This report is lengthy, but mostly due to the charts, so it's fairly quick read.

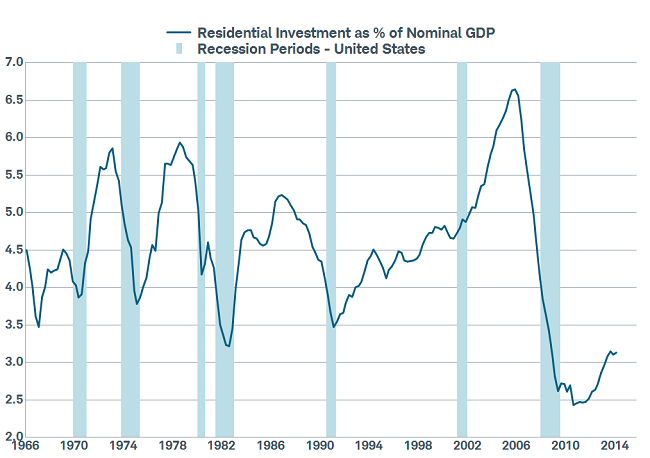

After a sharp recovery off the post-bubble low in housing, many of the key indicators have stalled. Housing has been historically considered a key driver of the US economy. But starting in the early 1990s, the relationship began to weaken. Housing was less important a driver during the tech boom of the 1990s; but then steadily grew, culminating in the bubble peak in the mid-2000s. At the peak, residential investment was at the highest share of US gross domestic product (GDP) in the post-World War II period; a clear "overshoot" relative to the 1990s.

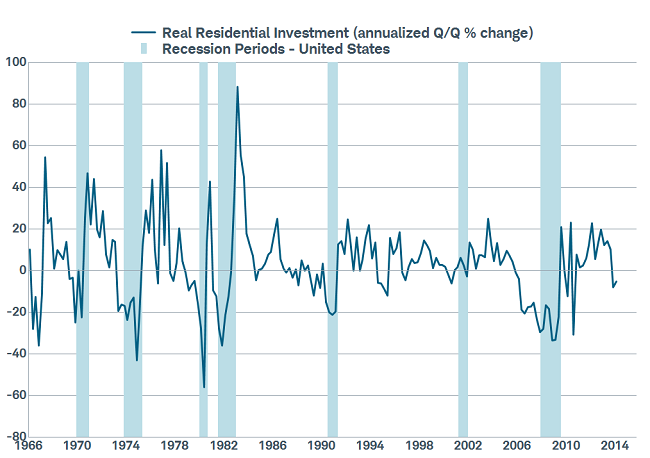

We recently saw an end to 12 consecutive quarters with residential investment as a positive driver of GDP; occurring between the fourth quarter of 2010 and the third quarter of 2013. However, the past two quarters have been negative (see Chart 2). The economic impact overall has been muted however, thanks to housing's share of GDP having shrunk by more than half since the bubble peak (see Chart 1).

Chart 1: Housing Much Smaller as Share of Economy

Source: Bureau of Economic Analysis, FactSet, as of March 31, 2014.

Chart 2: Housing's Growth Sinks Back Into Negative Territory

Source: Bureau of Economic Analysis, FactSet, as of March 31, 2014.

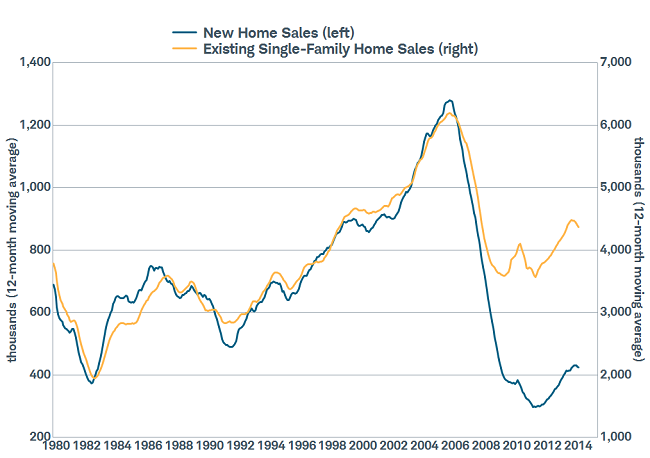

There are several headwinds bearing down on housing recently, causing home sales to stall (Chart 3). They include: Â

