Key Points

- A lot of movement to go nowhere can characterize the major indexes to this point in the year. History suggests we're entering a potentially tough period for stocks, due to both seasonal and midterm election year tendencies.

- The spring economic rebound appears to be in full force, with housing being a notable exception, but markets haven't reacted enthusiastically. The Fed continued tapering its securities buying, which was greeted with a yawn, with focus now on when short rates will begin to rise. Meanwhile, the call for corporate tax reform may grow louder in light of recent moves by corporations to lower their tax rates via foreign acquisitions.

- Earnings season in Europe was disappointing but we believe things are improving and stocks are attractively valued. Meanwhile, the Chinese property market is concerning, but we believe an economic hard landing will be avoided, providing investment opportunities for risk-tolerant investors.

Sell in May. A common refrain heard this time of year. Historical evidence compiled by our friends at Ned Davis Research shows stock market returns in the time period between May and September since 1950 have been far less than those for the time between October and April. Combine that with the history of midterm election years (2014 is one), which shows that there has typically been a sizable mid-year downturn in stocks and the outlook for the next several months may have investors on guard.

But where to go? Cash is returning next to nothing, yields on fixed income remain extremely low, with the potential for price erosion if yields should move higher, and most international markets have greater concerns than the United States—as detailed below. Additionally, since 1950, 64% of the time periods between May and September have produced positive equity returns, including last year's 5.3% for the S&P 500. Add these facts in, combined with the issues of timing, transaction costs, and tax consequences makes trying to trade around these short-term forces more treacherous.

We still believe a decent-sized pullback could occur in the next couple of months, but the fact that some of the more extremely overvalued and highflying stocks have already corrected without substantial overall market damage may lessen those odds. Regardless, we continue to believe that stocks will end the year higher thanks to accelerating economic growth.

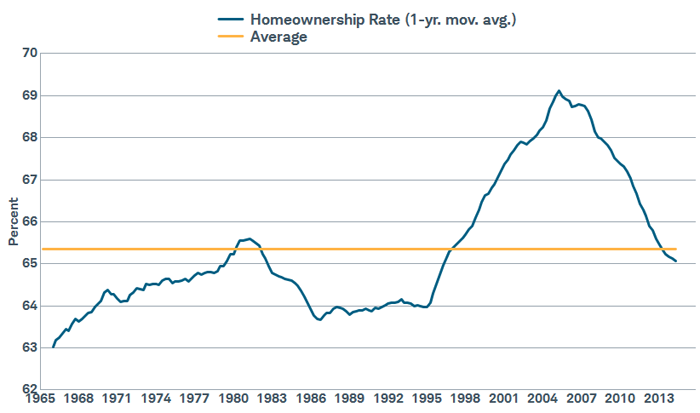

Spring thing

Recent economic developments and the outlook for the rest of the year look encouraging. As expected, most data readings have rebounded nicely from the winter slump. The weak 0.1% growth reading in first quarter gross domestic product (GDP) was largely ignored as the start of the second quarter looks to be improving greatly. The Chicago PMI jumped to 63 from 55.9, while the Institute for Supply Management's (ISM) Manufacturing Index rose to 54.9 from 53.7, with the employment component posting a nice 3.6 point gain to 54.7. Additionally, the ISM Non-Manufacturing Index rose to 55.2 from 53.1, while the new orders component jumped to 58.2 from 53.4. Corporations appear to be regaining some of their "animal spirits" as capital expenditure plans have expanded and merger and acquisition activity has accelerated. Our friends at ISI Research report that, as of the end of April, the previous 84 days saw 142 deals totaling over $1.2 trillion dollars—a lot of cash to use and more to get at low cost if needed.

And the consumer seems to be rebounding as well, shaking off the winter doldrums and working off some of the pent-up demand that was built. Personal spending rose 0.9% in March, the largest gain since August of 2009, which builds on a nice rebound in retail sales we saw last month. Also, employment continues to improve as ADP reported 220,000 private sector jobs were added in April and the more widely-followed Bureau of Labor Statistics jobs report showed a much better-than-expected 288,000 additional jobs. In addition, the prior two months were revised higher by 36,000 and the unemployment rate fell to 6.3%. There continue to be concerns regarding the historically low labor force participation rate and the long-term unemployed, but these may be more structural and demographic issues that may not turn around to any great extent.

The weak link in the bounce at this point continues to be housing, as mortgage applications are relatively weak, housing starts continue to falter, and the homeownership rate continues to fall. However, our belief is that there is a tendency to overshoot on the downside when coming off of an inflated upside, potentially boding well for the future as the condition normalizes.

Leveling off?

Source: FactSet, U.S. Census Bureau. As of May 6, 2014.

