Global Fears

Key Points

- Stocks again pulled back as global concerns reached a tipping point. But indicators we look at still point to a renewed uptrend.

- Federal Reserve policy and midterm election uncertainty can add to investor consternation. But the Fed seems to be leaning more dovish and the period following midterm elections has historically been very positive.

- The world is not monolithic and outlooks vary. China, Japan, and India appear to be stabilizing or improving, while Europe and South America are experiencing significant weakness.

Global fears escalated to the point where investors took some risk off the table, with the Russell 2000 dipping into correction territory. Escalating Mideast violence, continued Russian conflict, Hong Kong protests, and even the Ebola virus added to concerns over global economic growth. Taking some profits after a nice run can be a good idea, but we don't see anything that indicates a more sustained downturn is in store.

We are entering a traditionally positive period seasonally for stocks. According to ISI Research, since 1950, December and November have been the highest returning months of the year, on average. Additionally, according to Strategas Research Group—also since 1950, in midterm election years—October has been the best performing month, followed by November and December. The recent selling we've seen could just be setting up for a nice year-end run.

Domestic concerns?

Contributing to the recent selloff was a package of weaker-than-expected economic data, including a decline in consumer confidence, softer housing data, and some slight weakening in manufacturing surveys. But keep these readings in context. For example, the Institute for Supply Management's Manufacturing (ISM) Index fell to 56.6 from 59.0, but that was off of a multi-year high and still robust. Similarly, the new orders component, an indicator of future activity, fell to 60.0, which is still very strong.

ISM-down, but not out

Source: FactSet, Institute for Supply Management. As of Oct. 3, 2014.

A similar story was told by the ISM Non-Manufacturing Index, coming off its best reading since 2005, falling to 58.6 from 59.6, while new orders fell to 61.0 from 63.8—down but still quite positive on both accounts.

Earnings reporting season is also about to kick into high gear and it will be instructive to hear what executives are seeing in their international business, and how the stronger dollar and weaker commodity prices are impacting them. We are seeing increasing signs of corporate confidence, as companies now seem to be shifting their spending from financial engineering—such as stock buybacks—to capital expenditures. (Read more in Liz Ann Sonders article: One Thing Leads to Another: From Dividends/Buybacks to Capex)

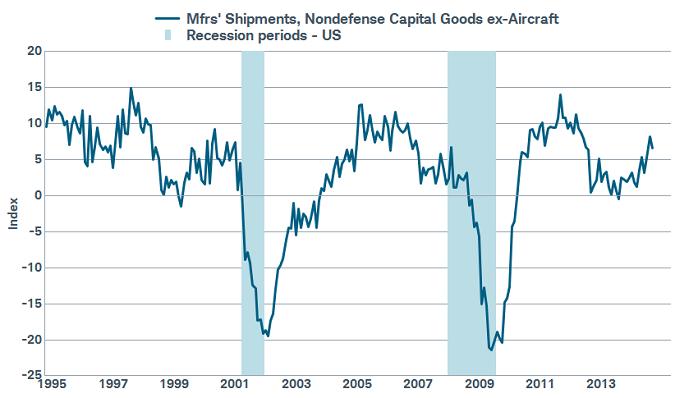

Capital expenditures on the rise

Source: FactSet, U.S. Census Bureau. As of Oct. 3, 2014.

Consumers are also showing signs of life heading into the holiday shopping season. Consumer spending rose 0.5% in September; and while consumer confidence measures have dropped a bit, they remain relatively high. Additionally, the labor market continues to improve, with jobless claims now consistently below 300,000; and the recent employment report showing 248,000 jobs were added and the unemployment rate fell to 5.9%, the lowest level since 2008. As expected, the weak August reading was revised nicely higher—from 142,000 jobs to 180,000—and July was boosted to 243,000 from 212,000.

Consumers are also getting a nice tailwind at an important time of the year as energy prices have fallen. This puts more money into the pockets of shoppers as they consider how much to spend this holiday season.

Lower gas prices a tailwind to consumers

Source: FactSet, U.S. Dept. of Energy. As of Oct. 3, 2014.

Washington worries

Uncertainty surrounding midterm elections and Federal Reserve policy hasn't helped investor confidence. Good news is coming though. First, the election will be completed in the next month, meaning political ads will stop; and attention can be turned to the coming year of potential action on such things as corporate tax rate reform. And the year following a midterm election tends to be positive, with the S&P 500 posting positive returns in the 12 months following every midterm election going back to 1950 (thanks to Strategas Research Partners).

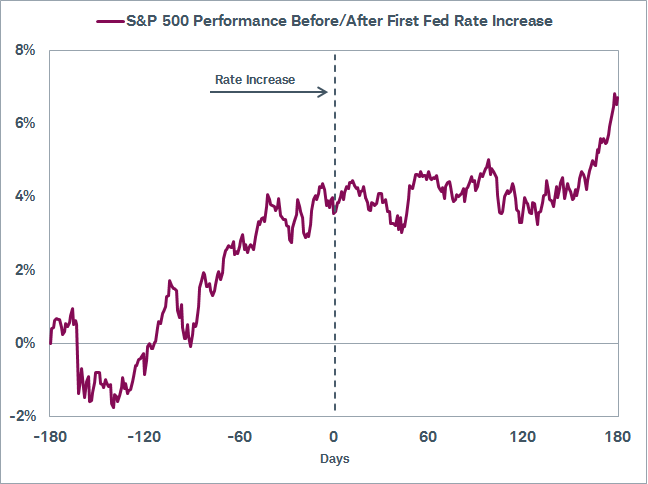

Also, although conflicts exist among the voting members of the Federal Open Market Committee (FOMC), the majority of commentary has leaned dovish lately. This should benefit risk assets; with concerns about slack in the U.S. economy, still-low inflation, and global growth problems seeming to trump the desire of some on the FOMC to hike rates more quickly. And stocks have historically performed relatively well leading up to and during a rate-hiking period.

