Key Points

- Stocks have seen wide swings recently, but year-to-date major indexes are roughly flat. Volatility may persist, but we suggest investors look past the near term and focus on the underlying fundamentals.

- The economy appears to be picking up steam and earnings season has been generally better than previously-lowered expectations. The Fed continues to sound a dovish tone, but we are starting to see signs of deflation risk receding. Geopolitical risks are elevated and the regulatory environment continues to be a concern to businesses.

- Europe is still slowly recovering and the European Central Bank (ECB) may be able to forgo quantitative easing, but Japan seems to have a disjointed economic policy and may have difficulty escaping its long-term decline. Chinese stocks appear priced for a lot of bad news, which we think makes them an attractive option for risk-tolerant, patient investors.

There are not many solid reasons behind the recent market action we've seen. Momentum stocks have come under significant selling pressure, and we are glad to see some of those extended valuations come down, but what started the selloff is difficult to pinpoint. Pricing concerns in the biotech space may be one culprit. Equally confounding has been the rotation within the equity market from cyclical to defensive names, especially into utilities stocks, along with the continued fascination with 10-year Treasuries yielding around 2.6-2.7%.

To us, this illustrates the folly of trying to time the market. Near-term moves often have no obvious catalyst, and certainly not one that can be accurately predicted. Focusing on the underlying fundamentals of the economy and earnings, and keeping a longer-term view in mind, is key to successful investing. However, the recent pullback and elevated volatility has helped to work off some of the froth in the market and correct sentiment indicators that had gotten extended, helping to set the stage for the potential next move higher.

Economic clouds are lifting

The extended rotation within the market from cyclicals to defensives has been in contrast to economic data rebounding from the largely cold-weather induced slowdown. Retail sales posted a better-than-expected 1.1% gain in March, while ex-autos and gas they rose a solid 1.0%; and previous months were revised higher. And although the Empire Manufacturing Index unexpectedly fell, it remained in territory depicting expansion, and the Philly Fed Index jumped from 9.0 to 16.6. And improving capital spending is one of the themes we believe will be a major driver of the market in the coming months.

Business spending plans improving

Source: FactSet, Nat'l Federation of Independent Business. As of Apr. 18, 2014.

Along that theme, industrial production posted another gain by rising 0.7% in March, and February's number was revised to a 1.2% rise from the initially reported 0.6%. Additionally, capacity utilization rose to 79.2 from 78.8, another indication of resources being used and the need for spending to increase. Most recently, durable goods (+2.6%) and core capex orders (+2.2%) were both well ahead of expectations. And we continue to see the labor market improve as jobless claims are comfortably in the low-300,000 range. and the unemployment rate is down to 6.7%. Also, earnings season has been better than expected relative to lowered expectations; and forward-looking commentary has been generally more upbeat than previous quarters. This suggests that cyclical sectors such as consumer discretionary, tech and industrials regain their leadership, interest rates again begin to rise, and defensive sectors such as utilities, telecom and consumer staples give back some of their recent gains. Amidst volatility and pullbacks, we do believe the market will end the year higher.

One potential problem could be if housing doesn't start to reaccelerate as we enter the critical selling season. Homebuilder sentiment continues to be subdued as indicated by the National Association of Homebuilder (NAHB) Index posting a disappointing 47 reading; although interestingly, builders cited lack of available labor as one of the headwinds they were facing. Lower affordability and inventories have been culprits as well. Housing starts rose by 2.8%, but permits fell by 2.4%, , while existing home sales fell 0.2% and new home sales fell a disappointing 14.5% to the lowest level in eight months. We believe we'll see housing accelerate as the weather continues to warm up, but we are watching rates, credit conditions, prices, and sentiment closely.

Fed focus nearing a shift?

