Schwab Market Perspective: Slow Summer?!

Key Points

- The typical summer slumber in the markets has been jolted by international turmoil. When the smoke clears, we believe the long-term damage will be minimal and we think a grind higher in US stocks will continue.

- While much action has been overseas, the US economy has continued along its tepid growth path. Global turmoil—notably in Greece and China—have yet to channel into either the US markets or economy; but they will likely continue to influence investor sentiment as well as the Fed’s decision about when to raise interest rates.

- Greece made a debt deal with European leaders which averts a near-term exit from the Eurozone, but Greece’s economic crisis will persist. China’s onshore and offshore markets have been volatile and government manipulation has the potential to be counter-productive; while the Iranian nuclear deal could serve to keep a near-term lid on oil prices.

Summer is supposed to be a time of slow trading, light news, and an opportunity for vacations. But the past several weeks have been anything but slow. Greece—a country representing 0.38% of the world economy based on gross domestic product (GDP), has dominated attention; China’s recent stock market plunge also dented sentiment among US investors. It’s meant the “running to stand still” characteristic of this year’s first half is persistent. In fact, the first half of the year saw the S&P 500 trade in its narrowest range in history. For what it’s worth, historically, tight ranges in the first half have typically broken out to the upside in the second half.

While unnerving, we don’t see a long-term impact from either Greece or China on the US economy or stock market; barring a significant deterioration in growth in China. In fact, we could see a calmer phase for the market this summer, before ramping up again in the fall as investors contemplate the possibility of a Fed rate hike. We believe the relative resilience shown by the US stock market during this time of heightened uncertainty serves yet again to remind investors of the perceived relative safe-haven nature of the US market. But the turmoil has impacted investor sentiment—dropping recently as seen in the Ned Davis Research Crowd Sentiment Poll; which, as a contrary indicator could bode well for stocks. Additional evidence of continued investor skepticism, according to Evercore ISI Research, are fund flows year-to-date that show a net $70 billion has come out of equities, with $77 billion being added to bond funds—leading us to believe there are still good opportunities for stocks to rise in the coming months.

In other news…

Relatively speaking, the US front has been relatively quiet, but it’s important not to lose the forest for the trees. Second quarter earnings season is in high gear, with expectations for modest gains year-over-year, excluding energy, once the season is complete. As usual, focus is on the future—with special emphasis likely on any commentary related to the Greece and China impacts as well as the effect on results of the dollar’s rise.

These expected modest earnings results fit with the economic picture that continues to develop—slow but relatively steady. Both Markit purchasing managers indexes (PMIs)—manufacturing and services—fell in June, but both remain in territory depicting expansion, albeit without acceleration. Also creating somewhat mixed messages has been the recent drop in commodity prices. Falling prices for commodities can mean lower costs for both businesses and consumers, but can also reflect economic concerns, in this case likely emanating from China.

Commodity fall has mixed message

Source: S&P Dow Jones. As of July 10, 2015.

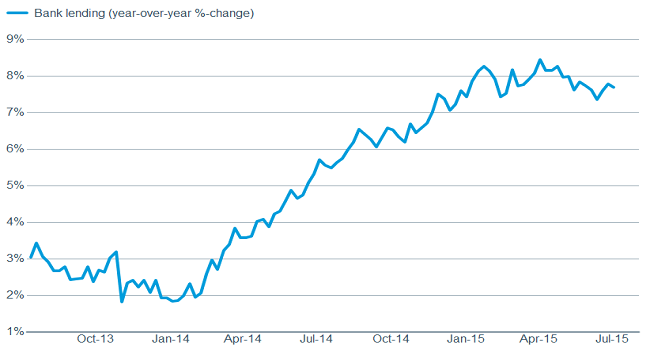

But corporate confidence seems to hanging in there as indicated by the surveys referenced above, as well as the rise in bank loans we’ve seen. Companies overly worried about future demand likely wouldn’t be anxious to add to debt in order to finance operations, but instead would be looking to cut back on such activity. The recent drop in small business optimism measured by the National Federation of Independent Business (NFIB) is disappointing but we believe it’s more of a dip than a trend.

Rise in banks loans a positive indicator

Source: FactSet, Federal Reserve. As of July 10, 2015.

Companies keep adding to payrolls, further indicating their confidence and helping bolster the consumer class. June’s jobs report showed that 223,000 jobs were added and the unemployment rate fell to 5.3%. But the details were less encouraging given that the drop in the unemployment rate was a function of a fall in the labor force participation rate (at its lowest level since 1977); while the previous two months’ payroll gains were revised lower by 60,000.

Potential workers still not engaging despite fall in unemployment

Source: FactSet, U.S. Dept. of Labor. As of July 10, 2015.

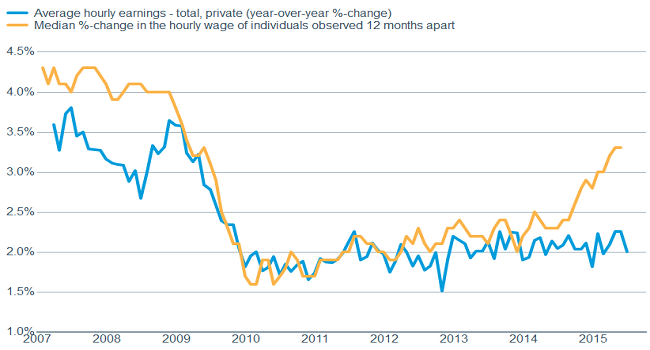

Declining labor force participation remains a point of uncertainty. Demographics, skill mismatches, lack of wage growth, and a rise in the number of people getting government benefits are all likely contributors. But whether it can be reversed, thereby adding more productive workers into the economy, is still in question. Equally disappointing were average hourly earnings—surprisingly unchanged month-over-month in June, and up only 2.0% year-over-year. This remains a bone of contention and a focus of the Fed’s, especially given the low level of unemployment seen. We continue to believe upward pressure on wages is beginning to take hold and this reading will be seen more as an anomaly. With thanks to Cornerstone Macro Research, we were alerted to an Atlanta Fed survey that has had a pretty good record of forecasting wage gains, and as you can see below, wages have some catching up to do if the historical pattern is going to hold.

Wages should be on the rise—based on history

Source: FactSet, U.S. Dept. of Labor, Federal Reserve Bank of Atlanta. As of July 10, 2015.

Fed outlook becomes murkier, government intervention has consequences

Given the above, combined with the international turmoil, the timing of the Fed’s first rate hike is a bit less clear. The low labor force participation rate and tepid wage growth remain on the Fed’s radar screen; so too are global events and the rise in the dollar. This argues for holding rates where they are for longer—which has been advocated by several members. Conversely, it seems the desire to begin the normalization process is strong among a majority of members, including Chairwoman Janet Yellen. Most Fed members seem to recognize that there are burgeoning risks to holding down interest rates at unprecedented levels. We still believe September is a probable jumping off point, but the odds have probably been reduced, and the “lower for longer” scenario we’ve been talking about seems firmly in place.

A deal in Greece

After lengthy and often bitter negotiations, Greece and its creditors reached an agreement on a process for Greece to remain in the Eurozone and receive needed funds. Bridge financing is being provided to make the 3.5 billion euro payment to the European Central Bank (ECB) due on July 20, and meet other needs before the new funds become available.

In Greece, political pressures against further austerity are likely to mount, and restoring growth in Greece remains a major challenge not yet addressed. An exit from the Eurozone remains possible for Greece in the coming quarters if political pressure leads to a failure to implement the required reforms. However, the markets have recognized that the prospects for Greece are separate from the rest of the Eurozone thanks to the isolation of Greece’s debt, and the ability of the ECB to buy the debt and recycle the bank deposits of member nations. This is evident in the relatively modest moves in interbank lending rates, sovereign bond spreads, and European stock prices in recent weeks. While Greece will remain in the news, it is likely to fade as a major driver of market movements.

A deal with Iran

This week a nuclear deal between Iran and the United States, France, China, Germany, United Kingdom, and Russia was announced. Under this agreement, Iran will limit its nuclear program and various sanctions will be lifted. Even if the agreement be rejected by the US Congress, other nations are likely to ratify the agreement.

The timeline of the various steps required to reach relief from sanctions suggests that Iranian oil flows will begin to rise next year as production likely increases gradually. Further supply is likely to keep pace with demand growth, leaving inventories high and keeping a lid on oil prices.

China is dealing with a bear market

China has two different stock markets: those shares that trade in Hong Kong (H shares) and others that trade in mainland China on the Shanghai and Shenzhen exchanges (A shares). After soaring over the past year, A shares plunged more than 30% from mid-June to early-July as Chinese policymakers implemented new margin rules. As liquidity dried up in the mainland market, selling spilled over to Hong Kong market. For further insights see China's Stock Plunge – What You Need to Know.

The stock market plunge does not seem to have affected key measures of financial stress in China: bank bond yield spreads have been stable, the short term money market is not indicating any problems with liquidity, and the currency has been steady. Economic data has been stabilizing as evidenced by second quarter GDP growth, the manufacturing PMIs, and property prices. However, the moves by China’s policymakers to halt the stock market decline may undermine longer term pro-market reform initiatives and may result in weaker foreign investment and less entrepreneurship in China. We will continue to monitor key measures of financial stress and economic growth.

So what?

Markets will likely settle down into a more traditional summer mode in the coming month as some of the immediate international pressure fades. But action could ramp back up as we get closer to a potential Fed rate hike. Global growth is slowing modestly and we will be watching to see whether this is the start of a trend and how big of an impact it may have on the US economy. We continue to see a grind higher in US stocks, but with the potential for more volatility and a pullback.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

Ned Davis Research (NDR) Crowd Sentiment Poll® is a sentiment indicator designed to highlight short-term swings in investor psychology. It combines a number of individual indicators in order to represent the psychology of a broad array of investors to identify trading extremes.

The S&P GSCI (formerly the Goldman Sachs Commodity Index) serves as a benchmark for investment in the commodity markets and as a measure of commodity performance over time.

Markit Manufacturing Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Services Purchasing Managers Index (PMI) released by Markit Economics captures business conditions in the services sector.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0715-4939)