Will a Spring Thaw Lead to a Stock Surge?

Key Points

-

US stocks have struggled to regain upward momentum, but a rebound in economic activity should help. Valuations are somewhat extended, which could make further gains tougher to come by.

-

The Federal Reserve removed “patient” from its statement but went on to assert that it wasn’t impatient. The stronger dollar and weaker economic data over the past two months, along with little inflationary pressure, suggest that it will likely be the second half of the year before the initial rate hike.

-

Improving economic prospects overseas have US investors moving some funds into non-US equities. Meanwhile, the global growth leader has shifted from China to India.

US markets have seen a lot of action, but little actual movement over the past month. The S&P 500 has gone 27 consecutive trading days without back-to-back up days—the longest stretch since 2001.Weaker economic data, combined with uncertainty around Fed policy has dented investor optimism. Although stocks and bonds rallied, and the dollar fell immediately following the Fed announcement, (read more from Kathy Jones in The Fed’s Message: Slower and Lower on Rate Hikes), the reaction was short-lived. And unfortunately it appears to us that we may be in for more of the same in the near term, with volatility increased but little actual momentum being generated.

A consolidation of gains seen over the past year isn’t necessarily unwelcome and it may help to forestall a more severe correction. So while the Fed removed patient from its statement, investors may have to be just that in the coming months as we work through the effects of a frigid February, the west coast port strike, the consequences of a higher dollar, and the sharp fall in the price of oil. But investors also need to brace for sharp counter-trend moves in both the dollar and oil, as we’ve seen recently.

Earnings at risk

As we’ve noted, earnings expectations for the current quarter have been reduced sharply, reflecting concerns over both the rising dollar and the impact of lower oil prices. Expectations are for S&P earnings to decline in both the first and second quarters. This provides the opportunity for upside surprises but forecasting earnings in such an environment as this is quite difficult, leading to more uncertainty in the market.

The sharp rise in the dollar has impacted both earnings expectations and economic data, especially on the manufacturing side, with regional manufacturing surveys showing softness. And while we think the dollar will continue to strengthen, which has typically been a positive for stocks, we blieve the recent dovishness by the Fed and its focus on currency movements has helped to slow the rate of increase, which should help to calm reactions to currency moves.

Earnings don’t tend to fall into negative territory outside of recessions. But there have been two notable exceptions: 1986 and 1998. Both occurred due to a strong dollar and weak oil prices, and were not ultimately recessionary. We think today’s case is similar.

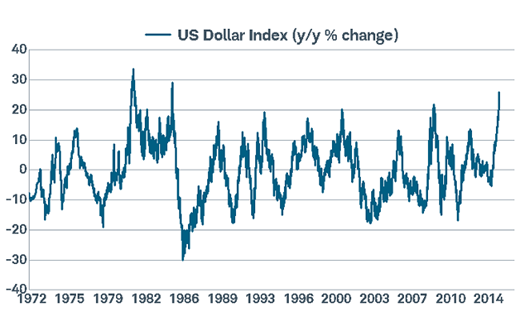

Sharp gains in the dollar may slow.

Source: FactSet. As of Mar. 25, 2015.

The sharp move in the other direction for oil has also caused some consternation among investors. Although most, including us, think the fall in energy prices will be a net positive for the economy, it has resulted in a reduction in payrolls, capital spending plans, and earnings in the energy space. And one of the major positives expected—a boost to consumer spending—has yet to really come to fruition. Retail sales have been relatively disappointing in recent months as it appears consumers have been more interested in saving or paying off debt, at least in the initial stages of the drop in oil. History, however, has shown that it often takes a sustained period of lower prices before consumers adjust their spending habits upward.

We don’t attempt to forecast oil prices, but many of the conditions supporting a bottoming process historically have kicked in recently. One of those conditions is sharp and high-magnitude swings in oil prices on a day-to-day basis. Another has been the plunge in the rig count. That said, it seems that many of those idled rigs weren’t all that productive as US production has continued to rise. Additionally, in the US there are reports that storage facilities are quickly approaching capacity, meaning oil with nowhere else to go could soon be flooding the market; a negative for prices. Finally, there is always the wildcard of geopolitics, and the latest eruption involving Yemen and Saudi Arabia caused a swift upward shift in the direction of oil.

Rig count down, but production keeps on growing

Source: FactSet, U.S. Dept. of Energy, Bloomberg. As of Mar. 19, 2015.

Economic data should turn

As noted, we do think some of the extreme movements we’ve seen in the dollar and oil could recede, helping to calm investors. Additionally, the weather will be warming up, which should help economic data in the coming months. Industrial production in February was a disappointing 0.1% gain after January was revised lower to a 0.3% decline. Not surprisingly, the readings were held down by weakness in manufacturing, which confirms other soft readings on manufacturing seen lately.

Industrial production has been disappointing to start the year

Source: FactSet, Federal Reserve. As of Mar. 19, 2015.

The housing market has been mixed, with housing starts dropping a surprising 17% in February, while the National Association of Homebuilders –Wells Fargo Housing Market Index fell to 53, although that was up slightly from the 2014 average of 52. The weakness, however, appears at least somewhat weather related, and there was a hopeful sign in the building permits number, which showed a 3% gain. And new home sales were particularly strong—up 7.8% in February to the highest level in 7 years. With the spring selling season coming up, interest rates remaining quite low, the job market continuing to improve, and a benefit from lower energy prices kicking in further, we believe we’ll see improvement in the housing market in the next several months.

