Schwab Market Perspective: As the World Turns

Key Points

- Despite many gyrations in the US stock market, little progress has been made this year, although it remains near all-time highs. Investors may be waiting for a catalyst, while international developments are moving toward center stage.

- A rebound from the weak start for the US economy this year has yet to surface, but it remains our base case. The consensus (and our) expectation is that the Fed will remain on hold through the summer and not begin raising rates until at least September. But it’s the subsequent path of rates that matters more than the start point.

- Japan, and the exports from its manufacturing sector, could be one of the bigger beneficiaries from the Trans-Pacific Partnership (TPP) trade deal currently being debated in the US Congress.

Please note: Due to the upcoming holiday the next Schwab Market Perspective will be published on June 12, 2015.

The bund!

In keeping with the greater interconnectedness of global markets and central bank divergences, moves in global markets have driven US markets, volatility and sentiment. The fixed income market has been particularly volatile, with the German bond market—specifically the yield of the 10-year bund—taking center stage.

The bund’s move…

Source: FactSet, Bundesbank. As of May 15, 2015.

… has at least partially influenced US rates.

Source: FactSet, Federal Reserve. As of May 15, 2015.

Greater globalization means money can move internationally relatively easily. The spread between the German bund and the US Treasury—two countries considered fiscally sound—can only get so large, so when one moves, the other is likely to move as well as investors reposition. So what does this mean?

For now, we believe this was a relatively minor move in a short time frame, but doesn’t indicate increased fears of inflation or mean that we are now in for sustainably higher yields. Many countries, including much of Europe, Japan, and the United States, have sub-target and near-zero inflation rates , with no large economy showing signs of immediately-pending inflation pressures. But with the amount of liquidity global central banks are providing, volatility and price dislocations are likely to occur, and investors need to be prepared and appropriately diversified. Read more on the reasons behind the rise in yields in Kathy Jones’ article “Surging Bond Yields: Temporary Correction or New Trend.”

Central banks’ balance sheets have exploded

Source: FactSet, Federal Reserve, Bank of Japan, European Central Bank. Indexed to 100=Jan. 5, 2007. As of May 15, 2015.

Seasonally, we’re entering a period when activity tends to wane as summer vacations ramp up. The June Fed meeting will keep investors engaged through at least the 17th , and the Greek debt drama seems destined to continue. Grinding away seems the most likely course with equity market valuation concerns helping damp down enthusiasm. Also, US economic activity typically slows in the summer; while European activity—already faltering relative to expectations—typically falls off a cliff given the lengthy summer vacations of many Europeans. In fact, the European Central Bank (ECB) announced that it would pull forward some of its QE-related asset purchases to May and June due to the lack of liquidity in July and August. The risk to this is that thinner trading and less experienced traders at the helm could lead to more violent, albeit temporary, moves in the summer.

Still sputtering

The US economic picture has become a bit more troubling. We have yet to seen much of a rebound from the weak first quarter as April retail sales were disappointingly flat; while ex-autos and gas they creeped up a meager 0.2%. Consumers remain cautious, as four out of the last five retail sales readings have been flat or negative. And now oil has rebounded, which puts the possibility of a strong resurgence in consumer spending further in doubt.

Crude bounce could dampen consumer surge hope

Source: FactSet, Dow Jones & Co. As of May 15, 2015.

Not all is downbeat, however, and we still believe economic growth will rebound in the coming months. Initial jobless claims—a leading indicator—continue to trend lower, suggesting the labor market is relatively healthy. Also, The National Federation of Independent Business (NFIB) business confidence survey rose to 96.9 from 95.2, while capital expenditure plans also expanded.

The mixed data continued with industrial production (IP) falling again, while capacity utilization moved further away from the 80 level that typically indicates a robust economy that requires capital expenditures to add capacity. IP has declined for five consecutive months, which has never occurred historically outside of a recession. However, there are a few caveats this time. The overall drop is only about 1%, which is much lower than the typical recession-related drop. In addition, when two of the five negative IP numbers were originally released, they were positive readings, before being revised lower. And finally, the manufacturing side of the US economy has shrunk, so IP is less dominant in our economy than in decades past.

A brighter spot has been within housing; with a renewed boost coming from new home sales, which were up over 20% in April to the highest level since November 2007; while building permits also posted a robust 10.1% gain, both according to the US Census Bureau. Household formations—after a long post-bubble drought—are also rebounding sharply. These readings don’t yet guarantee a trend, but it does provide some hope that the soft patch was really just a temporary occurrence.

