Investing for retirement is about precision. It's a lot like golf: The closer you get to the pin, the more accurate you need to be.

As plan participants near their retirement date, they need to have greater certainty around the preservation of their nest eggs. More specifically, they need a certain level of income to live comfortably when they exit the work force. The wider the range of a plan's expected income, the less certainty retirees will have about their financial security.

Indeed, it's accuracy and timing that matter. The allocation can be controlled, but how the markets perform can't. So turbulent markets, especially near or at retirement, can jeopardize even the savviest investor's life savings. And a downturn in the markets can strike without warning. Think about your golf game: A pinpoint accurate drive and the perfect approach shot can be squandered by a couple of missed putts.

A Sweeter Swing

That's why properly preparing for retirement—for both plan sponsors and their participants—should include consulting a financial advisor. In fact, the Department of Labor formally recognized the benefits of plan participants having access to professional advice in December 2011.

Things like getting the 401(k) plan savings rate right, managing myriad risks—such as down markets, longevity, rising interest rates and inflation—and properly diversifying are just a few of the many advantages of an advisory relationship. It's akin to golfers having a swing coach or a caddie, someone to help keep them out of the rough and away from the bunkers—without taking too many chances.

And keeping emotions at bay and staying grounded too. That's where lessons from behavioral finance are applicable. We all have inherent biases that cloud our judgment and lead us to make poor investment decisions. An astute advisor can help raise awareness of these psychological influences and deploy tactics to offset them.

For example, hyper loss aversion is a condition in which investors place greater emphasis on losses than they do on gains. On paper, a 50% chance of winning $100 or losing $10 looks like a good bet. However, research shows that many retirees offered this choice turned it down. For them, the emotional impact of losing $10 was far too great.

When you apply these lessons to income investing, you would expect the conservative choice to be an annuity because it doesn't carry investment risk. Surprisingly, studies reveal that hyper-loss-averse retirees are actually less likely to buy an annuity. Why? Because people focus more intently on the possibility of losing the money used to purchase the annuity, rather than viewing it as a hedge against longevity risk.

A Softer Landing

In many ways, being "retirement ready" means heading off downside risk. Regardless of market terrain, that income should be there when plan participants retire. Investors need to put "shock absorbers" on their portfolios, so to speak. That means being more conservative, more defensive and sufficiently diversified.

Looking back, history has shown that people tend to overreact and sell when there's market turmoil. But, as we know, a bad allocation decision near retirement can be devastating and make it tough to recoup losses. For people who retire during such a tumultuous period, they may run out of money. If they start withdrawing, say 4%, while markets drop, then they will exacerbate its ill effects. In some cases, those individuals won't be able to retire at a time of their choosing.

This phenomenon leads us to portfolio construction and design. In order to preserve a lifetime of good savings, retirement investors must have the right glide path, that is, a dynamic asset allocation approach that's adjusted over time as market conditions change, and they get closer to retirement. Preserving capital at the right time can make or break plan goals. An emphasis on a higher percentage of defensive asset classes such as short-term bonds, TIPS and dividend-paying stocks can help mitigate risk, or help absorb market shocks.

Going with a more conservative allocation doesn't necessarily mean less income. On the contrary, we've found—using real market results—that the income stream can be higher and more stable when there's less equity exposure.

