Key Points

- The stock market continues to exhibit great resiliency, with bouts of selling this year stopping short of a correction, and reversing quickly. While still optimistic, we are becoming more concerned about a possible melt-up in equities given the severity with which they tend to end.

- Housing has rebounded some, while the labor market continues to improve. Disagreements appear to be growing within the Fed; while politicians come back to town, with nothing but hollow arguing likely to come.

- Europe's economy continues to struggle and we are skeptical about the European Central Bank's ability to aggressively fight deflationary pressures. Meanwhile, Japan's economy is showing some near-term signs of improvement; while China has stabilized, providing opportunities (although substantial longer-term challenges still remain).

Stocks suffer a quick 4-5% decline only to recover fairly rapidly and move to new highs. Longer-term interest rates labor higher only to plunge again. The Federal Reserve remains extremely accommodative, despite improving economic conditions. The European Central Bank (ECB) "stands ready" to act but does little to address the growing economic concerns in the eurozone.

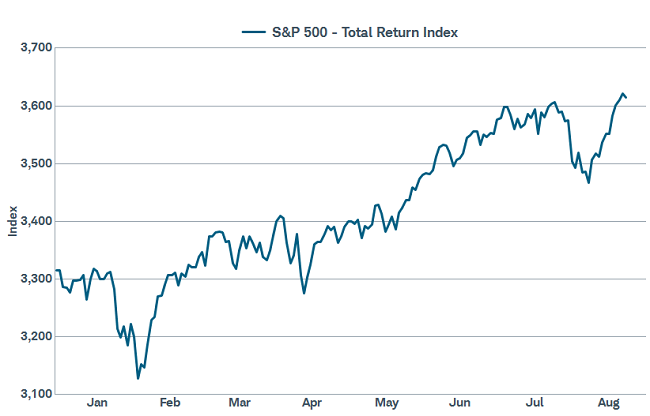

Groundhog Day?

Repeating Pattern

Source: FactSet, Standard & Poor's Corporation. As of Aug. 25, 2014.

Of course, patterns may repeat until they don't, and then what? That depends largely on what breaks first. Does the Federal Reserve tighten sooner than expected? Does the ECB move more aggressively than currently believed? Or perhaps the geopolitical situation takes a strange turn? All would likely have different impacts on the market.

The most recent stock selling appeared eerily reminiscent of earlier pullbacks this year where some concern, in this case geopolitics combined with Fed tightening worries, caused a selloff, helping to wash out overly optimistic sentiment and moving commentators to question whether it was the long-awaited correction. But then, the selling stopped, buyers stepped in, and the market recovered to new highs again. The resilience of the market has been impressive, but has renewed worries about a melt-up scenario as investors "capitulate in" to the market. The problem with melt-ups, however good they feel while underway, is that they typically end quite painful and abruptly.

We remain optimistic about stocks for the foreseeable future, although we would prefer the kind of grind-higher market we've experienced recently over a melt-up. We would also welcome pullbacks and even a correction as it would keep sentiment contained; and could elongate the bull market.

Economy supports further gains

The main reasons for our continued optimism are the improving economy, higher earnings growth and still-reasonable valuations. Stocks typically haven't suffered bear markets unless a recession was imminent, and we see no indications of that—in fact, quite the opposite.

The Index of Leading Economic Indicators (LEI) posted a solid 0.9% gain in July, while industrial production moved up 0.4% and capacity utilization crept closer to the 80 level often associated with "full capacity" by posting a reading of 79.2. Additionally, the labor market continues to improve with initial jobless claims remaining around 300,000 on a 4-week moving average basis and continuing claims moving to their lowest levels since June 2007. In addition, the Job Openings and Labor Turnover Survey (JOLTS) continues to show the "quit rate" (people voluntarily leaving their jobs) is increasing, indicating growing confidence in the labor market's improvement.

Also, the housing market is finally showing signs of renewed life as the National Association of Homebuilders (NAHB) Housing Market Index rose to 55, the highest level in seven months; housing starts rose 15.7% in July; building permits jumped 8.1%; pending home sales rose 3.3%; and existing home sales increased 2.4%. With the backup in mortgage rates we've seen, combined with changes to credit scoring that should make it easier for borrowers to qualify for loans, further improvement appears likely.

