Plan sponsors are well-versed in the table stakes for retirement plan oversight. They're known as the three F's: fiduciary obligation, fees that are reasonable and fund selections that are in the best interest of participants. But to stand out in a crowded field—and not just squeak by—plan sponsors must design plans that go beyond the basics.

That's why we've developed a new way of thinking about plan success that speaks more directly to what participants need. We call them the three R's of a successful retirement plan—results, reliability and risk. Let's take a look:

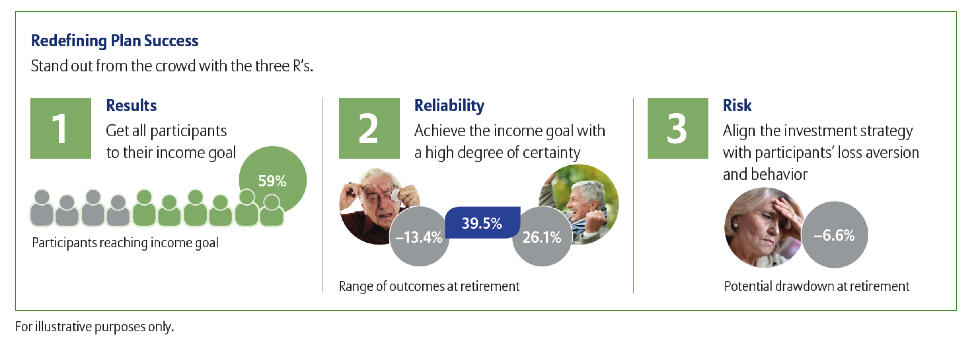

1. Results: Get all participants to their income goal

Having goals is important, but hitting them is what matters most. Plan sponsors should be asking themselves, "What percentage of the participants will achieve their minimum income replacement?" Is it 54% of the population or 80%? It's not about some participants or many participants achieving their goals—it's about all participants achieving their goals.

For their part, many retirement plan providers are offering their participants tools to project the amount of income they will need to retire comfortably. That's good news because it helps set expectations and aims to educate participants on how much money they'll need in retirement. But those projections tend to be all over the map largely because the assumptions and methodology vary widely from one plan administrator to the next. Plus, these forecasting tools spit out a specific dollar figure, which can be misleading to retirement savers.

Still, defined contribution plans do not guarantee a certain level of income in retirement like defined benefit plans, which are now being phased out at many companies. The income replacement target should be a range that is based on a number of factors—not a finite number. (In the December 2014 issue of Dialed In to Retirement, "Taking Aim at the Income-Replacement Bull's-Eye", I highlighted the participant data needed to do the math.)

But for some plans, the goal might not be a good fit for the participants. Choosing the appropriate plan goals can make or break someone's retirement. For example, let's say a participant invested in a 401(k) plan that includes target-date funds managed to achieve the highest average account balance. And the plan provides a projected annual income estimate of $22,000 on the account statement.

However, the actual approximate annual retirement income can range from $13,000 to $36,000, with an average of $22,000. The problem is the range is too wide to give plan participants any sort of comfort that there will be enough income to live off. Essentially, you'd have to significantly adjust your lifestyle if you hit the low end of the range. While the average account balance might be $22,000, the minimum is still almost half the average.

To us, by optimizing the glide path—dynamically shifting allocations over time—and boosting participants' savings rates, fiduciaries can improve the odds of more participants reaching their goals—while minimizing the shortfall for those who don't make it. We call this approach "No participant left behind."

2. Reliability: Achieve the income goal with a high degree of certainty

We have said in the past that the focus of a well-designed retirement plan should be to replace a certain amount of income for its participants once they reach retirement. For example, the goal might be to replace 80% of income—including Social Security—with a certain degree of reliability. Today, the success of a plan should be determined by the ability to get more participants to reach their goals. And that's a direct result of achieving sufficient income with a high degree of certainty. How high? Well, at Allianz Global Investors, we believe at least a 95% probability of achieving the income replacement target for participants is feasible when you have the right approach.

3. Risk: Align the investment strategy with participants' loss aversion and behavior

We all have inherent biases that obscure our judgment and lead us to make poor investment decisions. Loss aversion—a psychological phenomenon marked by weighing losses more heavily than gains—leads investors to undershoot their retirement goals. It's common among retirement-plan participants.

Indeed, when investors become increasingly loss averse, it creates a disparity between what's needed to achieve their goals and the amount of risk they're comfortable with. That gap often translates into an income shortfall for retirees. And not everything can be explained with mathematical models. Monte Carlo simulations don't take into account participants' actual behaviors and tendencies, such as those exhibited in response to the 2008 market collapse. They also fail to account for the fact that many Americans retire unexpectedly—ahead of their target date—due to health issues or a job loss, for example.

Of course investment risk is also a key consideration. Within a target-date fund, for example, there should be sufficient diversification across asset classes with balance between returning-generating assets and defensive assets that either take on less risk near retirement, protect against inflation or have low correlation to stocks and bonds.

Performance must always be evaluated in the context of risk. That could mean looking at risk measures such as Sharpe ratio and standard deviation during the due diligence process. Ultimately, plan sponsors want to protect participants from a steep drawdown at or near retirement, or sequencing risk.

About Dialed In to Retirement

This article originally appeared in Glenn Dial’s Dialed In to Retirement column, which is available as a subscription for financial professionals only. Sign up for thoughtful insights from our US Head of Retirement Strategy on ways to improve outcomes for plan participants, including analysis of emerging retirement trends, portfolio construction ideas, regulatory developments and behavioral finance research Visit us.allianzgi.com to learn more.

Past performance of the markets is no guarantee of future results. The principal value of target date funds is not guaranteed at any time, including the target date. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities. There are no assurances that the strategies outlined will yield positive investment results or success. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Forecasts are inherently limited and should not be relied upon as an indicator of future performance.

©2015 Allianz Global Investors Distributors LLC, 1633 Broadway, New York, NY 10019-7585, us.allianzgi.com

AGI-2015-05-21-12333