the shift that's occurred in historical returns. For the five years ending in 2012, the price-only return for the S&P 500 was -3%; while at the end of 2013, it's on track to be near +100%. What a difference a year makes (especially when you can drop 2008 out of the look-back period).

A near-term pullback to relieve extended sentiment conditions would neither be a surprise nor unwelcomed. The gains came in the face of ongoing macro challenges, illustrating again that stocks often like to climb a "wall of worry." The past year started with a government "crisis" and an agreement regarding the "fiscal cliff." Throughout the following months we saw political problems in Europe, an international crisis in Syria, another US government shutdown, a botched rollout of the Affordable Care Act, and the word "taper" entering the investing lexicon. Yet stocks kept powering higher, with only brief pauses along the way. A lesson from 2013 was that waiting for the perfect opportunity to get into stocks means taking the risk of being out of the market during a strong upside run.

After the skittishness shown by the market leading up to what was believed to be the start of tapering [its bond purchases associated with quantitative easing (QE)] by the Fed in September, this time around the market seems more prepared. Tapering is very likely to begin soon and continue to be a prominent story throughout 2014, but volatility may not be as extreme as many have assumed. During the summer rout, investors were assuming short-term rates were going to get hiked sooner than originally anticipated; but today, the futures market show an anchoring of short rates until at least mid-2015. This suggests the market now believes the mantra that "tapering is not tightening."

Finally, we encourage investors to go back to the end of 2012 and look at the stock market predictions by "experts" for 2013. This is the final lesson from last year and it's one that remains the same—that predictions for specific returns over an arbitrary time period like a calendar year are usually nothing more than a shot in the dark and should be treated as such.

Where we're going

We are seeing some developments that we think will help contribute to a still-positive equity environment in 2014.

There are a couple of trends that are interesting to note based on history. According to our friends at ISI Research, there have been 11 years since 1950 that the S&P 500 has posted 25% plus gains, which is roughly what we appear to be in store for in 2013. After each of those 11 years, with the exception of two recession years in 1981 and 1990, the S&P posted positive results in the following year, with an average gain of over 16%. Adding to our historical quiver, Ned Davis Research provides excellent word on Presidential cycles which, since 1929, shows a prevalence of corrections in the second quarter of the second year of a cycle—which is 2014. The good news may be that those corrections historically have proven to be great buying opportunities, as the third and fourth quarters of the second year in an election cycle, and the first quarter of the third year, have posted the highest average gains of all.

Heading into the New Year, economic growth appears to be gaining some traction. Jobless claims continue to head lower (although seasonality issues does provide for volatility in individual readings), while the past couple of jobs reports have been strong, with October's and November's gains of over 200,000 each month. In addition, the unemployment rate dipped to 7.0%, the lowest level since November 2008.

We've also seen a pickup in the Baltic Dry Index (an index of global shipping rates), which tends to be a good indicator of global economic growth, after a pullback earlier in the year.

Global growth appears to be accelerating

Source: FactSet, Baltic Exchange. As of Dec. 6, 2013.

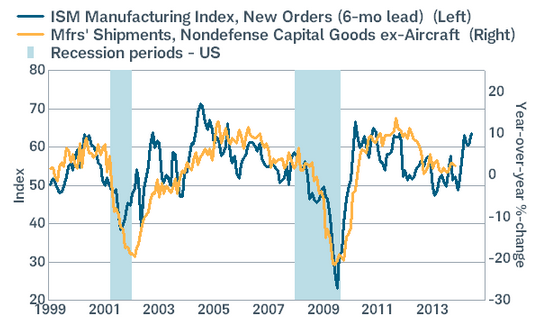

And the business community may finally be coming around, with improved sentiment and leading indicators suggesting a coming rebound in capital spending; supported by bloated cash balances. The November Institute of Supply Management (ISM) Manufacturing Index posted a reading of 57.3, the best level since April of 2011, while the new orders and employment components both posted solid gains.

ISM indicates increased capex in 2014

Source: FactSet, ISM, U.S. Census Bureau. As of Dec. 6, 2013.

