Schwab Market Perspective: Heads, Bulls Win; Tails, Bears Lose?

Key Points

-

US stocks have moved into positive territory for the year, despite continued soft economic data and a relatively weak earnings season so far. Investor skepticism seems to be helping support equities in a contrarian sense ; although grinding rather than racing appears to be the current track.

-

While some Fed speakers have noted that a June hike is not off the table, it appears relatively unlikely. They continue to point to the soft economic data as temporary, although it may be going on a little longer than expected.

-

Gains in the Chinese stock market appear to be more of a catch-up than an overshoot (yet), but a correction is still possible. Greece continues to struggle greatly but the broader risks to the Eurozone seem to have dissipated.

The US stock market’s resilience has been notable, given Fed-related uncertainty and dollar-related weak earnings growth; with bears unable to take hold of the market. As most investors know, data can be spun in many different directions, and currently it seems to be spinning modestly in favor of equities. Weak economic data is viewed as pushing back the “launch date” for the Federal Reserve in raising interest rates, while any recent positive data is viewed as economic improvement—both potentially positive for stocks. We’ve even seen stocks react positively to the recent rise in oil prices, as it eases concerns about global deflation and weak growth.

But US stocks have been on a hamster wheel—a lot of movement to get nowhere. This has shifted investors’ behaviors and attitudes. According to Evercore ISI Research Group, investors have pulled $27 billion out of equity funds year-to-date as of April 15, while putting an additional $52 billion into bond funds.

In terms of attitudinal measures of sentiment, notable has been the recent spike in “neutral” respondents to the well-watched sentiment survey put out by the American Association of Individual Investors. Not only do those in the neutral camp outnumber those in either the bullish or bearish camp, they represent nearly 50% of responses—a new cycle high. Ambivalence is the sentiment of the day.

This skepticism can help to put a floor under selloffs in the market as money remains on the sidelines, but it can also help to limit gains as investors are timid about joining any sustained move higher. The result is much as we’ve seen, a grind generally higher, increased volatility, but no real excitement.

Of course, that can change at any time, and very quickly, in either direction. So it’s important to remain vigilant about maintaining a diversified portfolio appropriate for your risk level—not always exciting, but prudent.

Waiting for a rebound

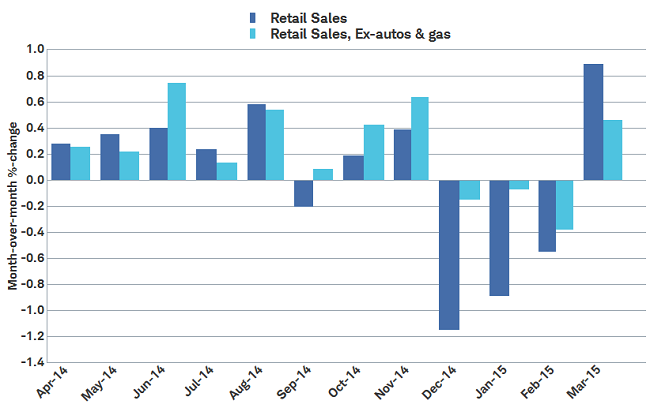

This continued caution seems to be permeating the United States, as consumers aren’t returning to their free spending ways following the financial crisis as quickly as some had hoped. The expected rise in retail spending from lower oil has yet to come to fruition, with consumers choosing to save or pay down debt rather than spend, as had been typical. The March retail sales number showed a 0.5% increase ex-food and energy—positive, but not the jump expected by economists following weak reading in the previous few months.

Tepid retail rebound—so far

Source: FactSet, U.S. Census Bureau. As of Apr. 20, 2015.

We expect a further rebound in retail sales as the weather continues to warm and with job growth still healthy. The leading indicator of initial unemployment claims continues to run below 300,000, while the number of job openings in the latest JOLTS (Job Opening and Labor Turnover Survey) rose to the highest level since 2001. But a somewhat surprising level of prudence remains as the number of Americans without a credit card has risen to 29% in 2014 from 22% in 2008, according to a survey by Gallup and reported by creditcard.com. And debt deleveraging continues, at least at the consumer level.

Consumers continue to pare debt

Source: FactSet, Federal Reserve. As of Apr. 20, 2015.

While probably prudent, a timid consumer likely leads to slower economic growth; and while we don’t think this is a permanent shift, the impact of the financial crisis should not be discounted and this caution could be more secular than cyclical.

Businesses’ confidence has also waned recently, as the National Federation of Independent Businesses (NFIB) reported that its confidence survey fell in March to 95.2 from 98.0; although they attributed at least some of that weakness to weather. Additionally, industrial production fell 0.6% in March, while capacity utilization fell to 78.4%, again attributed largely to utility production weakness due to weather.

We expect these readings will move higher as we progress through the year, especially if housing continues to improve. The National Association of Homebuilders (NAHB) Survey rose to 56 from 52 and household formation has been rising—both potentially positive for housing—while existing home sales rose a solid 6.1% in March. But restraint and caution remains as housing starts only rose 2.0% in March after a sharp drop in February, while building permits were down 5.7%.