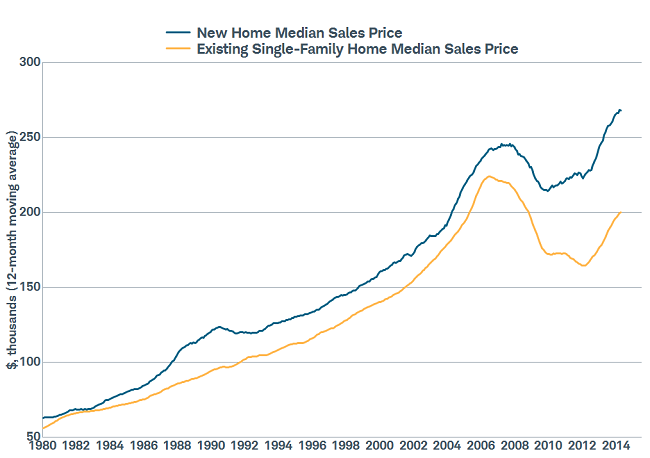

- The sharp increase in home prices, especially for new homes (Chart 4)

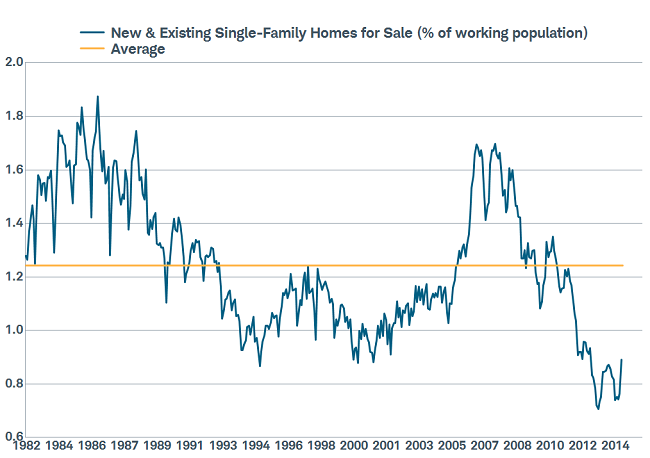

- Low inventories of homes for sale (Chart 5)

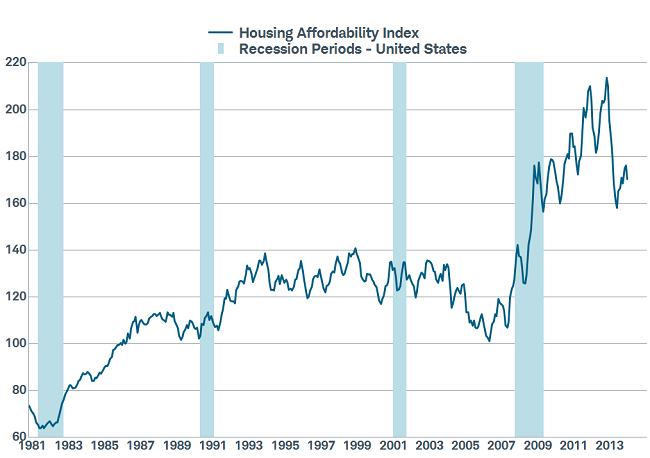

- Lower housing affordability (Chart 6)