We believe the first part of 2014 will see a continued upward trend in US equities, although we will likely see some pullbacks along the way, with another debt deadline looming. There is a glimmer of hope around political dysfunction with the recent budget agreement; albeit not anything resembling a "grand bargain." Additionally, Fed tapering will continue to be on the minds of investors, but low inflation puts little pressure on Fed to act aggressively and gives it increased flexibility.

Global growth to improve, despite regional divergences

Adding to the likelihood of a less aggressive US Fed, global growth is expected to strengthen in 2014, with the most recent OECD leading indicator and new orders in the global manufacturing PMI hitting multi-year highs, and pointing to an improvement in most major economies. The International Monetary Fund (IMF) is forecasting global growth of 3.6% in 2014, an improvement over the estimate of 2.9% for 2013 and 3.2% in 2012.

Divergences exist under the surface though, with Japan likely to slow, both the United States (as mentioned above) and Europe expected to accelerate, and emerging market growth forecasted to improve after a disappointing 2013. Differences in stages of the business cycle will result in divergences in monetary policy as well.

Mixed monetary policy globally

* Rebased to Jan. 5, 2007 = 100

Source: FactSet, Federal Reserve, European Central Bank, Bank of Japan. As of Dec. 11, 2013.

Despite regional differences, the improved global growth outlook in 2014 is likely to have a positively reinforcing impact economically and could improve confidence for businesses, consumers and investors.

Europe less chaotic

Europe improved dramatically this past year, thanks in large part to ECB President Draghi's "do whatever it takes" pledge, and the subsequent conditional bond purchase program that provided a safety net, restored confidence and thawed credit markets. Additionally, the fiscal drag in Europe decreased and labor reforms improved competitiveness in Spain, Portugal and Ireland.

As a result, Europe emerged from recession in 2013, defying the bears. Europe's outlook for 2014 is subdued however, as there are obstacles to growth. The modest recovery has yet to become self-reinforcing to the upside, and the longer growth is suppressed, the risk is that prices, and therefore profits, begin to fall, which can become self-reinforcing on the downside. Already, eurozone inflation of 0.7% in October was low enough that the ECB felt compelled to cut rates and prompted bears to discuss the possibility that deflation in the eurozone could turn the region into the next Japan. We note that inflation is not a leading indicator, and if the economic recovery continues as we expect, inflation could pick up in the future.

The euro's strength has confounded traders and is another risk for the eurozone. While the reasons for the strength are complicated, we believe the next move for the euro is lower relative to the US dollar. The Fed taper is likely to lift the US dollar and we believe the ECB needs to ease further to keep the economic recovery in motion. The decline in the ECB's balance sheet and reduction in bank lending means eurozone financial conditions are tightening—an obstacle to growth. However, the next step for the ECB is likely to be more complicated, and could cause volatility in both the euro and eurozone stock markets.

We remain positive on European stocks because valuations are low and profit margins are depressed (and possibly at an inflection point); but there could be volatility in the first half of 2014 related to whether and how the ECB eases further.

Japan in a wait-and-see mode

The Bank of Japan's (BoJ) QE program propelled economic growth improving to 1.8% in Japan, but the outlook by the Bloomberg consensus of economists is for moderation in 2014 to 1.5%, and is likely to be determined by the Japanese consumer. Japanese consumer spending will face the hurdles of a sales tax hike that begins in April, and inflation on the rise due to the weak yen pressuring import prices for food and energy. While Prime Minister Abe is calling for wage increases, we believe businesses are likely to wait until they have better certainty regarding demand.

Investors are likely to adopt a wait-and-see attitude toward Japanese stocks, as many believe the BoJ will need to increase its asset purchase plan. But the BoJ could wait until after the impact of the sales tax can be measured. Meanwhile, structural reform momentum appears to have waned.

China—near term risks but better outlook?

Our narrative of "slower growth is the new normal in China" played out in 2013 and we expect it to continue in 2014. This outlook is based in the view that the old economic model of debt-led investment in factories, infrastructure and property was running out of steam as the economic dividends were waning and debt had risen too far, too fast. While we were encouraged by the new leadership's attempts to clamp down on speculation, we believed it could be a risky proposition and suggested stock investors avoid Chinese-related investments until we moved to a neutral position in September.