Household formation should boost housing

Source: Bloomberg. As of Apr. 20, 2015.

Earnings season is underway, with expectations quite weak at the outset. Although most stocks didn’t pay a large price for lowering those expectations, were rewarded when they beat the low bar set by themselves and the analyst community—frustrating for the bears in the crowd. The consensus for first quarter earnings has improved from nearly -6% year-over-year, to only about -2% today. We do believe if earnings do close the quarter in negative territory, it will be simply an earnings recession; not indicative of an overall economic recession.

The common reasons cited for the weakness have been the stronger dollar leading to reduced foreign demand, the plunge in oil prices (until recently), and weather-related hits. Forward guidance has again been cautious, but the dollar’s gains have slowed, and the weather is warming, which should allow for better performance in coming quarters.

Fed faces a tough road

The Federal Reserve has to take all of these issues into account and attempt to predict the future 12-18 months out as monetary policy typically works with a substantial lag. The Fed’s tone remains dovish, and it seems willing to be patient, despite the removal of that word from its statement. This patience, however, has limits, and there seems to be a strong and growing desire to move off the zero bound for short-term interest rates. Volatility will likely continue as we get closer to that date, but after the first hike is when things get really interesting. At what pace do they raise rates? And how does that relate to how fast the Fed will reduce its balance sheet? Incoming inflation and growth data will undoubtedly play a large part in those decisions, but the urge to move toward normalcy should not be discounted.

China’s stock market doubles

In contrast to the muted gains in the United States, a market that has garnered a lot of attention lately for its strong rally is the Shanghai Composite—mainland China’s stock market, which is largely closed to foreign investors. This index has more than doubled in the past year even as China’s pace of economic growth has slowed.

Looking back over the past 20 years or so, China’s Shanghai Stock Exchange Composite Index has generally moved higher in a wide and volatile range. The recent sharp move to the upside reflects more of a rebound from overly pessimistic conditions accompanying new stimulus (like the further cut to bank loan reserve ratios this week) than a surge to overly optimistic levels.

China’s stock market snapback

Source: Charles Schwab, Bloomberg data as of 4/21/2015.

It is worth noting that over the past 20 years both China’s earnings per share and gross domestic product (GDP) have outstripped the performance of its stock market. A year ago, this left Chinese stocks trading at some of the lowest historical valuations on a price-to-earnings or price-to-GDP basis. As a result, the snapback in stock prices seems to reflect a catch up, rather than a leap ahead, in terms of China’s fundamentals. Nevertheless, some signs of speculation are present and the risk of a correction has increased.

While Greece’s stock market gets cut in half

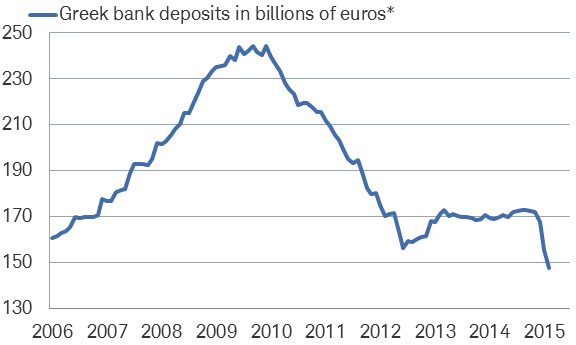

At the other extreme is a market getting a lot attention for its weakness: Greece. Another deadline has come and gone, and Greece has yet to strike a deal with its creditors to release the next tranche of financial aid. The related market turmoil remains largely contained to Greece; where reports that the European Central Bank (ECB) may limit the help it has been providing to keep Greek banks funded pushed down stocks on the Athens Stock Exchange General Index. The level of the index has been nearly cut in half over the past year—with a decline of 49% from March 18, 2014—and has returned to levels not seen since 2012. The ECB has been providing increasing amounts of emergency funds to banks as nervous Greeks have been pulling their euros out of Greek banks; as you can see in the chart of bank deposits below.

Greek depositors increasingly withdrawing money

*deposits non-MFI excluding central bank

Source: Charles Schwab, Bloomberg data as of 4/21/2015.

Although a Greek exit from the Eurozone remains unlikely, and the next tranche of aid may soon be released, interest rates on five-year Greek bonds rose to 20% and seem to be discounting a writedown or default. Whichever the outcome, as long as Greece remains in the Eurozone the risk that exit worries spread to markets in Spain or the UK ahead of the May elections in those countries are likely to remain minimal.

Both China and Greece have stock markets that are making dramatic moves to reflect primarily internal forces. Nevertheless, these forces and markets continue to bear a close watch for their potential to impact other markets.

So what?

The bears can’t seem to grab hold of this market, but that doesn’t mean full-speed ahead for the bulls either. Grinding generally higher with increased volatility seems to be the course for now, but the possibility of a correction still exists. Diversification, discipline and patience is required. International equity exposure should be part of most investors’ portfolios, to a level commiserate with risk tolerance. European risks related to Greece seem to have lessened, while the Chinese stock market doesn’t appear grossly overvalued, although a pullback from the recent run is certainly possible.

(c) Charles Schwab