Key Points

- Records continue to fall for US stocks and we are in a traditionally strong period seasonally. The trend is likely higher but risks exist and overconfidence is a threat.

- Politicians have the opportunity, via tax reform, to add fuel to the equity fire but it is appearing more likely that little of substance will get done. The Fed has brought quantitative easing to a close, but volatility could rise during the initial rate hike stage.

- The European economy is stuck in place, but there is hope from a more aggressive European Central Bank. Likewise, we’re seeing stepped up responses from Asian central banks, which could help to stimulate asset growth.

Please note: Due to the Thanksgiving holiday the next Schwab Market Perspective will be published on December 12, 2014.

Being a bull seems pretty easy with regard to US stocks. The near-correction of mid-October is a distant memory, new records for major indexes are being set on a regular basis, November and December traditionally have been quite positive for the stock market, and the third year of presidential terms is historically the best.

We, too, believe the longer-term trend is higher, but risks exist and more bouts of weakness and volatility like in October are possible. One near-term concern—sentiment, which tends to be a contrary indicator, is elevated, with the Ned Davis Research Crowd Sentiment Poll in extremely optimistic territory. Using sentiment as a timing tool isn’t a great idea, especially with regard to the optimistic side, but it does suggest the market may be more vulnerable to negative catalysts. Additionally, foreign growth remains a concern, although exports make up only 13% of US gross domestic product (GDP), potentially limiting the impact on the United States of modest weakness overseas. In fact, the sluggishness we’ve seen in such areas as the Eurozone, Japan and China, combined with large increases in US supply, have crushed oil prices, a positive for the US consumer.

Economic momentum building

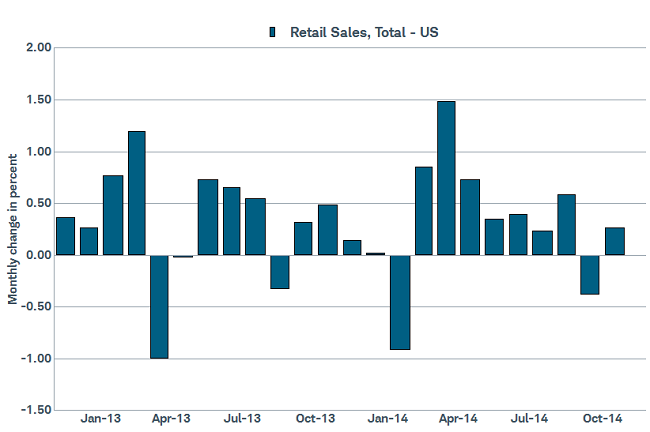

The aforementioned risks aside, we remain bullish, largely due to the continued improvement in the US economy. After a disappointing September retail sales report, October bounced back by posting a 0.3% gain, while ex-autos and gas we saw a strong 0.6% increase and September’s initial 0.1% decline was revised to a 0.1% increase.

Retail sales encouraging

Source: FactSet, U.S. Census Bureau. As of Nov. 17, 2014.

The National Federation of Independent Businesses (NFIB) also reported their survey increased to 96.1, from 95.3; still not overly robust but certainly in the right direction. Capital spending plans from the survey also increased, supporting our belief that capex will help to fuel the next move higher. Initial jobless claims, a leading indicator of employment, remain below 300,000—the longest stretch since 2000. And the quit rate in the Job Openings and Labor Turnover Survey (JOLTS), released by the Bureau of Labor Statistics (BLS), rose to its highest level since before the Great Recession. A greater number of workers willing to quit indicates greater confidence in the job market and should help to pressure wages higher in the coming months.

The latest release of the Conference Board’s Leading Economic Index (LEI) was also a strong 0.9%, above expectations and indicating an accelerating pace of growth. And, the most leading of the regional manufacturing surveys—the Philadelphia Fed Survey—was an upside blowout at 40.8 (double the level of last month). Within that report, new orders were up a very strong 35%, and 56% of respondents said employment would be increased over the next year.

A fly in the ointment

The midterm election results brought less than a day of hope about waning political dysfunction and government getting anything done.. In the above referenced NFIB survey, respondents more often cited government regulation and red tape as their biggest problem over all other pressures.

Have regulations gone too far?

Source: FactSet, Nat'l Federation of Independent Business. As of Nov. 17, 2014.

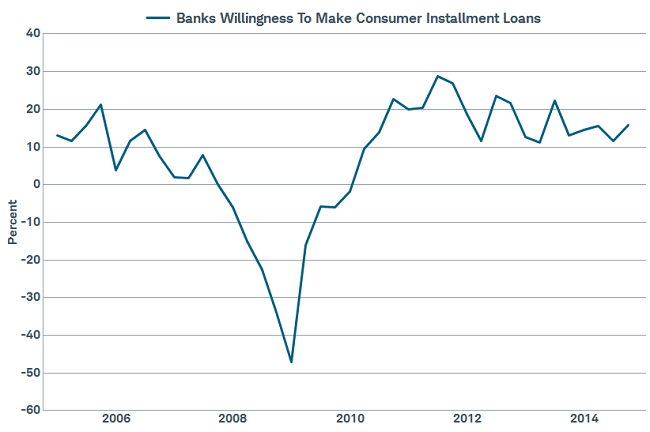

On the subject of regulation, the ongoing uncertainty around the Dodd-Frank regulatory structure may be partly at fault for banks’ muted willingness to lend.

