Should I Stay or Should I Go: Global Diversification Could be 2015’s Winner

Key Points

- Last year ended on a weak note for US equities; and January continued the trend

- Divergences will remain a theme and likely keep volatility elevated

- US investors haven’t felt the need to diversify globally…they should

From my dual perches at Schwab and Windhaven Investment Management, there are three themes for this year about which we’ve been speaking and writing: volatility, divergences, and Main Street being a happier street than Wall Street. This year doesn’t appear to have the markings of a finale of the secular (my view) bull market that began nearly six years ago; but it could be a year marked by a greater frequency of corrective phases and “black swan” events. It’s also likely to be a year when global diversification is appreciated more than in the past several years.

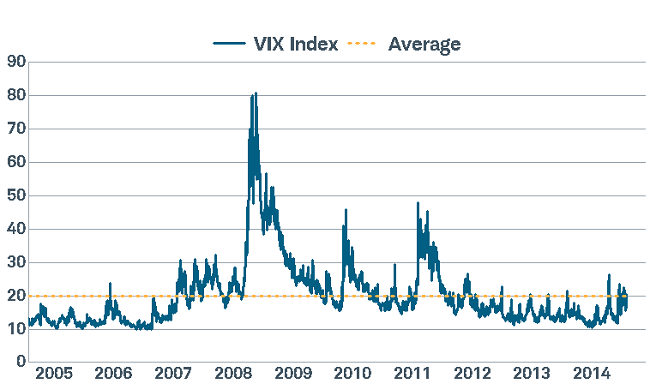

Volatility’s back

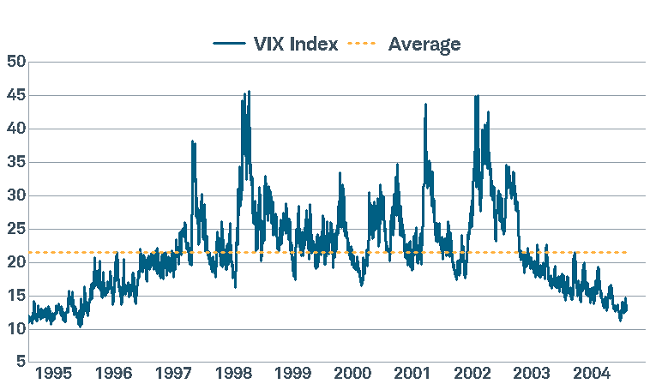

You can see the pick-up in volatility in the first chart below; which shows that the CBOE Volatility Index (VIX) has had several spikes above its 10-year average since last October. Because we’ve opined that this year could look a bit like the 1997-1998 period—when US growth surpassed much of the rest of the world, leading to US dollar strength, but also to some important global crises—I also show a chart of volatility for the prior 10 years.

Volatility over past two decades

Source: FactSet, as of January 30, 2015.

Between 1997 and 1998 the market had to weather the Russian and Asian currency crises, which led to the implosion of Long Term Capital Management (LTCM). In July/August 1998 the S&P 500 dropped almost 20%—barely missing the label of a cyclical bear market.

Divergences abound

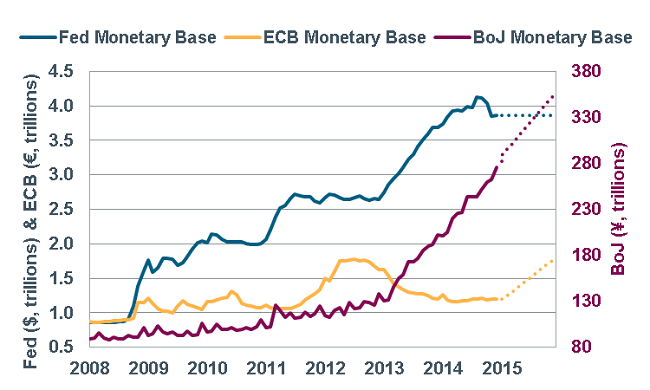

The most powerful divergence globally has likely been among global central banks, with the US Federal Reserve having ended quantitative easing (QE); while the Bank of Japan and European Central Bank (ECB) in full easing mode, including QE.

Global Central Bank Divergences

Source: FactSet, as of December 31, 2014. ECB=European Central Bank. BoJ=Bank of Japan. Dotted lines represent 2015 estimates provided by Strategas Research Partners LLC.

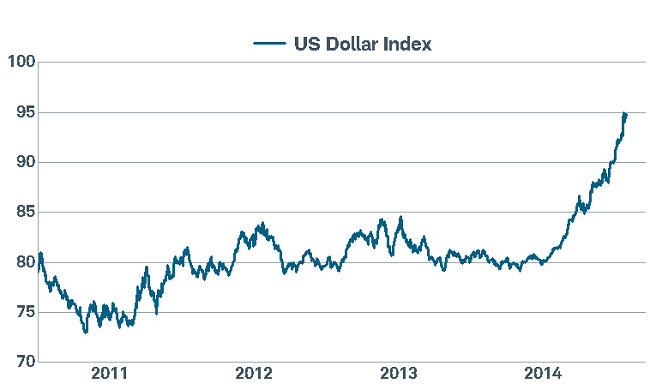

Volatility tends to accelerate as monetary policy becomes less easy and/or when an initial rate hike is on the horizon—the case in the United States. More recently, other global central banks have stepped up their easing since the Fed began tapering QE. In January alone, 14 countries cut rates or loosened borrowing standards. The combination of tighter US policy and easier global policy has led to the surge in the US dollar; another similarity to the 1990s.

US Dollar on a Tear

Source: FactSet, as of January 30, 2015.

