Glancing Back but Focusing Forward

Key Points

- 2014 is on track for another year of gains. There are some obstacles for stocks to climb in 2015, but we are optimistic that the bull market will continue.

- With a new mix in Washington in 2015, no election on the immediate horizon, and the historic tendency for stocks to do well in the third year of a presidential term, suggests optimism about 2015. Meanwhile the Federal Reserve remains dovish but is likely to begin raising rates in 2015.

- Major international economies diverged from the US economy in 2014, although there is hope that a reduction in austerity combined with central bank actions could help major economies converge in 2015.

Please note: Due to the upcoming holidays the next Schwab Market Perspective will be published on January 16, 2015.

Since the 2008 crash, stocks have risen fairly steadily and impressively, with 2014 set to mark another year of solid gains. This may be one of the most doubted rallies in the history of Wall Street, as numerous record highs in major indices have been met with skepticism. Gone are the days of streamers, hats and t-shirts when the Dow passed 10,000.

Unappreciated Rally?

Source: FactSet, Standard & Poor's. As of Dec. 4, 2014.

And although some near-term sentiment indicators are showing heightened optimism, digging deeper reveals quite a bit of investor skepticism with regard to stocks longer term. The “wall of worry” stocks like to climb remains intact and reinforces our relatively positive equity outlook for at least the first half of 2015.

“History doesn’t repeat itself, but it does often rhyme” (Mark Twain)

The end of one year and beginning of another can be a good time to learn from the past and look ahead to the future. We learned again in 2014 that unexpected events should be expected and that a diversified portfolio will help weather these storms. In 2014, we had the “polar vortex,” Russian invasions, quantitative easing ending, Ebola, a midterm election, oil falling off a cliff, and numerous other domestic and international events that could have derailed the stock market, but didn’t. We also learned that it’s good to pay attention to history, as we again saw a sizable stock market decline leading up to a midterm election; which has happened every midterm election year going back to 1962. And, sizable stock gains have typically occurred in the year following the correction, which in this case would take us through October 2015. In fact, traditionally, the third year of a Presidential cycle, which is 2015, has been the best of the four years of the presidential cycle; especially in the first half of the year.

Continuing trends?

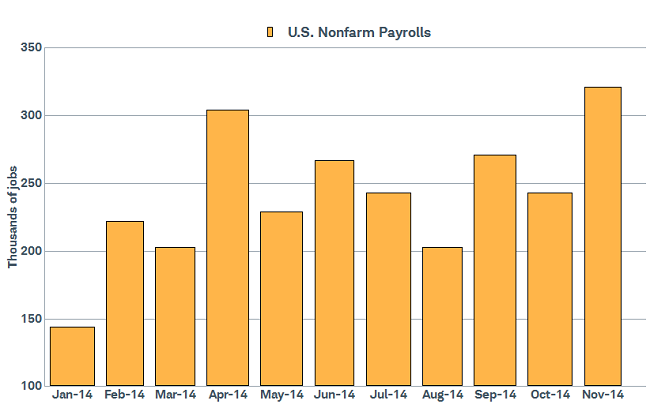

At this point, we have little reason to doubt these trends will continue into 2015, supported by improving US economic growth. Employment has picked up markedly, adding over 200,000 jobs a month for the majority of 2014, capped off with an impressive 321,000 job gain in November; while the unemployment rate dropped from 6.7% in January, to 5.8% in the December release. Additionally, average hourly earnings in November were up 0.4%, while the workweek hours reached the highest level since before the recession.

Employment continues to improve

Source: FactSet, US Dept. of Labor. As of Dec. 4, 2014.

Source: FactSet, US Dept. of Labor. As of Dec. 4, 2014.

Other indications of economic activity also showed solid improvement. The Institute for Supply Management’s (ISM) Manufacturing Index fell slightly in December to 58.7 from 59.0, but that is up from the average of 54 in the first of the year and from the 53.9 averaged in 2013. Importantly for 2015, new orders rose to 66.0, a very strong reading. The service side also looks good, with the ISM Non-Manufacturing Index rising to 59.3 in December from 57.1, and up from the 54.4 averaged in the first half of 2014. A weighted composite of the two suggests US real gross domestic product (GDP) growth of over 4%, although ISM has been overstating growth since the recession ended. Orders were positive here as well, moving from 59.1 to 61.4.

We also have what we believe is a tailwind in the form of lower oil prices. While hurting energy producers, depending on the length and magnitude of the fall, it should help a much larger segment of the economy—energy users. Businesses should benefit from lower input costs and consumers can take advantage of some more cash in their wallets. There is a risk of unforeseen problems associated with such a sharp fall in an important asset class, and we’ve started to see some fissures in the high yield market that are worth watching.