Muddy data doesn’t help Fed’s plans

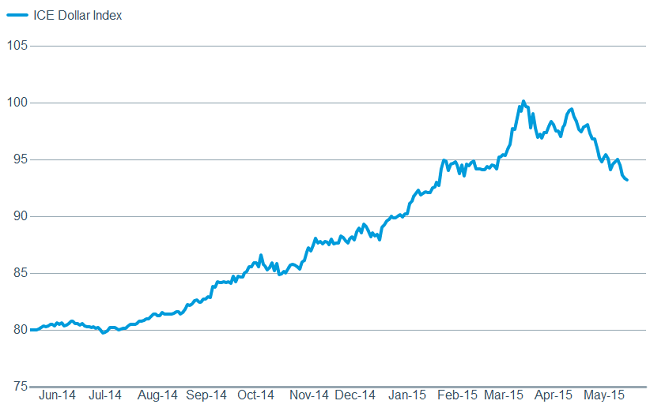

There appears to be a majority of Federal Open Market Committee (FOMC) members who would like to move interest rates off the zero level where they’ve been locked for six-and-a-half years. However, given the soft economic data, some are expressing reluctance to move too soon, while waiting for the data to improve. The FOMC is also more focused than usual on global developments; and the recent mentions of the US dollar/global currency movements has captured the markets’ attention—especially given that the Fed is usually silent on these subjects. A new wrinkle may be the recent reversal in the dollar, which could aid in their desire to raise rates.

Dollar’s reversal could move Fed closer to raising rates

Source: FactSet, Intercontinental Exchange. As of May 15, 2015.

We continue to believe the dollar remains in a bull market; but we’ve been expecting counter-trend moves. A strong dollar is a positive for the US consumption-oriented economy; but moves up that are extremely swift—like we had over the past year—cause short-term dislocations. A reversal toward a more stable dollar would be a welcome change.

There’s still a lot of time between now and September, when we think the Fed is most likely to begin to raise rates, but of course the data could change that view. We continue to expect heightened volatility across many asset classes, which is why we believe investors need to focus on global diversification.

Trade deal a win for Japan

In Washington, we are seeing some relatively rare bipartisan cooperation, with Congress working together in order to further a rather important economic agenda item. Aside from the increasingly routine spectacle over Greece’s debt deliberations, the world has been intently watching the US Congress decide on a trade deal in recent weeks. Trade Promotion Authority (TPA) is a necessary step to passing the Trans-Pacific Partnership (TPP) and other trade deals with limited congressional input. TPA is referred to as “fast track” since it requires Congress to a vote on a trade treaty within 60 days without amendment. Without TPA, trade deals could stall under endless amendments and the lack of a timetable under which to consider them. TPA approval would allow for a vote on the TPP as soon as June or July.

Japan’s Prime Minister Shinzo Abe was in Washington, DC at the end of April in part to promote passage of the TPP since Japan may benefit the most of all the nations involved in the TPP (Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, the United States, and Vietnam). Japan’s economy is struggling to maintain momentum after emerging from recession in 2014. However, the decline in the yen, combined with the TPP, should offer an economic boost. As of the start of this year, when a trade deal with Australia came into effect, Japan has trade agreements with countries amounting to about 20% of exports. The TPP would double that to about 40% due to the inclusion of the United States.

Japan is seeking free trade agreements with many trade partners

Japan’s exports by country as of February 2015

Numbers sum to more than 100% due to rounding.

Source: Charles Schwab, Japan Ministry of Finance data as of 5/16/2015.

While trade agreements can both help and hurt different segments of an economy, Japan is a unique case where the TPP offers little downside. Japan has almost no tariffs on most manufactured products so those businesses would not lose any protection in domestic markets; but the elimination of tariffs by other countries could lead to higher exports for Japanese manufacturers. Japan’s Ministry of Finance reports that autos, machinery, and electronics are Japan’s biggest exports, amounting to more than half of total exports. According to the World Trade Organization (WTO) tariff database, the United States imposes tariffs on Japanese cars (2.5%) and trucks (25%), electrical machinery (2.0%), and televisions (2.8%), among other goods, boosting prices in US markets. The elimination of tariffs would allow Japanese companies to better compete in US markets, potentially boosting sales and profitability.

Japan is also seeking trade deals with China, the European Union, and Korea, among others. A deal with these three would raise the percentage of Japan’s total exports to free trade countries to about 70%. As a result of these deals, Japan’s manufacturing sector could see a revival. This is important since Japan’s widely-watched manufacturing purchasing managers index (PMI) has slumped in recent months to a reading of 50, indicating a stalled manufacturing sector. A return of growth to manufacturing could provide a further boost to Japan’s stock market, which is leading the developed markets this year with the Nikkei 225 Index posting a gain of roughly 14% in US dollar terms as of May 20.

So what?

A market that grinds higher isn’t all bad as it allows time for earnings to catch up to prices; but complacency must be reined in. Sharp movements could and should come as we move closer to a potential Federal Reserve rate hike. We believe the US economy will rebound from the weak soft first quarter, helping to support stocks and a rate hike, but the turn needs to gain traction. Meanwhile, Congressional approval of fast track trade authority could pave the way for improvements in the Japanese recovery.

(c) Charles Schwab