Key Points

- The well-watched (and leading) Housing Market Index jump supports view that housing could be in a rebound.

- Household formations and job growth among 25-34 age bracket both surging.

- Residential investment setting up to be a more important driver of GDP.

Economic data has been mixed-to-weak over the past few months; but some of the housing-related data has perked up and could be a bright spot for the economy in the medium-term. Some recent highlights include single-unit permits, pending and new home sales, mortgage applications, building materials sales, anecdotal strength via the Fed’s Beige Book, and the well-watched Housing Market Index (HMI), put out by the National Association of Home Builders (NAHB). You can see the HMI in the chart below.

HMI Remains Strong

Source: FactSet, as of April 20, 2015.

The April reading of the HMI, at 56, is up four points since March. In addition to the improvement in the headline index, several of the HMI’s sub-components also increased nicely, including: Present Sales, Future Sales, and Traffic. On a regional basis, there was improvement in three out of four regions (with only the Midwest dipping). In fact, the Northeast saw the largest improvement of any region; suggesting that weather was a big reason for the weak first quarter data.

The strength in the HMI is good in and of itself; but it’s also a key leading indicator for housing starts, with about a nine month lead. The chart below (with the lead built in), shows that unless the HMI breads down from here—or the relationship no longer holds—starts should begin behaving much better.

HMI Leads Housing Starts

Source: FactSet, Strategas Research Partners, as of April 20, 2015.

Beige Book reference

The Fed had this to say in its recent Beige Book, which is a gathering of “anecdotal information on current economic conditions” by each Federal Reserve Bank: “Reports from the twelve Federal Reserve Districts indicate that the economy continued to expand across most regions from mid-February through the end of March … Residential real estate activity was steady to improving across most Districts, although there was some slowing in housing starts due to abnormal seasonal patterns owing to the harsh weather.”

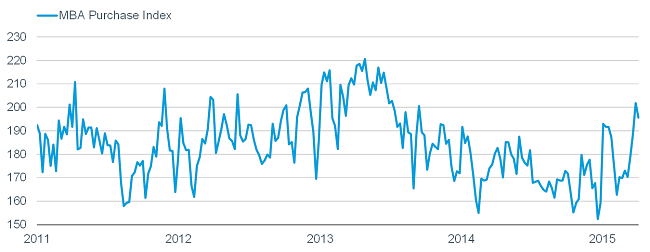

Mortgage apps

Weekly mortgage applications, seen in the chart below, are considered a very timely leading indicator; and notwithstanding the recent slight dip, are showing a surge in home buying so far this year. This is also consistent with a Strategas-reported Zillow survey, which indicated about a million more renters expect to buy a home in 2015 than in 2014.

Mortgage Apps Surge

Source: FactSet, as of April 10, 2015.

Bespoke Investment Group (BIG) studied the Mortgage Bankers Association (MBA) data and found that although they are not a sure-fire predictor of the direction of the housing market given the volatility, they can look at a smoothed trend for guidance. The growth in the purchase index usually leads or is at worst coincident with other housing data, but is released sooner. Assuming that relationship hasn’t changed, “MBA data suggests that housing is getting ready to kick into a much higher gear this year than we’ve seen over the last few years.”

In addition, an impediment to first time home buyers in many metropolitan markets has been lack of existing housing supply for sale; which has driven up prices and crowded out lower income buyers. New home construction is needed to ease the supply issue in many of these markets.

Home sales data—for both new and existing homes—out later this week, will also be a key tell for the housing recovery story.

Household formations surge

Also, notice the massive jump in household formations in the most recent quarter (fourth quarter of 2014) in the chart below. That is the largest surge in over 30 years! Caveat: It could be revised lower. Relative to a year ago, the numbers of households increase by nearly 1.7 million—the most since the third quarter of 2005. This data suggests that more people are leaving the nest to form their own households (regardless of whether it is to buy or rent a home); another boost for additional home construction and the economy more broadly.

Household Formations Rip Higher

Source: Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2015© Ned Davis Research, Inc. All rights reserved.), as of December 31, 2014.

I’ve heard it suggested that the Millennial generation is less interested in owning homes that its predecessor generation(s). But a recent survey from Fannie Mae showed about 90% of young renters are likely to buy a home. And according to the 2013 Demand Institute Housing & Community Survey, about 75% of adults under 30 still view owning a home as an important long-term goal. The Institute’s survey also showed that 24% of Millennials already own their own home; and an additional 60% plan to buy a home in the future. In addition, 87% of home buyers under the age of 33 considered their purchase a good financial investment, according to the National Association of Realtors. The homeownership rate has begun to stabilize for those under the age of 35, and was the only age cohort to turn higher in 2013.

Perhaps the most notable prop under rising household formations is the recent surge in job growth for 25-34 year olds. The level is the highest since 1992.

Younger Cohort Job Growth Surges

Source: Federal Reserve Bank of St. Louis, as of March 31, 2015.

And it’s not just job growth that has improved for this cohort. After reaching an all-time low last year, the relative wages of 25-34 year olds are starting to catch up to that of older workers. That said housing affordability remains extremely high. As such, the weakness in housing demand has been more of a balance sheet issue than a cash flow issue; but higher wages don’t hurt.

Starts and permits disappoint, but…

The data is not universally rosy though. Last month’s Housing Starts and Building Permits reports were ugly, and March’s data were not much better. In fact, looking back to 2000, the past two months are the first time that Housing Starts missed consensus forecasts by more than 100k in back-to-back months.

But even within this data there are glimmers of hope. Both starts and permits for single-family units were stronger than the headline reading and also showed growth. Single-family units generally have a greater economic impact than multi-family units, so the strength is in the “right” place for the economy. And like the regional HMI data showed, both starts and permits in the Northeast saw big gains; suggesting a weather-related rebound.

Looking at the lending side, residential real estate loan growth has been trending higher since late last year, and the three-month moving average is at its highest level in almost two years. Better lending activity should continue to support the HMI.

Impact on economy

Real residential investment—the housing component of gross domestic product (GDP)—increased at a 4.1% quarter-over-quarter annual rate in the fourth quarter of 2014. It was up 2.6% year-over-year; up from -0.7% in the third quarter. Leading indicators for housing point to the possibility that year-over-year growth could move into double-digit territory by the fourth quarter of this year; but we should probably temper those expectations given the reluctance to borrow, still-high home prices, and the possibility of higher mortgage rates. Nonetheless, housing is likely to be a brighter light illuminating the economy this year.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(0415-3199)