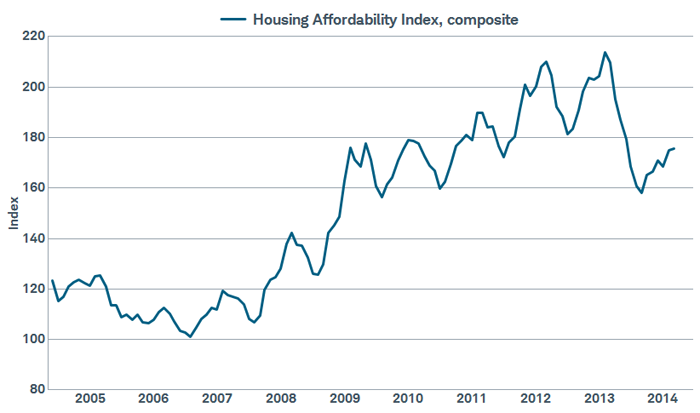

We still believe the warmer months will see a modest rise in housing activity, and we're pleased to see the rapid rate of growth seen in 2013 slow to a likely more sustainable pace. The reasons for the housing slowdown appear to be declining affordability (courtesy of higher prices) and low inventories. The housing recovery is likely to remain in pause mode in the near-term, but we believe the recovery will resume.

Affordability has fallen, but still looks attractive

Source: FactSet, Natl. Assoc. of Realtors. As of May 6, 2014.

Fed cruises along, but pressure may be building in Congress.

The most recent Fed meeting was mostly a non-event, with few changes to the Committee's statement. First quarter weakness was largely dismissed as weather related, and the continuation of tapering was announced; with the Fed now purchasing $45 billion of Treasuries and mortgage-backed securities a month. Attention has now squarely turned to the timing of the first rate increase, with the Fed suggesting that won't occur until well into 2015. But if economic data picks up, the Fed could move to raise rates sooner.

While an election year is unlikely to be one in which much gets done, there may be some urgency around one issue we've been noting for a while: corporate tax reform. With increasing tax "inversions", where companies establish a legal presence in another country to take advantage of lower tax rates, heat may begin to rise on politicians in order to keep that tax revenue in the United States. Recent rhetoric from both sides suggests a deal could be reached, but we won't hold our breath.

Will Europe be the source of another market selloff?

In contrast to growth scares and stock market selloffs in several prior summers, we believe the most likely scenario is that euro zone economic growth will add to global growth this year. This is because the contraction in lending appears to be stabilizing and leading economic indicators continue to point to a further economic recovery.

Indications euro zone recovery continues

Source: FactSet, OECD. As of May 6, 2014.

The euro zone recovery has been subdued however, keeping inflation low. While the initial reading on inflation improved to 0.7% in April from 0.5% in March, the threat of a prolonged period of low inflation has caused concerns about the threat of deflation. Deflation, or a broad-based decline in prices, is undesirable because once expectations of lower prices in the future set in, consumers and businesses may postpone spending to the future, creating a negatively reinforcing cycle that is difficult for central banks to fight.

"Lowflation" has prompted calls for a pre-emptive response to deflation, and the European Central Bank (ECB) appears to be open to unconventional policy, such as a large scale quantitative easing (QE) program. Due to technical restrictions and corporate reliance on banks for funding, the ECB prefers to buy bank loans as the transmission mechanism to lower rates and boost growth. However, the ECB may be unlikely to buy bank loans until completing its "Comprehensive Assessment" of bank balance sheets, which is not expected until this fall. By that time, a continued economic and lending recovery could avert the need for a large scale QE program, as described in our article.

We believe that easier access to credit and an economic recovery will eventually feed through to better earning; but for now, earnings of euro zone companies continue to disappoint. Of the 280 companies in the STOXX 600 Index reporting through May 7, 54% missed profit estimates in the first quarter, a sharp contrast to the 75% of S&P 500 Index companies beating earnings. Domestically-oriented companies have fared better, while exporters were hurt by currency issues such as declines in emerging market currencies and a strong euro.

On a cyclically adjusted price earnings (CAPE) basis, which adjusts for changes in the business cycle, euro zone stocks trade at a 40% discount to US equities. This is close to the largest difference in at least 30 years according to BCA Research, and suggests euro zone stocks could have room to rise if the economic recovery continues.

However, the Russia/Ukraine conflict is a risk to the euro zone and global recovery. Market volatility may to continue if there is the potential for disruptions to energy imports into Europe. The situation is difficult to predict, but if Russia's provocations don't go beyond eastern Ukraine, stock market declines could be buying opportunities. If Russia's intentions are beyond the "Russian sphere," then investors may take risk off until the situation plays out.

Will threats of a hard landing in China disrupt markets?

Imbalances in China's economy have been built, necessitating structural change and slower growth to repair, but policymakers have a fine line to walk – implementing reforms and reducing credit growth, while keeping economic growth from falling too much.

We don't believe a hard landing in growth is imminent, but are concerned about the slowdown in the property market. The property market has been hit by both a sharp increase in construction completions in recent months, along with credit restrictions on both developers and homebuyers. Property sales by volume fell 9% in April from the month prior and 19% versus a year earlier in the 44 cities tracked by China Real Estate Index System. The increased supply and lack of demand has created an inventory overhang; and property developers are cutting prices to unload inventory to meet cash flow needs and reduce risk. This in turn has slowed the average price increase and new construction.

