Key Points

- The final revision to second quarter real GDP showed a healthy contribution by capex.

- Tide may be turning away from returning cash to shareholders toward capex; pushed by activist investors.

- Capex's leading indicators point to further improvement.

Last week we got the third revision to second quarter real (inflation-adjusted) gross domestic product (GDP), and it jumped to a 4.6% annual rate, up from 4.2%. That is the healthiest pace of growth since the first quarter of 2006 and well above the historical average of 3.3%. The primary drivers of the upward revision were capital spending (capex) and net exports.

Nonresidential fixed investment—the formal definition of capex—was revised up to a 9.7% annual rate; up from 8.4% in the prior estimate. The strength was driven by upward revisions to capex on equipment (from 10.7% to 11.2%), nonresidential structures (from 9.4% to 12.6%) and intellectual property (from 4.4% to 5.5%). This raised capex's contribution to real GDP growth to 1.18 percentage points; up from 1.03 points previously. If you add in residential fixed investment (housing), the total investment contribution to real GDP was 2.87. This is the highest contribution among the four major categories: personal consumption expenditures, gross private domestic investment, net exports and government.

You can see a table of GDP with its components below.

|

% of real GDP |

1Q14 annualized |

2Q14 annualized |

|

|

Consumer spending |

68.2% |

1.2% |

2.5% |

|

Government spending |

18.0% |

-0.8% |

1.7% |

|

Net exports of goods & services |

-2.9% |

(1.7)1 |

-0.31 |

|

Fixed investment |

16.2% |

0.2% |

9.5% |

|

Change in private inventories |

-- |

(1.2)1 |

1.41 |

|

Real GDP |

-2.1% |

4.6% |

|

Source: Bureau of Economic Analysis, FactSet, as of June 30, 2014. 1. Represents contribution to percent change in real GDP.

Admittedly, GDP is lagging; but the pickup in growth from the weather-depressed first quarter is continuing in the third quarter. Consensus estimates for real third quarter GDP are comfortably above 3% and capex trends remain favorable. A composite of the Philly and Richmond Fed capex outlooks jumped 8.6 percentage points in September to a very healthy level. The third quarter average for this composite was 24% vs. 22.6% in the second quarter. According to Cornerstone Macro, there is a 75% correlation between this composite and the year-over-year percentage growth for quarterly real capex.

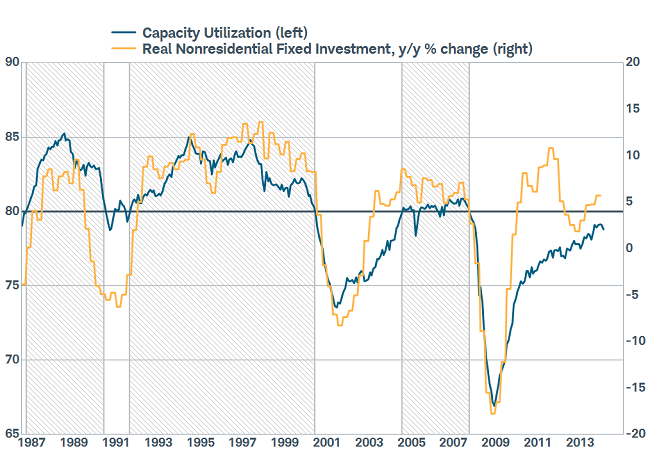

This better capex news is a welcome pickup after years of corporate stinginess when it comes to adding capacity. Since the recession's trough in 2009, capacity utilization has been rising, but remains below the 80% level that typically ushers in a sustainable uptrend in capex, as you can see in the shaded areas in the chart below. We would expect both to continue to lift from here.

Capacity Utilization vs Capex

Source: FactSet, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2014 © Ned Davis Research, Inc. All rights reserved.), Strategas Research Partners LLC. Capacity Utilization as of August 31, 2014. Nonresidential Fixed Investment as of June 30, 2014.

The problem for capex has certainly not been corporate poverty. As seen below, nonfinancial corporate cash as a percentage of GDP is at a post-WWII high.

Corporate Cash Mountain

Source: FactSet, Federal Reserve, as of June 30, 2014. Deposits=checkable deposits and currency, money market mutual fund shares, and time and savings deposits.

And the problem for capex has certainly not been youthfulness. As seen below, the average age of private fixed assets is at a 50-year high.

Serious Age Problem

Source: Bureau of Economic Analysis, FactSet, as of December 31, 2013.

So, where have corporations devoted their spending? They've been biased to returning cash to shareholders via stock buybacks and dividends; helping to explain the booming stock market. As you can see in the chart and table below, the ratio of capex spending to returning cash to shareholders has been nearly the mirror image of what we saw in the prior business cycle (which, by the way, was close to the normal ratio).

Bias Toward Return-to-Shareholders

|

Uses of cash: |

Average |

Average |

|

Invest in business |

58% |

45% |

|

Return to investors |

42% |

55% |

Source: FactSet, Strategas Research Partners LLC, as of December 31, 2013.

One force behind the recent turn up in the pace of capex is pressure from activist investors, who are increasingly pushing companies to refocus their attention on long-term investments vs. short-term financial engineering. The most recent Bank of America Merrill Lynch survey, highlighted in The Bank Credit Analyst, indicated that a record high of nearly 60% of investors preferred that firms increase capital spending; compared with 20% who wanted firms to return more cash to shareholders, and only 10% who wanted them to repay debt. This stands in sharp contrast to the responses in 2009, when 70% of respondents wanted firms to concentrate on improving balance sheets, and only 10% wanted more investment spending.

Looking ahead, most leading indicators of capex point to a further acceleration over the next several quarters. In addition to the age problem, there is declining policy uncertainty: the Economic Policy Uncertainty Index is down from its peaks over the past few years. And the credit spigots have opened further: the NDR Credit Conditions Index is near its best level since the spring of 2006. Low labor productivity is a capex aid as well given that many companies are having difficulty finding skilled workers, which argues for more capex. Finally, given the recent merger and acquisition (M&A) boom, in many industries and for many companies, it's becoming more expensive to "buy it" than "build it."

Finally, the weak pace of capex growth since the recession's trough means there yet exist the excesses that typically lead to recessions. As you can see in the chart below, cyclical spending has only now reached the level at which it used to trough! From those three prior troughs, it was seven years on average before a recession (blue bars) hit.

Cyclical Spending Has a Ways to Go

Source: FactSet, ISI Group LLC, as of June 30, 2014. Blue bars represent recessions. Dots represent years to recession.

The tide is turning. The private sector is largely through its painful deleveraging process; business confidence indexes have turned up; and bank lending—notably commercial and industrial (C&I) lending—is on the rise. The call is not for a boom however. In fact, given that capex booms often usher in higher labor costs and profit margin pressures, it would not be welcome. For now, capex is in "Goldilocks" mode.

© Charles Schwab