Self-Sustaining US Economy…So What Now?

Key Points

- The US economy appears to be firmly in self-sustaining expansion mode. While welcome, that could make near-term gains in the stock market harder to come by as the expectation bar has been raised.

- The Federal Reserve is reflecting belief in the strength of the economy by not appearing to waver on its plan to raise interest rates this year. Likewise, talk in Washington is centering on scuttling the sequester agreement and increasing spending due to the strengthening economic outlook.

- While Greece remains in the headlines, the Eurozone appears to be quietly improving. Meanwhile, there is an interesting currency battle underway as global central banks attempt to battle deflation threats.

For the past several years investing has revolved around a fairly consistent story. The US economy has been recovering, the Fed has been easing, and there haven’t been many attractive options—therefore—buying US stocks was a rewarding call. That narrative has worked well but the story appears to be changing. The US economy is expanding in a self-sustaining fashion, the Fed is looking toward tightening, and the options outside of the United States are becoming more attractive in our view.

What does this mean for investors? First, we are not turning bearish on US stocks, but believe that gains could be harder to come by, accompanied by heightened volatility. Stocks typically like to climb a “wall of worry” and expectations for the US economy are higher than they have been in several years; meaning a relatively low “wall” for the time being. Second, for investors who have remained well-diversified both by sector and asset class (globally), there’s likely not much to do except stay the course. But for those investors who have let their portfolios tilt heavily toward US equities, we believe now would be a good time to create a more balanced portfolio by adding some international equity exposure.

Self Sustaining

We agree with Treasury Secretary Jack Lew’s comment to Congress about the United States having entered a period of “self-sustaining” growth (Financial Times, February 4, 2015). The Institute for Supply Management’s (ISM) Manufacturing Index continues to show expansion with the latest reading at 53.5; although that was down a bit from the previous month. The services-oriented ISM Non-Manufacturing Index—representing a much larger share of the US economy—rose to 56.7, while orders strengthened to 59.5.

The job market reinforces the self-sustaining view as initial jobless claims remain consistently below the key 300,000 level (albeit with some volatility). Also, the economy continues to create jobs, with another 257,000 being added in January, while the previous two months were revised higher by 87,000 jobs collectively. The unemployment rate did tick up to 5.7%, reflecting more people entering the workforce as the labor participation rate rose. And the strength in the labor market may be starting to show up in at least a modest increase in wages as the Employment Cost Index (ECI) showed a 2.3% year-over-year gain in the fourth quarter of 2014; while average hourly earnings rebounded from December by posting a 0.5% gain in January.

Wages showing signs of rising

Source: FactSet, U.S. Dept. of Labor. As of Feb. 6, 2015.

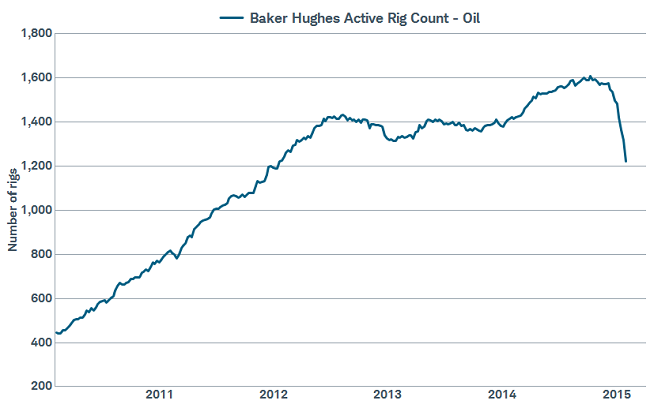

And although personal spending fell by 0.3% during December, January’s auto sales were solid, posting a 9% gain year-over-year, bolstered by truck and SUV sales, apparently spiking in response to falling oil prices. We continue to believe the fall in oil prices will be a net positive for the US economy, but there are negative shorter-term effects as well; with layoffs occurring throughout the energy space as well as related industries, and capital spending plans in the energy sector being slashed. We aren’t going to attempt calling a bottom in oil, but companies are certainly responding aggressively, which should eventually curtail excess supply. Rig counts have fallen precipitously, but US oil field production recently hit a record high according to the Energy Information Administration (EIA).