Housing on a renewed upswing?

Source: FactSet, U.S. Census Bureau, Freddie Mac. As of Aug. 25, 2014.

Disagreements in DC

Disagreements abound within the Federal Reserve regarding the pace of stimulus removal and the timing of the first interest rate hike. Minutes released following the Fed's most recent meeting showed that there was increased discussion about the current pace of normalization; with a vocal minority believing the economy and job growth have healed enough to warrant a quicker pace of accommodation removal and interest rate hikes. The market shrugged off such concerns as Fed Chairwoman Janet Yellen remains staunchly in the camp that believes with inflation pressures still benign, policy should be very slowly normalized to minimize the potential for negative economic consequences. But the hawks are concerned about being too slow to normalize rates; with asset value distortions potentially growing and complacency toward risk expanding, setting up the potential for a messy reminder. The Federal Reserve has a difficult needle to thread, and it's rare that it's handled monetary policy without disruptions and volatility.

Conversely, many investors continue to express dismay at the situation in the halls of Congress as politicians get back to work and head into the home stretch for the midterm elections. Rhetoric surrounding taxes, regulation, health care, immigration, and numerous other things will heat up, but little is likely to be accomplished. How the debates evolve and how the electorate reacts could insert some uncertainty and volatility into the system, especially given that midterm election years have brought typically-midyear pullbacks.

Europe: not enough inflation

Much bigger problems exist across the Atlantic as Europe's economy has failed to gain traction due to the eurozone debt crisis, a hobbled banking system, and a lack of flexibility. Regulations that stifle innovation and competitiveness have kept the region from reinventing itself and growing on par with the United States. While these negative factors are gradually being addressed, it has been a slow slog, and reforms have been notably absent in France and Italy.

Amid these headwinds, it's not surprising that the eurozone recovery has lagged the United States by several years. New pressure has come from the unrest in Ukraine and resultant sanctions between the European Union and Russia, which could tip the eurozone back into recession, as describe in our new article. We're concerned about softness in the locomotive of the eurozone, Germany, which comprises 30% of the region's economy.

Eurozone inflation slipping, QE to come?

Source: FactSet, Eurostat. As of Aug. 26, 2014.

The weak eurozone economic growth amid high unemployment has kept inflation well below the European Central Bank's (ECB) "below, but close to 2%" target, as seen in the chart above. Despite smaller price increases in recent months, expectations about future inflation have been little changed. Expectations are important, because once consumers and businesses believe prices will be lower in the future, they usually start to postpone spending, creating a negatively-reinforcing economic slowdown.

However, a slip in inflation expectations by the bond market in August resulted in a shift in language by ECB President Mario Draghi, encouraging the belief by investors that ECB action is forthcoming. While a small rate cut is possible, we believe hopes of a near-term ECB version of quantitative easing (QE) to buy assets are unfounded and that the ECB will want several months to measure the effects of the quarterly Targeted Long-Term Refinancing Operations (TLTRO), which starts September 18, before starting QE.

September 18 is also the date Scotland considers splitting from the United Kingdom. In our view, while a vote for full independence is a low probability, it could be accompanied by market volatility, as it may embolden other separatist campaigns across Europe, particularly in Catalonia, Spain.

Paradoxically, the worse the economic and deflation outlook becomes, the better the chance of QE and a bounce in European stocks. However, we currently have a neutral view on Europe and believe it is prudent to hold off on aggressively buying European stocks.

Japanese stocks back on the radar

Europe has sought to avoid deflation, or falling prices; a crux that has hobbled Japan's economy for several decades. Japan itself stepped up measures to generate inflation in April 2013, with the Bank of Japan (BoJ) announcing its "quantitative and qualitative easing" program.