The Federal Reserve continues to emphasize a "dovish" stance and remains concerned about both the labor market and the threat of deflation. Monetary policy continues to inch toward normalization, but Fed Chairwoman Janet Yellen has made it a point to emphasize the Fed's plan to stay accommodative for an extended period—data permitting. And that's where a shift may be occurring. We are beginning to see signs that deflation risk is ebbing and inflation may be set to pick up a bit. As noted above, capacity is increasingly being sopped up, both in the equipment and labor arenas. The recent Consumer Price Index showed higher-than-expected gains in both the headline and core readings, albeit still low by historical standards. And perhaps most importantly, we're finally starting to see signs of rising wages, particularly among non-supervisory workers.

Wages on the rise

Source: FactSet, U.S. Dept. of Labor. As of Apr. 18, 2014.

It could be that the surprise of 2014 is increasing prices from today's low levels. If this occurs, history has shown that it tends to be equities that are the best place to be as companies and consumers can both benefit from better pricing power and higher wages.

Putting a damper on things continues to be uncertainty regarding government policy. The regulatory environment is fraught with uncertainty and is continually cited by business as a hindrance to expansion, with large financial institutions seemingly especially under attack. The Dodd-Frank legislation has already imposed numerous new rules on much of the financial industry; but the real rub is that almost half of the rule-making process is still to come. We regularly hear from business leaders that when they don't know the rules of the game, they're less likely to suit up to play. According to law firm Davis Polk, as of April 1, 51.8% of the required rulemakings have been finalized, while 98 (24.6%) have yet to even be proposed, four years after the passage of the bill. But it's not all bad news. With the major initial hit of sequestration behind us, fiscal drag will likely have hit its peak in 2013 and is set to wane this year and next (and become a positive thereafter). And although public sector deleveraging has only just begun and has a long road to hoe, the budget deficit is now down to about 3% of gross domestic product (GDP) from its recent high of 10%.

Europe: will more stimulus be needed?

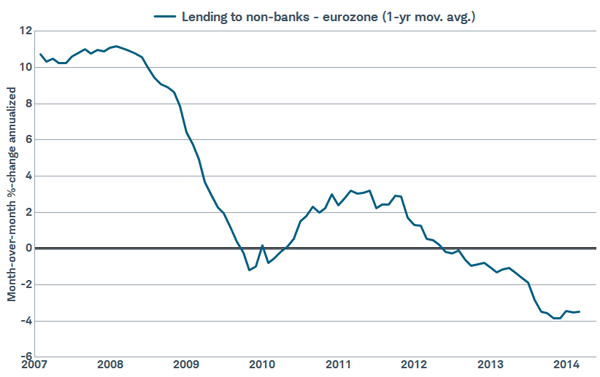

In comparison to the United States, Europe's recovery came later and has lagged in speed. It's been hampered by the eurozone sovereign debt crisis, as well as a prolonged policy response due to the lack of a true union beyond a shared currency and limitations on the European Central Bank (ECB). The aftereffects are still being felt, most notably in the banking system. Eurozone banks have been paralyzed by the threat of uncertain new regulations and higher capital requirements, resulting in banks' deleveraging at the expense of lending. Credit is the lifeblood of economic growth and the nearly two-year contraction in lending has kept a lid on growth and inflation in Europe.

The prolonged period of low inflation predicted by the ECB has resulted in calls for more monetary stimulus. At its April meeting, the ECB confirmed "unanimous commitment" to using "unconventional instruments," with investors weighing the potential for a US-style quantitative easing (QE) program. Unlike the Fed, restrictions on the ECB include the need to "sterilize" asset purchases, wherein liquidity injections are offset by asset sales; and a prohibition on "monetary financing," or financing the fiscal spending of individual countries.

Businesses in the eurozone rely heavily on banks, while those in the United States rely on the capital markets for funding; resulting in the ECB's preference for buying bank loans rather than government bonds as the transmission mechanism to lower rates and boost growth. However, the ECB would be unlikely to buy bank loans until completing its "Comprehensive Assessment" of bank balance sheets, which is not expected until this fall.