Companies react to oil fall

Source: Bloomberg. As of Feb. 6, 2015.

But oil production takes time to respond

Source: FactSet, U.S. Dept. of Energy. As of Feb. 6, 2015.

Although there will undoubtedly be some near-term dislocations as a result of the sharp fall in oil prices, we believe it is a net benefit to the US economy given its consumption orientation. But for now, consumers appear to be taking a cautious approach; with estimates from Visa and MasterCard estimating that only 25% of energy savings is going toward spending, while the rest is going to savings and paying down debt. As the lower price of oil becomes more entrenched, and wages continue to rise at a more consistent rate, consumers will likely become more comfortable with increasing spending, helping to fuel economic growth, and perhaps provide upside surprises in the second half of 2015.

Housing as an offset to capex

One recent bright spot has been housing, with a huge surge in household formation associated with the recently-rapid improvement in job growth for the key 25-34 year-old bracket. Household formations are now running well ahead of home construction, suggesting demand that may need to be met with increased construction. As the partner to non-residential construction within the investment component of the US economy, housing could serve as a positive offset to the negative implications for capex from the plunge in oil prices.

Steady Fed while Congress looks to scrap sequester

The Federal Reserve remains positive on the US economic outlook, while giving a nod toward international concerns. It appears to be on track for raising rates at some point this year, although the timing could be delayed should global drama escalate or the rising dollar become detrimental to the US economy. But investors need not fear, because although the path toward an initial rate hike can have a few potholes, the stock market has historically performed fairly well. And after watching many global central banks walk back recent rate hikes due to unexpected economic weakness, the Fed seems set on a very gradual pace of rate increases assuming the economic data is confirming.

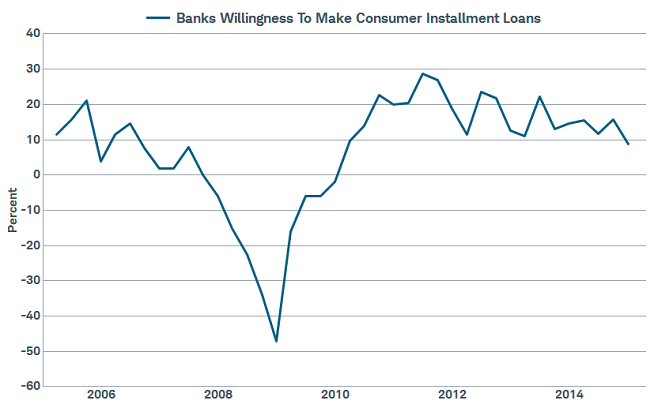

The Obama Administration released its budget proposal, which included scrapping the spending limits put in place during the sequester negotiations, while proposing increasing wealth redistribution in the United States. Various business survey data—including out of the National Federation of Independent Business (NFIB)-- show the regulatory environment as a headwind; certainly within financial sector, as evidenced by still-timid lending.

Banks still skittish

Source: FactSet, Federal Reserve. As of Feb. 6, 2015.

Europe’s glass seen half full

The showdown in Europe with Greece has remained the big global news story in recent weeks. Greece’s new leadership proposed a debt swap with new terms; but European leaders made it clear they expect Greece to honor its existing bailout commitments and to request an extension of the current bailout program. As both sides work toward a framework for compromise, the showdown is being felt most acutely by the Greek banks. This is due in part to the European Central Bank (ECB) upping the ante on negotiations by announcing it will no longer accept low-rated Greek government debt from banks as collateral for funding. This has forced Greece to tap the more costly “emergency liquidity assistance” from the ECB.

Despite the showdown and risk of a financial catastrophe in Greece, the Eurozone is expressing few signs of worry that a crisis may develop. In fact, many of the Eurozone’s economic participants are positively upbeat:

- Surveys of consumer and business confidence in the Eurozone are on the rise. The German ZEW survey of expectations for the Eurozone economy jumped further in January to near the highs of the past six years, and German economic confidence rose to levels rarely exceeded in the past 15 years.

- Investor sentiment has picked up. The Sentix survey of Eurozone investor sentiment increased to an above-average 12.4 in February 2015, after averaging 0.24 from 2002 until 2015.