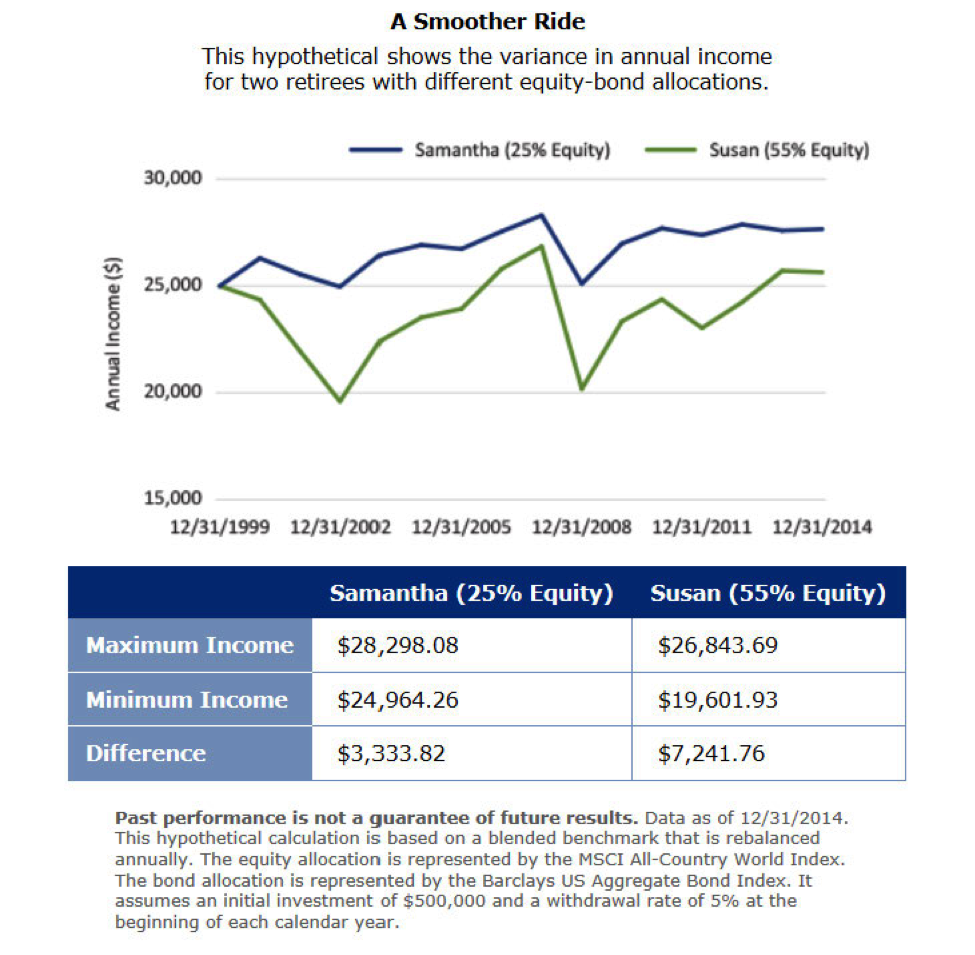

Take Susan, who retired in 1999 with $500,000 in accumulated wealth, and expects to withdraw 5% a year in income, while investing 55% of her 401(k) plan assets in stocks. Now look at Samantha, who retired in the same year and has the same account balance and withdrawal rate, but she has only a 25% equity allocation. If you apply that calculation to recent market conditions, the maximum income potential is higher for Samantha. Plus, her income range is narrower. The chart below demonstrates that participants can achieve a more reliable income stream by reducing their equity exposure near or at retirement.

Ultimately, having more reliable retirement income—narrowing the income range with a higher degree of confidence—means having less equity exposure when it counts. It's not enough to get plan participants on the green. We need them to sink the putt.

About Dialed In to Retirement

This article originally appeared in Glenn Dial’s Dialed In to Retirement column, which is available as a subscription for financial professionals only. Sign up for thoughtful insights from our US Head of Retirement Strategy on ways to improve outcomes for plan participants, including analysis of emerging retirement trends, portfolio construction ideas, regulatory developments and behavioral finance research Visit us.allianzgi.com to learn more.

Past performance of the markets is no guarantee of future results. The principal value of target date funds is not guaranteed at any time, including the target date. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities. There are no assurances that the strategies outlined will yield positive investment results or success. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Forecasts are inherently limited and should not be relied upon as an indicator of future performance.

The Barclays U.S. Aggregate Index is composed of securities from the Barclays Government/Credit Bond Index, Mortgage-Backed Securities Index, and Asset-Backed Securities Index. It is generally considered to be representative of the domestic, investment-grade, fixed-rate, taxable bond market. The MSCI All Country World Index (MSCI ACWI) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. As of May 2010 the MSCI ACWI consisted of 45 country indices comprising 24 developed and 21 emerging market country indices. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

©2015 Allianz Global Investors Distributors LLC, 1633 Broadway, New York, NY 10019-7585, us.allianzgi.com

AGI-2015-06-05-12410