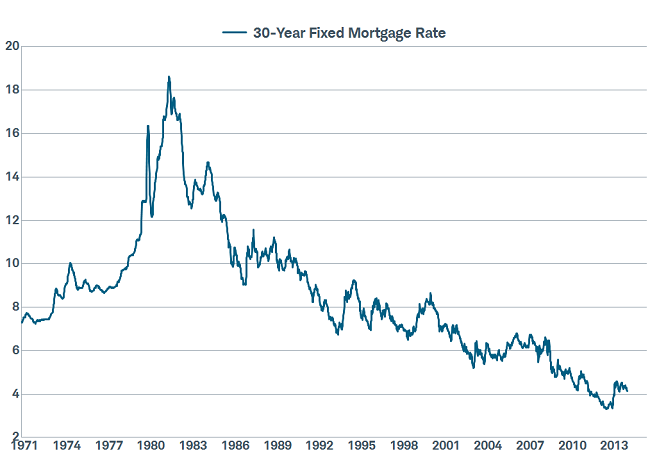

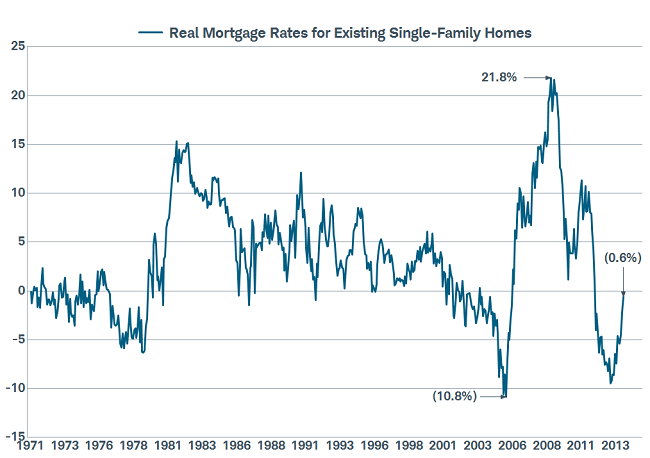

- The rise in mortgage rates that began last summer (Chart 7); including the rise in real mortgage rates (Chart 8)

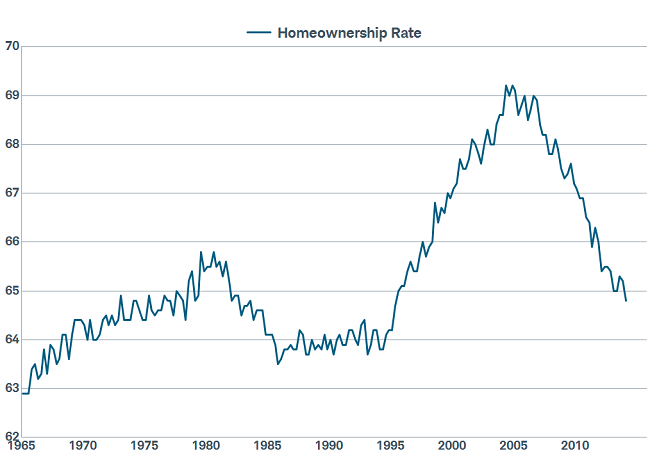

- A declining homeownership rate (Chart 9), partly due to extremely low household formations

- More recently, the horrendous winter weather

Chart 3: Home Sales Rolling Over

Source: FactSet, National Association of Realtors, US Census Bureau, as of April 30, 2014.

Chart 4: Home Prices Up, Especially New

Source: FactSet, National Association of Realtors, US Census Bureau, as of April 30, 2014.

Inventory cycle

In addition to inventories of homes for sale being quite low, the median home age has grown sharply over the past 30 years. The median age is currently 37 years, which is up from 21 years in 1985. And, 61% of single-family residences are now at least 31 years old.

Chart 5: Housing Inventory Extremely Low

Source: FactSet, National Association of Realtors, Organization for Economic Cooperation and Development (OECD), US Census Bureau, as of April 30, 2014.

Chart 6: Affordability Down But Still High

Source: FactSet, National Association of Realtors, as of March 31, 2014.