Oil's fall should be a net positive, but risks exist

Source: FactSet, Dow jones & Co. As of Dec. 4, 2014.

Not all is rosy

There are, of course, risks to the market continuing its upward trend and we expect to see more volatility in 2015 as we approach the Fed’s initial rate hike. In addition, geopolitics could flare up at any time; and slow global growth should result in a continued strengthening of the dollar, which could dent some multinational profitability. And while our view is that valuations aren’t overly expensive given the interest rate environment and based on historical averages, they are not cheap, removing some of the cushion we’ve had over much of the past few years. More stretched valuations place increased importance on earnings growth. So while we remain positive on equity market prospects heading into 2015, there will likely be more mood swings between risk-on and risk-off.

Washington focus

The Federal Reserve is likely to hike rates for the first time since before the financial crisis, although they have taken steps to indicate their continued dovishness, and the annual rotation of voting members appears to be ushering in an even more dovish slate of voters. In fact, we add this to our list of potential risks, albeit one that is out of consensus at this point, in the form of an inflation scare. With a dovish Fed, and lower oil prices depressing headline inflation, wage inflation could start to creep higher as the labor market continues to tighten. We don’t think we’ll actually have an inflation problem, but a scare is possible and could jolt markets.

Down the street, a new Congress will be sworn in, with hopes that at least some progress can be made given a new mix and no elections in 2015. Tax and regulatory reform, potential trade deals, health care, immigration, and the minimum wage debate will all be areas of interest for the business community. With opposing parties occupying the Executive and Legislative branches of the government, gridlock seems to be the most likely scenario, but some incremental progress doesn’t seem beyond the realm of possibility.

From divergence to convergence

In contrast to the accelerating growth we saw in the United States, internationally, Japan’s consumption tax hike caused its economy to fall into a recession; while a combination of restrictive fiscal and monetary policy accompanying weak export growth caused the European economy to stall.

After starting the year with a wide range, the widely-watched measure of economic activity known as the Purchasing Managers Indexes (PMIs) for the world’s biggest economies generally converged to just above 50 as the year matured; with the United States a notable exception, rising steadily throughout the year. The 50 level is regarded as the threshold between growth and contraction in output.

United States growth diverged from global trend in 2014

Purchasing Managers Index by Country

Source: Charles Schwab, Bloomberg data as of 12/5/2014

Among the world’s major economies, we foresee a shift toward convergence in 2015. As growth in the United States and United Kingdom stabilizes in 2015—solidifying 2014’s improvements—growth in Japan and Europe should improve. However, it won’t likely be enough to match that of the United States, as increasingly effective monetary policy is joined by an end to the economic drag from austerity.

Stock market performance has also diverged by country in 2014 to-date, with modest losses in US dollar currency terms for Japan’s Nikkei 225, STOXX Europe 600, and the UK’s FTSE 100; while the S&P 500 rose nicely and the US dollar-pegged Hang Seng Index is posting solid gains. While relative performance may converge to some degree along with economic performance in 2015, it is worth noting that in local currency terms all markets mentioned above have posted gains to this point in 2014. The divergence in the value of the US dollar versus other major currencies may be a continuing factor affecting relative returns for US-based investors as 2015 gets underway favoring US over developed international stock markets.

Recently, global equity markets started December with a bout of volatility. As of December 10, stocks in the United States and Europe, measured by the S&P 500 and STOXX Europe 600, were down about 2% in dollar terms. However, the worst of the losses were concentrated in commodity-producing countries in the Americas with Canada's TSX Index, Mexico's IPC Index and Brazil's Ibovespa Index all falling 5-10%. The ongoing decline in oil has been accompanied to a lesser degree by other commodities which are dragging down the stocks of commodity producers. While the commodity price declines benefit consumers, recent events have muted market participants’ enthusiasm over the potential positive impact of these lower prices. The recent events include the lack of new action from the European Central Bank (ECB) at their December 4 meeting, the uncertainty over Greek elections, and the Hong Kong Stock Connect program-driven swings in Chinese stocks. We continue to expect a more aggressive bond buying program from the ECB in 2015, but the potential for the Greek election to exacerbate concerns over a lack of fiscal discipline in Southern Europe makes the outcome less assured and has weighed on European stocks.

So what?

The US stock market appears set for further gains into at least the first half of next year, although risks are elevated with valuations no longer discounted and looming rate hikes. There is hope that ongoing easy monetary policy by global central banks can help to bolster economic activity is areas such as the Eurozone, China, and Japan. But we are somewhat skeptical about stock market performance in developed international countries and favor emerging markets to start out the New Year.

© Charles Schwab