Banks still cautious

Source: FactSet, Federal Reserve. As of Nov. 17, 2014.

Dodd-Frank has 398 total rulemakings that need to be finalized, with only 220 of those having been accomplished to this point according to Davis Polk & Wardwell, LLP. That’s both a lot of rules to keep track of, and a lot to keep waiting on. Further, with new fines being consistently imposed on banks, sometimes for actions encouraged by politicians either explicitly or implicitly, banks may be a little gun-shy about aggressively jumping back into the lending game. Hope for action regarding these roadblocks, or others such as tax reform, seem to be declining by the day. The President’s unilateral action on immigration is likely to fan the fire within Congress and diminish the possibility of party cooperation.

A frozen fall for overseas economies prompts responses

The weather forecasts for below average temperatures and above average snowfall in Europe this winter match the frozen economic forecasts. Last week, Eurostat reported that the Eurozone economy grew 0.2% in the third quarter, after growth of just 0.1% in the second quarter. The economic lift was most evident in the euro area’s two largest economies, Germany and France, as they posted only slight growth in the third quarter after a small contraction in the second quarter. Support for Europe narrowly averting a third recession in six years came from a boost in trade from the falling euro—down almost 11% since early May—as well as falling oil prices, which have dropped more than 25% during the same period.

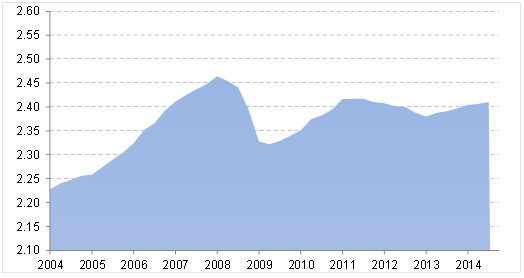

While the third quarter GDP report in Europe was slightly better than economists’ expectations, it shows just how frozen the economies of Europe are. The 18 economies that use the euro emerged from an almost two-year recession in the second quarter of 2013, but since then the region has not been able to post a quarter of growth in excess of 0.3%. Inflation is also near zero at just 0.4% for the year ending October. Europe’s economy has remained frozen in place well beyond the past few quarters: real GDP is in-line with where it was four years ago (see chart below).

Europe’s frozen economy

Eurozone real GDP in trillions of euros

Source: Charles Schwab & Co., Bloomberg data as of 11/19/2014.

In response, the European Central Bank (ECB) is attempting to heat up the economy. In recent months, the ECB has unveiled a number of unconventional measures, including a negative deposit rate, long-term loans to banks, and purchases of assets. Even more aggressive measures were hinted at during this month’s policy meeting, when ECB President Draghi said policy makers commissioned proposals for fresh stimulus. The ECB appears to be warming up to finally implementing the type of quantitative easing (QE) that the U.. Fed ended last month after nearly six years. The deep freeze in the economy is mirrored in European company earnings. European stocks remain under pressure with earnings per share for the economies in the MSCI Europe ex-UK index below the prior peak. Analysts continue to revise earnings growth estimates downward over the next 12 months, as they have every month since the beginning of 2011.

In contrast to Europe, Asian economies were cooler than expected in the third quarter. The -1.6% GDP contraction in Japan was the second consecutive quarter of a shrinking economy following the spring tax hike. As a consequence of the return to recession in Japan, Prime Minister Abe will delay the consumption tax increase scheduled for October 2015 by eighteen months. In the short run, Japanese stocks may benefit from the tax delay, potential for even more growth initiatives, and the recent boost in stimulus from the Bank of Japan. In China, third quarter growth took another step down in economic momentum. In response, the Peoples Bank of China has injected more funding into the banking system. Other Asian central banks have also responded with stimulus in the form of rate cuts (Bank of Korea and State Bank of Vietnam).

The US economy has benefitted from aggressive monetary stimulus, and now the Fed is ending QE. But other parts of the world have been less aggressive, with tepid growth to show for it. As a result, we are finally seeing a stepped up response in monetary stimulus, which may continue to push asset prices higher around the world.

So what?

We remain optimistic that US stocks will likely continue to move higher, but warn against getting overly complacent as a pullback is always a possibility. The US economy is improving, the Fed is erring on the side of dovishness, and both corporate and consumer confidence are growing. The fall in oil should be a net positive for the US and global economy, and we are in a traditionally seasonally positive time of the year for equities. Global economies remain weak, but we are seeing a glimmer of hope from stepped up responses from foreign central banks.

© Charles Schwab