Chinese home price increases slow

Source: FactSet, National Bureau of Statistics of China. As of May 6, 2014.

A lengthy or deep slump in the property ecosystem could catalyze a decline in the overall Chinese economy. This is because the property market accounted for 16% of GDP in 2013 according to Nomura Global Economics; and when including the sale and outfitting of apartments, was 23% of China's GDP in 2013, according to Moody's Analytics. Local governments' coffers are reliant on land sales, which fell 5% in March from a year earlier. Our concern is that the slowdown appears to be broadening out to a greater number of cities, and ensnaring mid-size Tier 2 cities.

However, China's policy options are not comparable to the response to the housing bubble burst in the United States. As a command economy, the Chinese government has the leeway to pursue policies unthinkable in the United States. While the United States. "over-spends," China "over-saves" - domestic savings are about 50% of GDP, translating into new savings of $4.5 trillion every year. Additionally, China has a closed capital account that restricts money moving in and out of the country, the government controls the majority of bank assets, and has $4.0 trillion in foreign exchange reserves to fight a liquidity crisis.

We believe Chinese policymakers have plenty of ammunition to fight a plunge in economic activity and have already begun to loosen monetary and fiscal policy, while property restrictions have begun to ease in several cities. The railway investment spending target for 2014 has been raised twice in recent months, to 800 billion yuan ($128 billion).

However, the economic support measures have not yet addressed the tight credit market. The longer policymakers keep the screws on credit, the higher the risk of a policy mistake; where growth slows too far, too fast, and causes a global market selloff on fears of a hard landing. Chinese stocks are pricing in a lot of bad news, and as long as a hard landing is averted, we believe the risk/reward is favorable for owning Chinese stocks within a market weight to emerging market stocks overall. Read more in Why New Reforms Make Chinese Stocks Attractive.

So what?

Trying to time the market and take advantage of historical tendencies has risks on both sides of the equation, but there are real costs associated with buying and selling that should be considered. Nervous investors may want to hold off allocating new money for a couple months, understanding that they may be buying at a higher price at a later date, but we suggest keeping with a long-term strategy. European stocks appear to have decent upside potential but China's property market is concerning although for risk tolerant investors, Chinese stocks look relatively attractive.

Important Disclosures

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management (ISM) Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

Mortgage Bankers Association (MBA) Mortgage Applications Survey is a comprehensive analysis of mortgage application activity compiled by the Mortgage Bankers Association of America.

The Labor Report is a monthly report compiling a set of surveys in an attempt to monitor the labor market. The Employment Situation Report, released by the Bureau of Labor Statistics, by the U.S. Department of Labor, consists of:

• The unemployment rate—the number of unemployed workers expressed as a percentage of the labor force.

• Non-farm payroll employment—the number of employees working in U.S. business or government. This includes either full-time or part-time employees.

• Average workweek—the average number of hours per week worked in the non-farm sector.

• Average hourly earnings—the average basic hourly rate for major industries.

The Unemployment Rate is the number of unemployed workers expressed as a percentage of the labor force.

Initial Jobless Claims is a measure of the number of jobless claims filed by individuals seeking to receive state jobless benefits reported on a weekly basis.

The ADP Employment Change report, sponsored by the ADP Employer Services, is a montly report that measures levels of non-farm private employment.

The S&P 500 Composite Index® is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The STOXX Europe 600 Index is an index that includes 600 components that represent large, mid and small capitalization companies across 8 countries of the European region, including Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

The National Association of Realtors (NAR) Housing Affordability Index measures whether or not a typical family could qualify for a mortgage loan on a typical home. A value of 100 means a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.

Existing home sales is a monthly economic indicator released by the National Association of Realtors of both the number and prices of existing single-family homes, condos and co-op sales over a one-month period.

New Home Sales is a monthly economic indicator released by the U.S. Department of Commerce's Census Bureau that measures sales of newly built homes, which includes both quantity and price statistics.

Housing Starts and Building Permits report is data compiled by the U.S. Census Bureau that reports the number of new residential construction projects that have begun during any particular month, while permits is the finalized number of the total monthly building permits on the 18th work day of every month.

Leading Economic Index (Indicators) is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

The Organization for Economic Cooperation and Development (OECD) Composite Leading Indicator is a monthly indicator used to evaluate near-term economic prospects and risks and is designed to capture turning points in an economy's growth cycle at an early stage.

Gross Domestic Product (GDP) is a quarterly report released by the U.S. Bureau of Economic Analysis that is an aggregate measure of total economic production for a country, representing the market value of all goods and services produced by the economy during the period measured, including personal consumption, government purchases, private inventories, paid-in construction costs and the foreign trade balance (exports are added, imports are subtracted).

The Home Ownership Rate is compiled by the U.S. Census Bureau that measures the percentage of homes that are owned by the occupant.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

Past performance is no guarantee of future results.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0514-3239)

(c) Charles Schwab