Chart 7: Mortgage Rates Ticking Back Down

Source: FactSet, Federal Reserve, as of May 23, 2014.

The relevance of "real" mortgage rates

A concept about which I've written and spoken extensively is the real mortgage rate (RMR). Its calculation is similar to how real GDP is calculated; which is simply the difference between nominal GDP and inflation. The same thinking can be applied to mortgage rates. It's not just the mortgage rate that matters when considering the purchase of a house; it's also the rate at which home prices are appreciating or depreciating (the deflator in this case). Using home price data from the National Association of Realtors (NAR), you can see the RMR below; which comes from subtracting NAR prices from nominal 30-year fixed mortgage rates.

RMRs peaked at nearly 22% during the bubble. That was when we were subtracting a deep negative number from the fixed mortgage rate; resulting in an extremely elevated RMR. Put more simply:Â at the weakest period in home prices, you could borrow at a 5% rate, but you were borrowing to buy a home depreciating at a 17% annual rate. As such, your "real" mortgage rate was 22%. There was little incentive then to borrow at any rate, regardless of how low, to buy a rapidly-depreciating asset. That is no longer the case, as you can see below. However, the recent move higher in RMRs has also been a problem.

Chart 8: "Real" Mortgage Rates Still Low

Source: FactSet, Federal Reserve, National Association of Realtors, as of April 30, 2014.

A key reason why the homeownership rate has plunged since the bubble peak is that household formations have declined substantially as well. The dominant plagues have been high student loan debt burdens, weak job growth, and tighter lending standards.

Chart 9: Homeownership Rate Back to Pre-Bubble

Source: FactSet, US Census Bureau, as of March 31, 2014.

Demographics

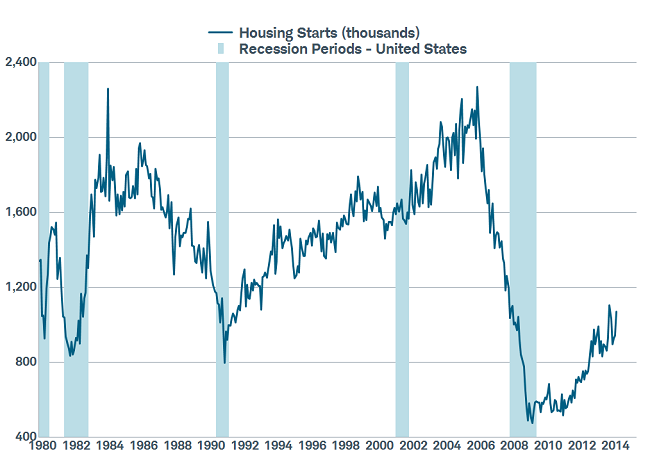

Low homeownership and formations have led to weak housing starts (Chart 10). The weakness corresponds to the period since which Millennials began entering the housing market. Demographics should eventually push starts back up toward normal levels. As noted in a recent Bespoke report, with an expected US population of over 333 million expected in 2020, catching up to historical norms in terms of housing starts per capita would see the nominal number north of 1.8 million per year; compared with the paltry sub-one million recently.

Chart 10: Housing Starts Up But Still Low

Source: FactSet, US Census Bureau, as of April 30, 2014.

One final note

Another housing-related question I get regularly is about investors having become more dominant buyers of homes. Indeed, investors now account for nearly as large a share of home purchases as owner-occupiers. But this is not necessarily a bad trend. The trend certainly helped when investors were adding demand when there was very little from traditional buyers. It's also been shown that investment buyers contribute about the same to the economy in the aftermath of a purchase than owner-occupiers.

Finally, although some of the aforementioned headwinds facing housing are fading (weather, mortgage rates and inventories); other are stickier (home prices). Housing may become less of a drag on the economy as these headwinds fade; but a more meaningful pick-up is not in the immediate horizon.