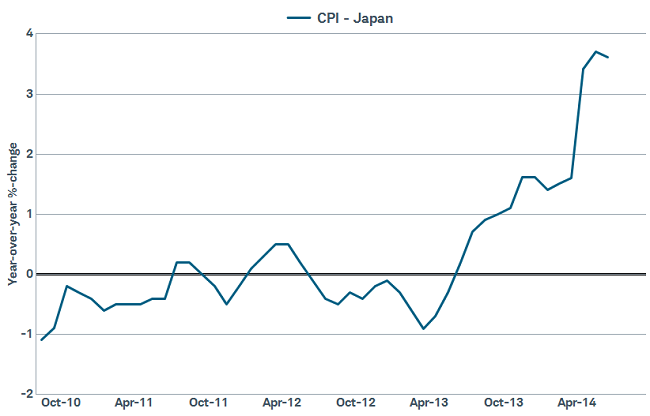

Japan's inflation below 2% target excluding tax hike

Source: FactSet, Ministry of Internal Affairs & Communications. As of Aug. 26, 2014.

Prices are now rising but have yet to meet the BoJ's 2% inflation target. The BoJ said that excluding the impact of the tax hike, core inflation excluding fresh food was 1.3% in May; and while it will moderate in coming months, it will accelerate toward the 2% target later this year. We are skeptical of this prediction, and believe the BoJ may need to extend its QE program beyond its initial 2014 end date to secure a stable and sustainable inflation mindset in Japan.

Japan's economy has longer-term structural issues that are tough to change, but stocks could perform well in the near term. We are encouraged by moves to improve corporate governance and return on equity of companies, as well as the potential for more QE and an allocation shift by Japan's massive public pension plan, the Government Pension Investment Fund (GPIF). We are neutral on Japanese stocks for now, but on watch for Japan's policymakers to move beyond talk to action.

China's slowdown likely to be contained

China's economy has returned to its gradual slowing trend in the third quarter—the "new normal" in China, in our view. The slowdown highlights the balancing act Chinese policymakers are trying to perform; pursing reforms that will likely slow growth, yet not allowing growth to slip too much. This could result in quarterly bumps up and down in the economic data along the way as the government experiments with market-based mechanisms for driving the economy.

Swings in growth have tended to result in outsized moves in Chinese stocks; notably earlier this year when debt payoff concerns resulted in worries about an economic hard landing. However, the relative stability in the economy beat those low expectations and encouraged investors to begin returning to Chinese stocks. Even the dip in the August preliminary HSBC manufacturing PMI failed to derail Chinese stocks, due to the expectation that policymakers are likely to meet the full year 7.5% growth target by enacting stimulus if growth slips too much.

The biggest risk to China's economy, in our opinion, is a sharper downturn in the property market, as the sector influences 23% of China's GDP according to Moody's Analytics. The longer the slowdown, the bigger the risk property developers slash prices, reinforce a buying freeze, and risk loan defaults.

Although Chinese stocks probably need to take a breather after the recent run up, we believe there is more upside and that Chinese stocks will outperform the broad emerging market (EM) universe. Chinese stocks could benefit from further stimulus, attractive valuations, and continued reform moves; such as privatizing state-owned enterprises (SOEs) and increasing the availability of yuan-denominated investment opportunities through the upcoming cross-exchange Shanghai - Hong Kong Stock Connect (SHKSC), or "through train."

We have a neutral rating on the broad emerging market stock universe because we believe tighter credit and an environment of deleveraging in many EM countries is an obstacle for growth and earnings. Also, high hopes for a change in leadership in some emerging countries could disappoint. While EMs have been exposed to changes in Fed policy in the past, the impact could be muted this time if the Fed communicates a gradual rate hike path and if the ECB and BoJ are doing QE, although some EMs are still vulnerable due to large dollar-denominated debt burdens.

So what?

Stocks seem likely to continue their upward momentum although volatility could increase with Federal Reserve interest rate uncertainty combined with midterm elections and geopolitics. An improving economy, decent valuations and a still-accommodative Fed leave us confident that dips should be viewed as buying opportunities. Conversely, Europe is looking worse and we would be cautious in adding new cash at this time, concentrating additional international exposure instead on China and to a lesser degree Japan, always with a diversified portfolio in mind.

© Charlies Schwab

www.schwab.com