- The bear market in oil prices is largely a positive for the consumption-oriented US economy, but there are caveats.

- Oil's plunge is more a function of increased supply and the stronger US dollar than it is of weaker global demand.

- Oddly, many investors are worried about the stock market because of oil's plunge; but history suggests otherwise.

The topic of oil prices and their impact on the economy and stock market has become a hot topic at client events at which I've been speaking. The most common question is whether the benefits of lower energy prices outweigh the negatives. In short, the answer is probably yes; but the longer answer is more nuanced.

As a consumption-oriented economy—with 68% of US gross domestic product (GDP) driven by consumer spending—lower oil and other energy prices act as a "tax cut" for consumers. But there is the capital spending-oriented angle to the story, too, which is the rub to an otherwise positive story.

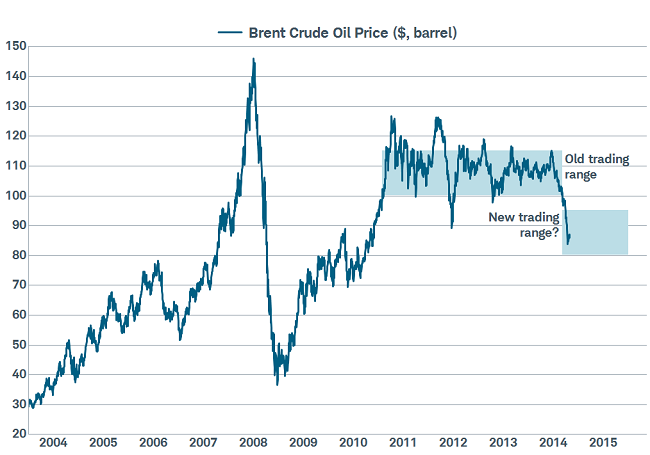

A New (Lower) Range for Brent Crude?

Source: FactSet, GavekalDragonomics, as of October 31, 2014.

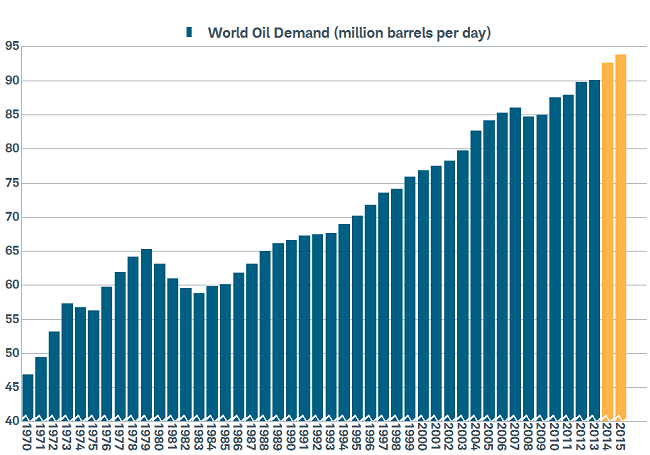

But let's first focus on the "why" of much lower oil prices; specifically over the past six months or so. In light of the focus recently on slowing global growth, many assume the plunge in oil prices has been weak demand-induced. But, as you can see in the chart below, world oil demand is still rising, and hasn't dipped to a level below the prior year since the "great recession" era in 2008/2009.

World Oil Demand Still Growing

Source: FactSet, International Energy Agency (IEA), Ned Davis Research, Inc. (Further distribution prohibited without prior permission. Copyright 2014© Ned Davis Research, Inc. All rights reserved.), as of October 31, 2014. Orange bars indicate estimates.

Yes, weaker demand—notably within China and other parts of Asia—is playing a part. The International Energy Agency (IEA) cut its global oil demand growth forecast to 700,000 barrels per day (bpd) in 2014, from a prior estimate of 1.3 million bpd. This compares to annual averages of 1 million bpd and 1.1 million bpd in 2012 and 2013, respectively. China, which over the past 12 years has accounted for about one-third of annual global oil demand growth, is the main contributor to the demand slowdown. According to GavekalDragonomics, average growth rates in China of 800,000 bpd in the years leading to the 2008 financial crisis are a thing of the past. In 2014, Chinese growth is likely to come in at a comparatively meager 200,000-250,000 bpd.

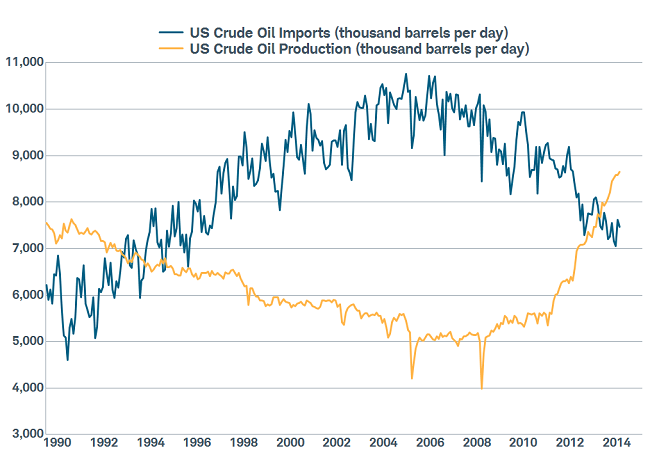

But supply is the bigger story. For several years, investors and market-watchers have chronically underestimated crude oil production by both the United States, and even within OPEC. The United States is now the world's largest oil producer (having taken the top spot from Saudi Arabia this year). Over the past four weeks, US oil inventories have increased by over 23 million barrels. According to Bespoke Investment Group (BIG), that is the fifth largest four-week increase since 1983, and the largest four-week increase since February 2009.