Despite the concerns about lending and low inflation, economic growth continues to strengthen, with the preliminary eurozone composite PMI hitting a three-year peak of 54.0 in April; signaling a 0.5% pace of GDP growth in the second quarter and building on the 0.4% rise in the first quarter according to Markit. Additionally, lending may be stabilizing and about to become less of a drag on economic growth. It is possible that deflation risks subside before any broader QE program could even be implemented, eliminating the need for QE.

Eurozone lending slide bottoming?

Source: FactSet, European Central Bank. As of Apr. 22, 2014.

Despite the risks to economic growth and potential for market volatility, we remain positive on European stocks, due to the prospects for economic and profit margin improvement.

Japan: would more QE help?

In contrast to the hopes of "three arrows" to revive Japan's economy, thus far one arrow, monetary policy, has been the primary strategy. The first arrow of fiscal stimulus has reversed to fiscal restraint; with a sales tax hike beginning in April and the International Monetary Fund (IMF) forecasting a fiscal tightening of 2.5% of GDP this year, and further tightening of 1.0% in 2015. Meanwhile, the arrow of structural reforms has been timid.

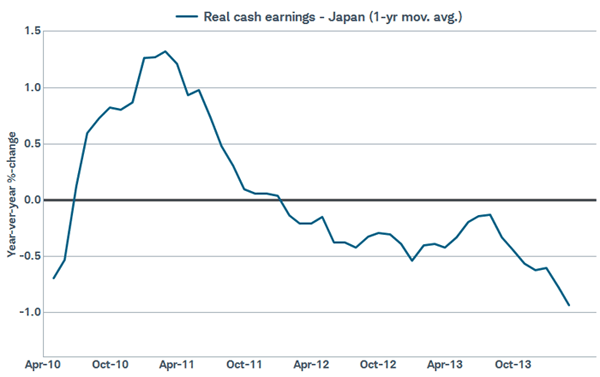

This leaves monetary stimulus as the lone arrow; and even the massive monetary stimulus by the Bank of Japan (BoJ) has had few apparent benefits for the Japanese economy. While economic growth in Japan surged in the first half of 2013 to above 4.0%, the second half of 2013 slowed to a rate below 1.0%. The economy is likely to struggle going forward due to the headwinds facing consumers, which represent roughly 60% of the economy. These headwinds include the sales tax hike, a lower yen reducing consumer purchasing power, and wages after inflation continuing to fall.

Japanese wages after inflation continue to fall

Source: FactSet, Japanese Ministry of Health, Labour and Welfare. As of Apr. 22, 2014.

The consensus expectation is for a magnification in the size of the BoJ's QE program in July, which could weaken the yen and boost the Japanese stock market in the short term. But we are becoming increasingly downbeat on the longer-term outlook for the Japanese economy and stock market.

China has options if the pain becomes too great

Imbalances in China's economy have built up in recent years, necessitating structural change and slower growth to repair. But policymakers have a fine line to walk---implementing reforms and reducing credit growth, while keeping economic growth from falling too much.

We don't believe a hard landing in China is imminent, but are somewhat concerned about the slowdown in the property market. The property market has been hit by both a sharp increase in construction completions in recent months, along with credit restrictions on both developers and homebuyers. As a result of a decline of 7.7% in new home sales in the first quarter, and the inventory overhang, property developers have offered discounted prices to meet cash flow needs and reduce their risk. This in turn has slowed average price increases and new construction.

The risk is that the debt troubles of small developers could reverberate if the confidence of investors in these debts is damaged to the point of less inclination or ability to loan to larger developers. The property market accounted for 16% of GDP in 2013 according to Nomura Global Economics; but the total of construction, sale and outfitting of apartments accounted for 23% of China's GDP in 2013, according to Moody's Analytics. As a result, a lengthy or deep slump in the property ecosystem could catalyze a decline in the overall economy.

