Key Points

- The Fed adjusted its most highly-monitored language; now using “patient” instead of “considerable time.”

- There were three dissenters, although none of them are FOMC voting members next year.

- We expect rates to begin rising in 2015; the stock market to be more volatile, but trending higher; the yield curve to continue flattening; and the US dollar to strengthen further.

The market has spent considerable time considering the words “considerable time,” which have been a fixture in the Federal Open Market Committee (FOMC) statement for a considerable time. The words did remain in the statement, but only as a reference point: “Based on its current assessment, the Committee judges that it can be patient in the beginning to normalize the stance of monetary policy. The Committee sees this guidance as consistent with its previous statement that it likely will be appropriate to maintain the 0 to ¼ percent target range for the federal funds rate for a considerable time following the end of its asset purchase program in October…” (Emphasis on the new and old wording is mine.)

I’m not sure the Fed solved the problem of obsession-about-words, as they just likely changed the obsession from “considerable time” to “patient.” For what it’s worth (perhaps nothing), the use of the word “patient” is reminiscent of the change in language the FOMC initiated five months in advance of the first rate hike 2004.

Not on board

Notable were the three dissents to the decision about the statement. However, important is the fact that none of the three are voting FOMC members next year.

- Richard Fisher, the Dallas Fed President, “believed that, while the Committee should be patient in beginning to normalize monetary policy, improvement in the US economic performance since October has moved forward, further than the majority of the Committee envisions, the date when it will likely be appropriate to increase the federal funds rate.”

- Narayana Kocherlakota, the Minneapolis Fed President, “believed that the Committee’s decision, in the context of ongoing low inflation and falling market-based measures of longer-term inflation expectations, created undue downside risk to the credibility of the 2 percent inflation target.”

- Charles Plosser, the Philadelphia Fed President, “believed that the statement should not stress the importance of the passage of time as a key element of its forward guidance and, given the improvement in economic conditions, should not emphasize the consistency of the current forward guidance with previous statements.”

There was limited reference to the plunge in oil prices in the FOMC statement other than, “…expects inflation to rise gradually toward 2 percent as the labor market improves further and the transitory effects of lower energy prices and other factors to dissipate …” We like the fact that the Fed chose not to reintroduce language that “strains in global financial markets” pose downside risks to the outlook despite the trouble in Russia and Greece, the plunge in commodity prices, and the increase in high yield spreads. This likely signals that the Fed does not see these events as worrisome longer-term; with oil price declines offsetting the rise in high yield spreads.

Forecasts

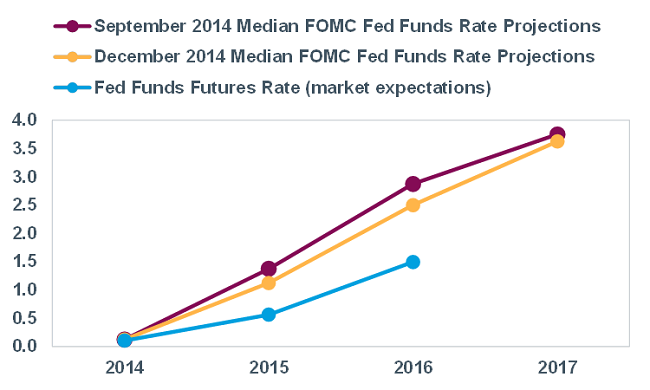

The FOMC also adjusted down their forecasts of the fed funds rate trajectory:

- 2015: from 1.375% to 1.125%

- 2016: from 2.875% to 2.5%

- 2017: from 3.75% to 3.625%

However, as you can see in the chart below, the Fed’s forecasts remain well above the market’s assumptions as per the fed funds futures market.

Fed Lowers Projection Dots

Source: Bloomberg, Federal Reserve, as of December 17, 2014.

The central tendency projections (CTP) for the unemployment rate (UR), real gross domestic product (GDP) growth and core personal consumption expenditures (PCE)—which is the Fed’s preferred inflation measure—were also adjusted:

Source: Federal Reserve as of December 17, 2014.

Press conference

In Fed chair Janet Yellen’s opening remarks, she stated that the FOMC does not expect to start the tightening process for “at least the next couple of meetings,” although she noted that the statement is “data dependent.” She noted that virtually all FOMC officials expect tightening to begin at some point in 2015, which is our view as well. During Q&A, she pushed back on the notion that the Fed might consider having a press conference after every meeting; specifically refuting the idea that the Fed feels compelled to announce rate hikes only during meetings with associated press conferences.

In sum, regardless of the obsession around the specific words used, the statement is somewhat par-for-the-course; and supports our consistent view that rates should begin rising at some point in mid-year 2015, that the US dollar will remain strong, and that the yield curve should continue to flatten (as a result of benign inflation keeping longer-term rates fairly low). Although our view is that the stock market will be at the mercy of more frequent mood swings, the secular bull market we believe began nearly six years ago should persist in 2015.

© Charles Schwab