The risk of the government's clampdown came to fruition in the form of a liquidity crunch in the banking system in June. In order to thwart a growth scare, China's government pulled out its "automatic stabilizer"– stimulus in the form of infrastructure spending, which saw a dramatic pick up in the third quarter and stabilized growth. Additionally, the government backed off of restrictions on the shadow banking sector, and stopped its verbal clampdown on the property market.

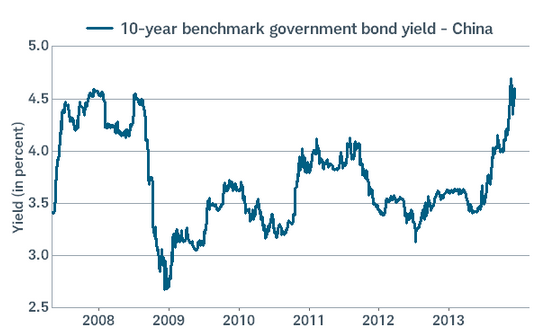

Looking forward, we believe China's economic outlook is to the downside in the near-term. China's economy could become more vulnerable the longer reforms are delayed; and a transition away from debt-led investment is likely to be accompanied by lower growth. Therefore, we expect China to continue with reforms and allow a gradual economic slowdown. Additionally, financial conditions are "stealth tightening," as yields on government, corporate and interbank debt have increased 50-100 basis points since the beginning of November. This is likely to either dissuade borrowers or create higher borrowing costs for those that do borrow, cutting into economic growth.

Stealth tightening in China

Source: FactSet, JPMorgan Chase. As of Dec. 11, 2013.

However, our intermediate-term outlook for China is improving as a result of a comprehensive reform plan put forth in the Third Plenum planning session. The top reforms we view favorably include those around the financial system, local government budgets, rural land rights, and hukou (household registration). We are warming to Chinese stocks as valuations and sentiment are low, and the reforms, if implemented, could create higher quality and more sustainable growth for China. However, we still have a neutral view on emerging markets overall due to structural issues for many countries. We will be writing more about this and other issues in articles at www.schwab.com/oninternational.

So what?

In 2013 we saw investors move somewhat reluctantly into equities, and we believe there is more cash to be put to work in 2014. Investors should heed the lesson that there is no perfect time to invest, and often the times when it feels least compelling ultimately prove to be the most profitable. We expect the US market to experience a decent pullback at some point during 2014, but still believe stocks will end the year higher. Treasury yields will also likely continue to move higher, but not substantially so; with a 3-3.50% range seeming reasonable to us for the 10-year Treasury. European equities look attractive, and we are warming to the Chinese market, but Japan faces some critical events that we will be watching closely, while emerging markets ex-China still look unattractive. As always, keep a longer-term perspective in mind, as 2014 is bound to have both ups and downs that will require discipline in your investing strategy.

Important Disclosures

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

Manufacturing Purchasing Managers Index (PMI)is an indicator of the economic health of the manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Labor Reportis a monthly report compiling a set of surveys in an attempt to monitor the labor market. The Employment Situation Report, released by the Bureau of Labor Statistics, by the U.S. Department of Labor, consists of:

• The unemployment rate - the number of unemployed workers expressed as a percentage of the labor force.

• Non-farm payroll employment - the number of employees working in U.S. business or government. This includes either full-time or part-time employees.

• Average workweek - the average number of hours per week worked in the non-farm sector.

• Average hourly earnings - the average basic hourly rate for major industries.

Initial Jobless Claims is a measure of the number of jobless claims filed by individuals seeking to receive state jobless benefits reported on a weekly basis.

Leading Economic Index is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

The Organization for Economic Cooperation and Development (OECD) Composite Leading Indicator is a monthly indicator used to evaluate near-term economic prospects and risks and is designed to capture turning points in an economy's growth cycle at an early stage.

The Baltic Dry Index is shipping and trade index created by the London-based Baltic Exchange that measures changes in the cost to transport raw materials such as metals, grains and fossil fuels by sea.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

Past performance is no guarantee of future results.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab