Key Points

- US stocks have managed to nudge their way higher so far this year, but have been in the narrowest range in S&P 500 history. Historically, narrow ranges have typically broken to the upside, but a risk of a correction still exists.

- US economic data has improved since the weak first quarter but to a still-subdued pace, allowing the Fed to “normalize” monetary policy at a measured pace, without yet having to react to inflationary pressures.

- Greece continues to deal with debt deadlines. We don’t know how this will end but the damage to the European economy with a potential default should be relatively minor.

Please note: Due to the upcoming Independence Day holiday, the next Schwab Market Perspective will be published on July 17, 2015.

We aren’t going to use the young lady’s name due to potential royalty requests from her and a family of bears, but the US economy appears to be improving—in a not-too-hot, not-too-cold manner. Depending on your point of view, that could be just right, or disappointingly lukewarm.

Stocks have managed to creep into positive territory for the year, pushed along by somewhat better economic data, continued loose monetary policy by global central banks, and robust merger and acquisition (M&A) activity. According to Evercore ISI Research there have been more than 1000 deals over the past 16 months. M&A activity, however, can be viewed in a couple of ways: Positively, solid balance sheets and good corporate confidence leads businesses to expand, potentially taking some competitors out of the market and improving pricing power. Alternatively, it could also represent companies not finding a lot of new opportunities within their own businesses and being unwilling to invest in capital in order to organically grow. The truth may lie somewhere in the middle.

The middle is where we seem to be stuck from a US market perspective—valuations are neither a screaming buy or sell, sentiment is relatively neutral, the Fed is in limbo, and economic data is lukewarm. Beige would be the color that seems to best describe the current environment. Even the potential Greek debt crisis has been going on so long that it seems to eliciting smaller reactions from investors. We continue to believe that stocks will manage to grind higher over the next several months, with some bumps along the way. And the possibility of a correction still certainly exists; which although unpleasant, could help to break the market out of its “beige” phase.

Economic data better…but not too much

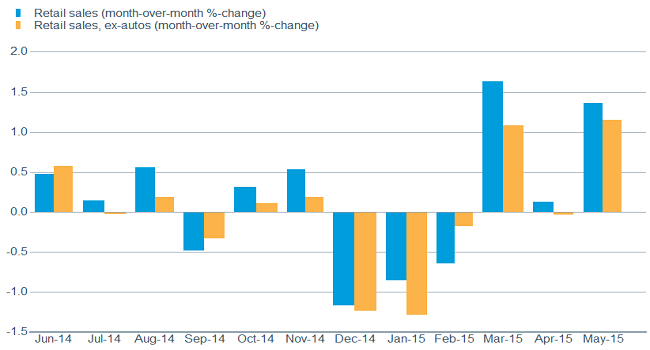

The economy is continuing to rebound after the weak first quarter, but the second quarter is no barn-burner But the US consumer may be coming out of its shell, highlighted by retail sales rebounding in May after a string of weak readings.

Encouraging retail sales bounce

Source: FactSet, U.S. Census Bureau. As of June 22, 2015.

There’s hope for a continued acceleration. Even with the recent rebound, energy prices are substantially lower than they were last summer, unemployment is down, interest rates remain low, and wages are starting to rise—all supports for an improving consumer. And housing is starting to pick up steam, with the National Association of Homebuilders (NAHB) Index rising to 59, while building permits—a gauge of future activity—rose 11.8%. However, housing starts fell 11.1%, although that followed two strong months prior and reflected a sharp weather-related drop in multi-family starts. Meanwhile, existing home sales rose 5.1%, while new home sales gained 2.2%. Pent-up demand is likely kicking in, as the home ownership rate was only 63.7% in the first quarter as reported by the Commerce Department. That was the lowest rate since 1989; but household formations have picked up, rising by 1.5 million year-over-year in the first quarter, driven by a surge in job growth for the 25-34 year-old cohort.

Unfortunately, the manufacturing sector appears to still be struggling, potentially hampered by the strong dollar, although the sharp rise has now stabilized. But until capacity utilization moves back above 80%, capital spending is likely to remain subdued.

Dollar’s recent rise negatively impacted US manufacturing

Source: FactSet, Intercontinental Exchange. As of June 22, 2015.

The Empire Manufacturing Index fell to -2.00 in June, although that was offset by a Philadelphia Fed Survey reading of 15.2, up nicely from 6.7 in May; while Markit’s preliminary manufacturing PMI fell to 53.4 from 54.0. Also, industrial production surprising fell 0.2% in May, while April was revised lower. Perhaps even more disappointing was capacity utilization falling to 78.1%, retreating from the aforementioned and critical 80 mark.

Capacity utilization reverses course

Source: FactSet, Federal Reserve. As of June 22, 2015.