However, China's policy options are not comparable to the response to the housing bubble burst in the United States. As a command economy, the Chinese government has the leeway to pursue policies unthinkable in the United States. While the United States "over-spends," China "over-saves." Domestic savings are about 50% of China's GDP, translating into new savings of $4.5 trillion every year. Additionally, China has a closed capital account that restricts money moving in and out of the country, the government controls the majority of bank assets, and has $4.0 trillion in foreign exchange reserves to fight a liquidity crisis.

We believe Chinese policymakers have plenty of ammunition to fight a plunge in economic activity and have already begun to loosen monetary and fiscal policy. Meanwhile, Chinese stocks appear to be pricing in a lot of bad news. As a result, we believe Chinese stocks could recover and outperform the emerging market universe. Read more in Why New Reforms Make Chinese Stocks Attractive and at www.schwab.com/oninternational.

So what?

At times, markets are difficult to read in the short term-even after the fact. But the fundamentals of the economy and corporate health tend to win out in the longer term, and we believe that there are positive developments on those fronts in the United States. Internationally, Europe may be able to escape without the ECB actually acting, while the Japanese situation is growing more concerning as they may not be able to reverse their long decline.

Important Disclosures

The Empire State Index is a regional, seasonally-adjusted index published by the Federal Reserve Bank of New York distributed to roughly 175 manufacturing executives and asks questions intended to gauge both the current sentiment of the executives and their six-month outlook on the sector.

The Philadelphia Federal Index is an index that is published by the Philadelphia Federal Reserve Bank and is constructed from a survey of participants who voluntarily answer questions regarding the direction of change in their overall business activities. The survey is a measure of regional manufacturing growth.

Industrial Production is an indicator measures the amount of output from the manufacturing, mining, electric and gas industries.

Capacity Utilization is a metric used to measure the rate at which potential output levels are being met or used. Displayed as a percentage, capacity utilization gives insight into the overall slack in the economy.

Durable Goods Orders is an economic indicator released monthly by the Bureau of Census that reflects new orders placed with domestic manufacturers for delivery of factory hard goods (durable goods) in the near term or future.

The Labor Report is a monthly report compiling a set of surveys in an attempt to monitor the labor market. The Employment Situation Report, released by the Bureau of Labor Statistics, by the U.S. Department of Labor, consists of:

• The unemployment rate - the number of unemployed workers expressed as a percentage of the labor force.

• Non-farm payroll employment - the number of employees working in U.S. business or government. This includes either full-time or part-time employees.

• Average workweek - the average number of hours per week worked in the non-farm sector.

• Average hourly earnings - the average basic hourly rate for major industries.

The Unemployment Rate is the number of unemployed workers expressed as a percentage of the labor force.

Initial Jobless Claims is a measure of the number of jobless claims filed by individuals seeking to receive state jobless benefits reported on a weekly basis.

The National Association of Homebuilders (NAHB) – Wells Fargo Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to measure homebuilder sentiment in the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. It is a weighted average of separate diffusion indices for these three key single-family series.

Existing home sales is a monthly economic indicator released by the National Association of Realtors of both the number and prices of existing single-family homes, condos and co-op sales over a one-month period.

New Home Sales is a monthly economic indicator released by the U.S. Department of Commerce's Census Bureau that measures sales of newly built homes, which includes both quantity and price statistics.

Housing Starts and Building Permits report is data compiled by the U.S. Census Bureau that reports the number of new residential construction projects that have begun during any particular month, while permits is the finalized number of the total monthly building permits on the 18th work day of every month.

Markit Manufacturing Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

Manufacturing Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

Gross Domestic Product (GDP) is a quarterly report released by the U.S. Bureau of Economic Analysis that is an aggregate measure of total economic production for a country, representing the market value of all goods and services produced by the economy during the period measured, including personal consumption, government purchases, private inventories, paid-in construction costs and the foreign trade balance (exports are added, imports are subtracted).

Past performance is no guarantee of future results.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0414-2914)

(c) Charles Schwab