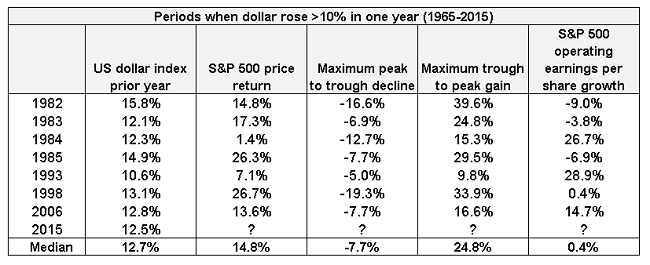

In general, a stronger dollar has historically been a favorable backdrop for both the US economy and US equity indices. However, as you can see in the table below, although the stock market has had a perfect track record of positive returns following years during which the dollar was up more than 10%; the intra-year maximum “drawdown” was meaningful. In sum, the message is that strength of the dollar may be considered a good thing longer-term; but it can cause major headaches in the short-term.

Source: Bespoke Investment Group (B.I.G.).

Putting a value on earnings

One of those headaches—as seen in the final column in the table above—is the hit to multi-national earnings. Profits have been fraying; largely due to the strength of the dollar and its commensurate currency translation hit, but also due to the crash in oil prices and weak global growth. So far this earnings season, the spread between companies raising vs. lowering earnings estimate guidance is -8.6 percentage points, according to Bespoke Investment Group (BIG). This is by far the worst reading of the current bull market; and it’s close to the two extremely negative levels seen in the fourth quarter of 2008 and the first quarter of 2009. Caveat: a negative guidance spread is nothing new for the bull market; although the spread so far this season is much worse than those in prior years. It has a “companies throwing in the towel on 2015” look to it.

With US equity market valuations marginally above long-term median levels, the onus is on earnings to do more of the market’s heavy lifting…a heavy task in light of the aforementioned pressures.

Sticky optimism is something new

January’s weakness was unsettling, although not a surprise to us for much of what’s already been discussed above. For the second year in a row, the S&P fell in January. It’s now down about 5% from the late-December peak. And it’s been a volatile start to the year…18 of last month’s 20 trading days experienced a >1% move in the S&P 500; and 13 trading days experienced a >100 point move in the Dow Jones Industrial Average.

More surprising than the market’s gyrations though is the sentiment around them. Despite the recent volatility, individual investor sentiment is not sinking. According to the weekly survey from the American Association of Individual Investors (AAII), bearish sentiment actually declined from about 31% to 22%; and bullish sentiment rose from about 37% to 44%, which is above the bull market average to-date of less than 39%.

The same can be seen looking at Investor’s Intelligence (II), which is a survey of professional newsletter writers. The latest survey showed a “Bull Ratio” —bulls/(bulls+bears) — of over 76%, near the upper end of its historical range. SentimenTrader.com (ST) highlighted times in the past when the S&P 500 pulled back in consecutive months (with a total loss smaller than -5%), while the II Bull Ratio remained above 50%. Generally, this persistent optimism in the face of declining prices led to weak returns for the market in the months ahead.

ST pointed out that the main culprits were the years 1976/1977, 2000 and 2007. The 2007 occurrence occurred about three years after the 2004 spurt following the initial push off the 2003 bear market bottom. And now, we’re seeing a similar setup about three years after the 2012 instance, following that spurt off the 2009 market bottom. Food for thought.

US to shine less brightly in relative terms

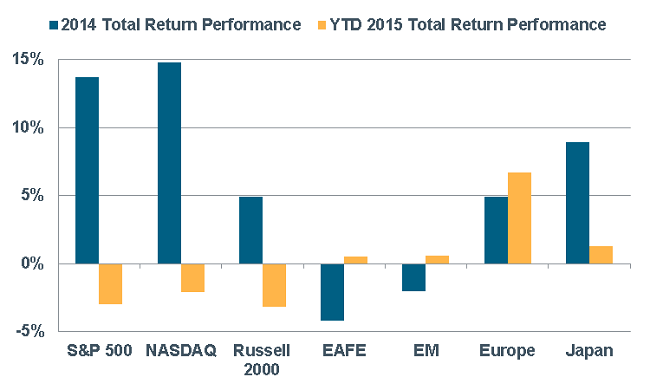

I have not become a market bear; but am much more cautious than at any point in the past few years. It’s in keeping with Schwab’s neutral recommendation on US stocks (and our overweight recommendation on emerging markets); believing investors may benefit from global diversification more this year than during the past few years. You can see in the chart below how quickly performance trends can reverse. The first bar for each asset class represent full-year 2014 performance, and the second represents January 2015.

Non-US Equities Rebounding

Source: Bloomberg, FactSet, as of January 30, 2015. EAFE=MSCI EAFE Index (Europe, Australasia, Far East). EM=Morgan Stanley Capital International (MSCI) Emerging Markets (EM) Index. Europe=EURO STOXX 50 Index. Japan=Japan Nikkei 225 Index.

There was about a 17 percentage point difference between the S&P 500’s performance and non-US global equities’ performance in 2014; courtesy of stronger performance from both US stocks and the US dollar. This was the widest dispersion for any year since 1992, according to Bloomberg. There were four other periods since 1970 when the US market diverged from international equities at a similar rate as in 2014. Each time, the MSCI All-Country World ex-US Index was up in the following year—beating the S&P 500 by an average 14%.

What a difference a month makes.

Global diversification

The world’s economies and central bank policies are diverging—part of the rebalancing necessary for the world to deleverage from its 50-year debt supercycle. But it’s likely to be a volatile process; with central banks trying to thread the stability needle very carefully. Global diversification is likely to become increasingly important.

(c) Charles Schwab