- European stocks are rallying. The STOXX Europe 600 Index has posted an 8% year-to-date gain through February 6 (though in US dollar terms it amounted to only 1%); pushed higher by a rise in price-to-earnings ratios not seen since the 1998-2002 dot-com bubble.

Eurozone investors upbeat

Source: Bloomberg data as of 2/9/2015.

Eurozone upbeat on economic prospects

ZEW Survey: Assessment of Economic Conditions in Germany

Source: Bloomberg data as of 2/8/15.

The glass half-full perspective seems to be based in part on the additional stimulus, announced by the ECB in January, working to revive growth. For our perspective on the risks to this outlook see our recent comment: Why ECB QE May Not Boost European Stocks For Long. Another reason for the optimistic outlook is that despite lackluster job and wage growth, retail spending has picked up in recent months as oil prices have fallen. As expectations rise, Europe’s stock markets will increasingly depend on improvement in economic and profit readings.

Non-traditional currency war

While the focus of many market participants remains on the Fed and when they may begin to raise interest rates, another global theme impacting the markets has been rate cuts and other non-traditional policy actions by foreign central banks.

- The ECB will launch its massive bond-buying program announced last month, and the Bank of Japan (BoJ) said last month it would continue to aggressively expand the money supply.

- China announced its first system-wide reserve requirement ratio cut since May 2012 to improve credit availability. It served as a second step following a rate cut, to lower the cost of credit late last year in a series of efforts intended to address growth, liquidity and disinflation headwinds.

- A rate cut by Australia’s central bank followed cuts from Canada, Switzerland, Russia, India and others since the start of the year. Some have even cut rates into negative territory.

The central banks of seven of the world's 10 biggest economies are stepping up their stimulus efforts so far in 2015, while the United States and United Kingdom have paused. Only Brazil is currently raising rates, despite a weak economy, as it seeks to contain inflation and stem capital flight.

A traditional currency war focuses on countries seeking to lower the value of their currency to drive exports and lower imports of goods from other countries. But, as global inflation continues to slow, a non-traditional currency war has emerged, where central banks of countries representing about one-third of the global economy are engaging in policies that result in currency devaluations that export deflation to, and import inflation from one another. More central banks are being dragged into the fray with the Bank of Canada enacting a rate cut last month for the first time in almost six years.

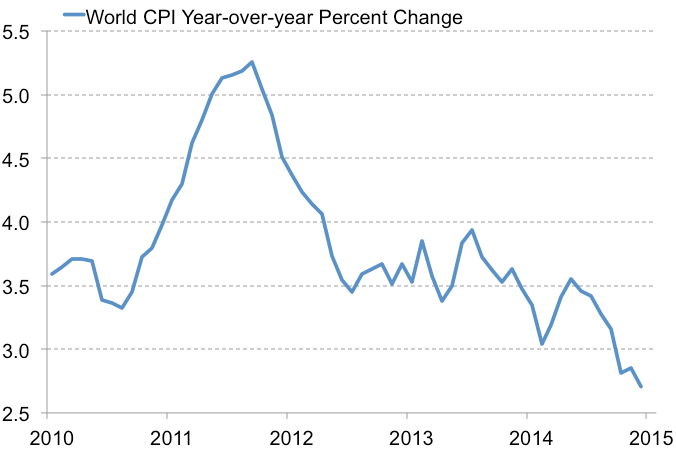

Despite the actions, for every currency that declines another rises against it, and global inflation continues to decline. While markets seem to welcome the actions, it is stronger demand, rather than cheaper currencies, that is the only real cure for weak prices.

Worldwide pace of inflation remains in a downtrend

International Monetary Fund World Consumer Price Index

Source: Bloomberg data as of 2/10/15.

So what?

The US economy appears to be in a self-sustaining phase of the expansion, which could mean more volatility as the Fed embarks on a tightening cycle. We remain confident the secular bull market is intact, but volatility has risen and we suggest investors who are over-exposed to US equities consider global diversification, with a preference for emerging markets. Europe appears to be stealthily improving, but Greece remains a flash point and Eurozone equity markets may have gotten ahead of themselves a bit.

(c) Charles Schwab