We also believe that manufacturing data will show improvement in the coming months as the port backup gets resolved and businesses get a better handle on managing the stronger dollar and yield benefits from lower energy costs.

Fed no longer “patient”…but still patient?

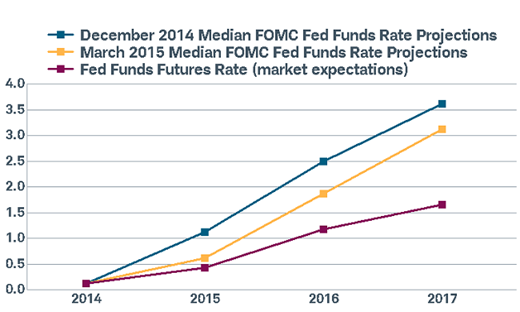

The Federal Reserve removed the word “patient” from its official statement, giving it more flexibility and removing any perceived calendar-oriented constraints. The remainder of the statement, and the press conference, served to try to convince investors that it would indeed be patient. Perhaps more notable then the removal of “patient” was the Fed’s lowering of its forecast “dots” (the Fed’s expectation for the fed funds rate at the end of the next 3 years). Those dots moved closer to the market’s expectations, although there remains a wide gap in 2016 and 2017.

Fed Lowers Rate Expectations

Source: Bloomberg, FactSet. As of Mar. 25, 2015.

We currently believe the first rate hike will be in the second half of the year and subsequent hikes will be slow and small. However, inflation concerns, especially if wages accelerate would likely cause the Fed to be more aggressive than is currently anticipated. There are some indicators already flashing, including announcements from major retailers of higher wages; while broad wage gains typically start to occur after the unemployment rate hits 5.5%, which is where it stands at the present time.

U.S. Investors Send Money Abroad

U.S. investors bought a net $10 billion of European and $4.4 billion of Asian stocks in January, according to the latest data from the U.S. Treasury International Capital System. The strong pace of net inflows into overseas markets appears to have continued with the Tokyo Stock Exchange reporting five-straight weeks of net buying by foreign investors.

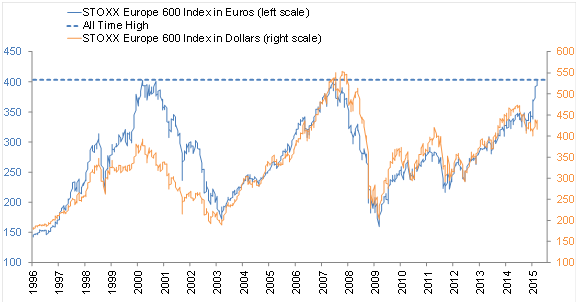

Economic growth in Europe continued to improve in March, according to the latest Purchasing Manager Index data. The improvement in economic data combined with the European Central Bank’s (ECB) quantitative easing (QE) announcement has appeared to help ignite interest in European equities from US investors, and pushed Europe’s stocks back to all-time highs. The STOXX Europe 600 Index again reached the peaks seen in 2000 and 2007. Though, from the perspective of US investors, in dollar terms the index still has a way to go to make a new high.

Europe’s stocks back to all-time highs

Source: Charles Schwab, Bloomberg data Mar, 20, 2015.

Factors boosting Europe’s growth improvement include:

- The decline in oil prices, which has lifted consumer spending on non-energy goods.

- The decline in the value of the euro which is helping to drive exports.

- Signs that loan demand is picking up, including the surprisingly strong demand by banks for March’s targeted long-term refinance operation (TLTRO) by the ECB.

- The end of the drag on growth from budget austerity in the form of spending cuts and tax hikes.

New leader in global growth rates

With growth improving in much of the world, the consensus global GDP estimate for 2015 may have bottomed at 2.7%, up from the anticipated 2.4% in 2014, according to the estimates tracked by Bloomberg. The anticipated pickup in global growth in 2015, has a new leader.

Source: Charles Schwab, Bloomberg data Mar. 20, 2015.

India is expected to take the lead as the world’s fastest growing economy in 2015. China has consistently grown faster than India over the past 10 years, and that margin widened to about three percentage points in the past few years. But China’s growth is expected to continue to moderate to 7.0% and India is expected to experience a surge to 7.4% in 2015. Not a surprise to Emerging Market investors, India has been one of the top performers over the past year, gaining more than 20% in dollar-terms. Pro-growth reforms from the Modi administration may sustain the strong performance. For example, last week saw the first annual budget of the Modi era which focused on infrastructure growth and reduction of the corporate tax rate.

So what?

US economic data has been soft, repeating a trend we’ve seen in recent first quarters. But we believe growth will again bounce back as some of the temporary weights drop off. US stocks should continue to grind generally higher—but with heightened volatility—aided by better data and a still-dovish Federal Reserve. But investors shouldn’t ignore international opportunities. Global growth generally appears to be improving and foreign central banks are largely easing monetary policy, potentially benefitting risk assets.

(c) Charles Schwab