US Production Has Surged

Source: Energy Information Administration (EIA), FactSet, as of August 31, 2014.

There is also the effect of the stronger US dollar on oil prices. There is a strong inverse correlation between the US dollar and oil prices; given that the latter are priced in the former.

But there's another side to oil's slide, and that is its impact on global oil producing economies, as well as on US oil/gas capital spending and the US stock market. Gavekal believes" the tipping point toward some form of action to restrain supply will come if global oil prices fall decisively below $80. A coordinated supply response by OPEC states is possible, but still unlikely. More probable is a unilateral supply cut from Saudi Arabia. But the true floor under oil prices will be established by private oil companies."

As far as the impact on capital spending (capex), oil/gas-related capex is less than 10% of overall US capex. As of this year's second quarter, total nominal US capex hit a peak of over $2 trillion; with oil/gas capex just under $180 billion. However, Strategas notes that employment in energy producing states is 3.4% above their pre-recession peak, while non-energy producing states are below their peak. And GDP is running 1.4% higher per year in energy producing states.

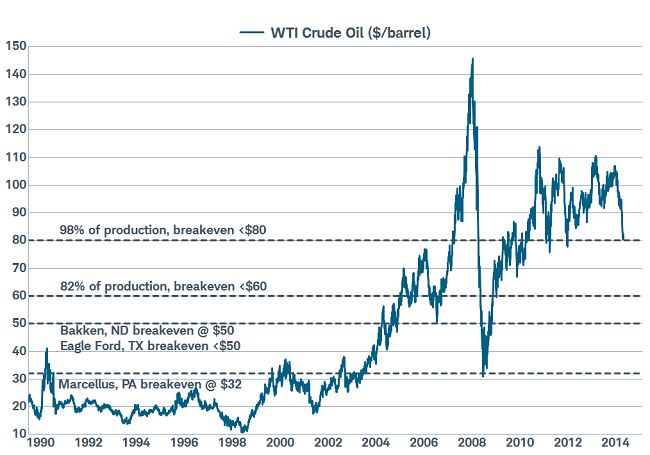

Although the estimates vary widely, using IEA and Petroleum News data, you can see in the chart below that West Texas Intermediate (WTI) oil prices remain above the "breakeven" levels for the largest oil-producing fields in the United States. Globally, according to Gavekal, only about 3% of oil production has a breakeven price above $80.

WTI and Breakevens

Source: FactSet, Petroleum News, Reuters, as of October 31, 2014. WTI=West Texas Intermediate.

But there are ripple effects to consider as well. The employment "multiplier" for energy-oriented growth is fairly large, so there will likely be meaningful secondary impacts if oil/gas capex slows significantly. But the net is that lower prices are good for both US consumers and many US businesses. The Brookings Institute recently noted that the decline specifically in gasoline prices thus far represents a $500 "tax cut" per household.

As far as the impact on the stock market, the latest buzz suggesting that weaker oil is a harbinger of doom for the stock market is likely ill-founded. The current bear market for oil began in September 2013, when the West Texas Intermediate (WTI) crude price peaked at over $110. Since then, oil prices are down about 27%, while the S&P 500 is up about 22% since then. Longer term, according to BIG, during all oil bear markets since 1985, the S&P 500 averaged a gain of 2% (median 5.5%), with positive returns slightly more than two-thirds of the time. In Fact, during 84% of all days that crude oil was in a bear market, the S&P 500 was in a bull market.

In sum, there are offsetting negatives to the positives associated with lower oil prices. If the drop in prices continues, drilling and extraction activity will weaken, which would hurt not only the energy industry and the states which dominate that industry; but the providers of equipment to it as well. But the positive impact on consumers and businesses outside of the energy sector (which is a larger portion of the US economy) will outweigh the negatives.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(1114-7562)

Thumbs up / down votes are submitted voluntarily by readers and are not meant to suggest the future performance or suitability of any account type, product or service for any particular reader and may not be representative of the experience of other readers. When displayed, thumbs up / down vote counts represent whether people found the content helpful or not helpful and are not intended as a testimonial. Any written feedback or comments collected on this page will not be published. Charles Schwab & Co., Inc. may in its sole discretion re-set the vote count to zero, remove votes appearing to be generated by robots or scripts, or remove the modules used to collect feedback and votes.