We believe manufacturing will improve in the coming months, helped by a more stable dollar and improving global economic growth, but caution seems likely to continue in businesses and consumers for the foreseeable future.

Fed sending up flares

The Federal Reserve has taken great pains to attempt to prepare investors for a hike in interest rates at some point this year. The Fed clearly doesn’t want to disrupt financial markets through its heightened transparency. September seems to be the most likely “lift off” point; but more importantly, unless inflation unexpectedly accelerates in the near term, the Fed has made it clear it plans to move slowly toward a more normal policy stance. While this doesn’t mean there won’t be some hiccups along the way, it could mean more dampened volatility than would otherwise be the case. And, history shows that the stock market performs substantially better during a slow tightening cycle than a fast one.

Greece’s default option

Volatility has already been seen from the ups and downs of the Greek debt crisis. Many deadlines have come and gone, but Greece is now running out of cash and has so far been unwilling to adopt reforms that would give it more funds from its creditors. A last minute deal may be struck, or a default may be imminent.

A last minute “kick the can” deal would be typical of Eurozone negotiations in the past. A compromise involving higher taxes and reforms to pensions may allow for the delayed release of a limited amount of bailout funds to cover debt payments, wages, and pensions for a few more months. This would buy time and drag out broader discussions over the second half of the year. Alternatively, a default by Greece would by no means be unprecedented. Greece has spent 46% of the time in default since its independence from the Ottoman Empire in 1829 at varying levels of debt-to-GDP, according to data from the International Monetary Fund and Eurostat.

Greece has spent nearly half its history in default on its debt

What may another Greek default mean for investors in global stock markets? Perhaps not that much. Here are five reasons why a potential Greek default may not be a major market event:

- It’s been five years since global growth was as strong and balanced as it appears to be at the midway point of 2015 with all of the world’s major economies growing. That means the global economy may be more resilient to shocks, such as a Greek default.

- The risk of a financial contagion has been greatly diminished from the threat posed a few years ago. This has been a slow-motion and widely watched move toward insolvency since 2008, but in particular since 2011. In that time, over 75% of Greece’s debt has been moved to the books of government institutions and is no longer held by highly leveraged banks that could cause a financial crisis, or a hedge fund that could cause a market failure.

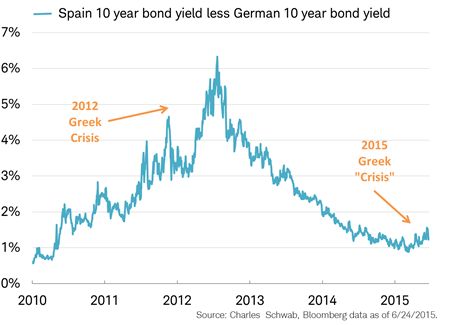

- The risk of a spreading panic in Europe is likely contained in that the European Central Bank (ECB) stands ready to buy the debt and recycle the bank deposits of member nations. Evidence that this is working can be seen in Spain, a country which is often lumped in with Europe’s troubled peripheral nations. The Spanish 10-year bond yield relative to Germany’s peaked this year around 1.6% (up from the low of about 0.9%); but that’s way below the 6.5% of July 2012 the last time we had a real Greek crisis.

Greek crisis contagion risk: 2012 versus 2015

- The Eurozone banking system outside of Greece now has more Greek deposits than loan exposure, per data from the ECB and Bank for International Settlements. Greeks have been moving their euro-denominated bank deposits out of Greek banks to those based in other Eurozone member nations such as Germany. Actual loans to Greeks by non-Greeks outside of governmental holdings are less than half that the amount of deposits thanks to five years of write downs and little-to-no new lending.

- A default and the cut off of central bank liquidity does not automatically mean a “Grexit,” or Greek exit from the euro. Opinion polls conducted by Greek newspapers reflect an overwhelming majority of Greeks desire to remain in the Eurozone. Since the treaties do not provide for an exit from the euro, it is possible euros would still circulate and financial services would be provided by foreign banks and the Greek government would issue IOUs in euros. This could happen even if the Greek government was in default, all Greek banks were excluded from ECB operations and facilities, and Greek bank deposits were frozen.

The potential default and related withdrawal of ECB support for Greek banks would be painful for Greece and ultimately may lead to elections and a new government. But, the efforts by policy makers over the years have served more effectively to isolate rather than to resolve Greece’s problems.

So what?

Despite the narrow range for US stocks this year, things can change quickly. We believe volatility will pick up over the next several months as we head toward the Fed’s initial rate hike. Across the pond, the best we may be able to hope for with regard to Greece is another “kick-the-can” solution. But any potential damage should be relatively contained due to the work done in the Eurozone over the past five years.

(c) Charles Schwab