Fed hikes don't spell doom

Based on fed tightening cycles since 1962. Discount rate used prior to 1984. Fed Funds rate used since 1984. Source: Birinyi Associates, Inc.

Global growth downgrade

On October 7, the International Monetary Fund (IMF) released its latest global growth forecast which incorporates estimates for 189 countries. The 2014 growth estimate of 3.3%, down 0.1% from its forecast in July, is the same pace as in 2013. While in 2015, the IMF expects growth of 3.8%, down 0.2% from earlier expectations. This news comes less than a month after the Organization for Economic Cooperation and Development (OECD) slashed its outlook for the global economy. Accompanying the news, stock markets in the United States and Europe fell nearly 2%, extending a decline that began in early September. The market reaction begs the question: how accurate are these forecasts and should investors expect more market volatility tied to the global growth outlook?

Looking back at recent years, the IMF does not have a great forecasting track record. It has consistently had to lower its forecasts for global growth, typically by a full percentage point over the two-year period until the end of the forecast year. More specifically, from the October forecast of the year before until the end of the following year the IMF had to lower its forecast by 0.1 to 0.6%. This suggests that, if the global economy continues to muddle along at the growth rates of the past few years, more downward revisions may be forthcoming to the current October 2014 forecast for 2015.

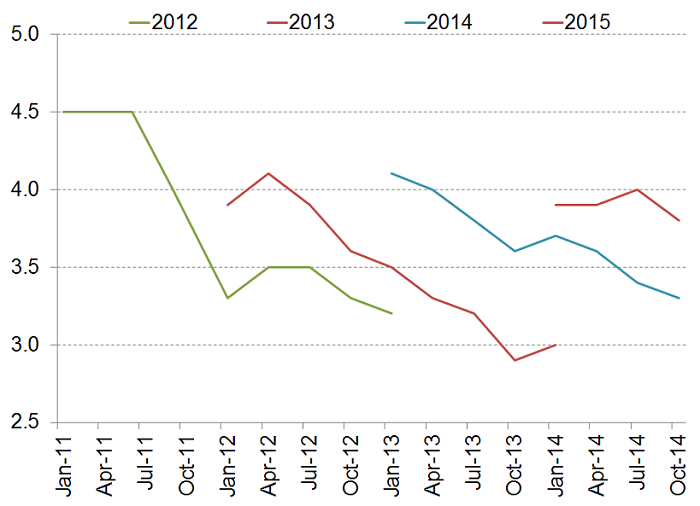

Initial IMF growth forecasts too optimistic in recent years

Quarterly IMF Global Growth Forecasts by Year

Source: Charles Schwab, International Monetary Fund data as of October 7, 2014.

Over the past few years, despite regular downward revisions to growth estimates, global stock markets have produced gains, with the FTSE All-World Index producing a total return of 48% since the start of 2012. In fact, even on the days the IMF released its global growth outlook each quarter since the start of 2012—usually a downgrade—global stocks declined on only one-third of those days, showing investors generally did not find the news all that worrisome.

However, despite this history, the recent stock market reaction is telling and may be a sign of what is to come. If there are more downgrades to the global growth outlook ahead, investors should anticipate that it may result in more market volatility and the potential for declines in some regions. Many stock markets have reached all-time highs as stock values rose on optimism that growth would eventually improve, and risks to growth would fade as central banks provided aggressive economic stimulus. Disappointment by investors in the pace of global growth may increasingly result in market volatility now that stock market valuations are higher, the Federal Reserve is preparing to pull back economic stimulus, and it is becoming clearer that meaningful reforms to growth impediments in some parts of the world are not coming any time soon.

We see a different degree of risk to growth by region. While our assessment of the actual pace of global growth may differ from those of the IMF, in general, the IMF and OECD forecasts by region align with our views of the global economy. Growth is less likely to disappoint in the United States and Asia:

- Economic growth is stabilizing in China and rebounding to the long-term trend rate in Japan.

- Growth is strengthening in India and expected to remain strong elsewhere in emerging Asia.

In contrast, growth in Europe and South America is at greater risk:

- Growth in Europe has weakened—even in Germany—and remains at risk of a return to recession in the near term.

- In South America, the largest economy, Brazil, is expected to make only a slow recovery from recession.

Europe and South America remain weak spots with central banks unable or unwilling to take aggressive enough action along with a rising threat from too low inflation in Europe and too high inflation in South America. This may result in further downgrades to the growth outlook, and heightened volatility and potential underperformance in these markets relative to stronger and better support growth in the United States and Asia.

So what?

Volatility could continue but equity investors should keep the longer-term picture in mind, which we believe is positive. The U.S. economy is improving and monetary policy remains quite loose. The international picture is more concerning but diversification is important across asset classes. We currently favor emerging markets within a diversified international portfolio.

© Charles Schwab