Schwab Market Perspective: The Calm Between the Storms

Key Points

- Stock market action has calmed down, settling into a more typical summer pattern. But action is likely to heat up again as we get closer to the initial interest rate increase. We believe the bull market is in tact but volatility is likely to increase.

- Earnings have been in focus and results largely bested expectations that were yet again set too low. Forward-looking guidance remains cautiously optimistic, reflecting an economy that is growing, but at a tepid pace.

- Fallout from the Greek debt crisis appears fairly limited, with growth improving in Europe. Meanwhile, volatility in China’s equity markets persists, but its economy appears to be stabilizing.

Peak earnings season is behind us, Greece is not in imminent danger of exiting the euro, Europeans have headed out on vacation and the US Congress won’t be far behind. After a volatile start, the US market appears to be settling into a more typical summer pattern—for now.

Calming Down—For Now

Source: FactSet, CBOE. As of July 24, 2015.

Stocks have maintained their tight trading range, with the modest selling seen through the first part of July largely made up. The range so far this year remains the narrowest in history; which is why we’ve been referring to it as a running-to-stand-still market. Investor sentiment has returned to a more neutral level as per the Ned Davis Research Daily Sentiment Composite. There is some notable technical weakness; with very narrow breadth suggesting the market’s internals are weaker than the averages suggest. The possibility of a decent-sized pullback should not be discounted as the market gears up for a possible Federal Reserve rate hike in the fall; Presidential campaigning ramps up; and Europe gets back to work, having really not fully solved the debt crisis in Greece.

Earnings take center stage, but US economy still chugging higher

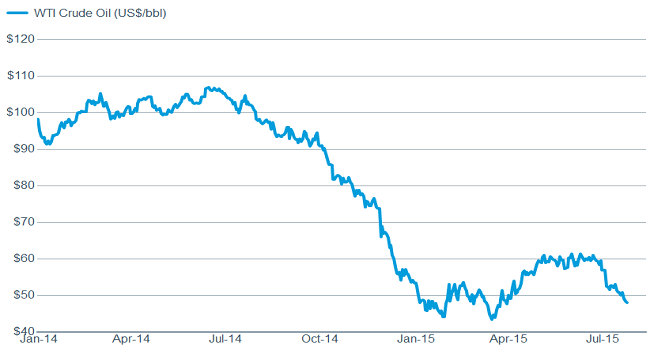

The past few weeks have seen corporate results for the second quarter take center stage. Comparing the results to expectations has become a bit of an inside joke as companies try to manage expectations lower, in order beat them when the moment of truth comes. Companies have generally hurdled the lower bar and are relatively upbeat on the future. Concerns about the stronger dollar and still relatively tepid demand have been featured in much of the forward guidance; but overall the earnings picture appears relatively solid. One notably weak sector is energy, given the renewed plunge in oil prices. And the consternation has extended to other areas of the commodities complex; with weak global growth and China’s slowdown reinforcing our long-held view that the commodity “super cycle” definitively ended in 2011.

Oil resumes its fall

Source: FactSet, Dow Jones & Co. As of July 24, 2015.

The weakness in the energy sector notwithstanding, lower oil and other commodity prices should help the American consumer—allowing them to spend less on "essentials." And consumers may be showing their increasing confidence as the housing market has begun firing on most cylinders. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index rose in July to its highest level since November 2005, while existing home sales reached their highest level in over eight years. Meanwhile, the more leading housing indicators were also strong, with both starts and building permits improving.

Housing looking up

Source: FactSet, U.S. Census Bureau, Nat'l Assoc. of Realtors. As of July 24, 2015.

Although housing’s contribution to gross domestic product (GDP) is nowhere near its bubble peak, it remains an important growth and confidence driver. The NAHB recently released a study estimating the economic impact of homes being built in a “typical local area.” They estimate that the building of 100 single-family homes in a typical local area provides a one-year impact of close to $29 million in local income, $3.6 million in taxes and other government revenue, and almost 400 jobs.

And better housing data fits with the economic trend we’ve seen recently. Evercore ISI Research estimates that since mid-May, 67% of the cyclical economic indicators have been positive; compared to only 41% in the first four months of the year. So while not robust, economic growth is trending in the right direction, which should help to support the continuation of the bull market in stocks.

Fed debate continues

The recent improvement in economic data, which included the lowest initial jobless claims reading since 1973, gives support to those on the Fed that want to begin normalizing monetary policy. The Fed’s meeting this past week had little new information and all eyes are now on the September meeting, when we believe the Fed could raise rates for the first time since 2006. But with little inflationary pressure, the Fed will likely move very slowly—a support for the stock market. Although volatility may increase heading toward the initial hike, history has shown that stocks perform much better in the year following slow tightening cycles than fast cycles.

No contagion in Europe

The Fed made no specific mention of European events in its most recent meeting; and despite Greece’s dilemma in recent months having the potential to weigh on economic activity, growth in the Eurozone economy and profits is accelerating.

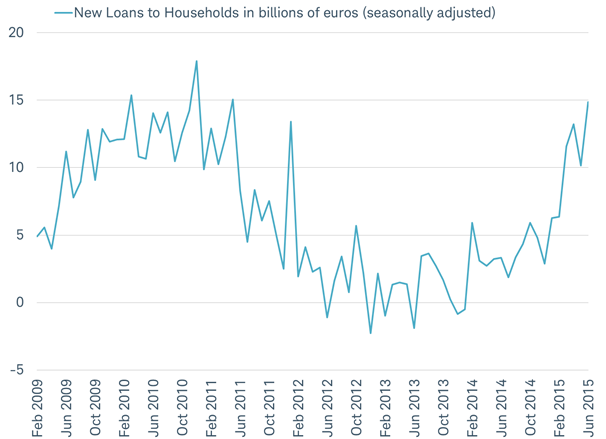

The latest data reports confirm this trend. The German IFO survey rebounded in July according to the European Central Bank (ECB). Indicating improving confidence and willingness to spend, bank lending to households rose again in June, marking the strongest growth in lending in over four years. In addition, Eurozone bank lending to businesses rose in June, following three consecutive months of contraction; supported by further easing of lending conditions reported in the July euro area bank lending survey from the ECB.

Borrowing is on the rebound in Europe

Source: Charles Schwab, European Central Bank data as of 7/29/2015.

The apparent lack of economic or financial contagion extending from the Greek debt crisis extends to political risk as well. Spain’s upstart left-wing political party, often likened to Greece’s ruling SYRIZA party, saw polling results tumble in July. After leading in the polls earlier this year, July polling results show support at less than half of the 30% seen back in January; widely trailing the mainstream parties.

China saw stable growth in second quarter

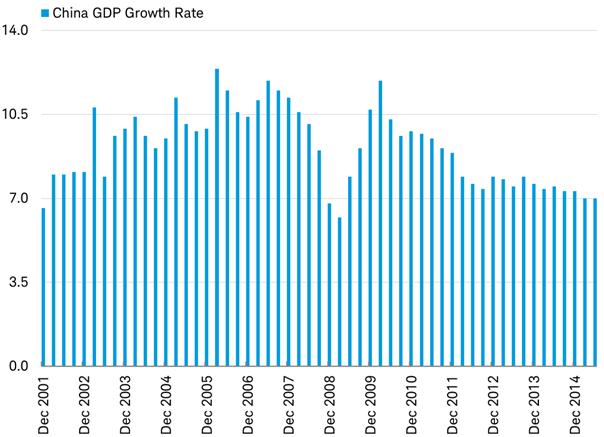

China’s National Bureau of Statistics reported that GDP was 7% higher than a year ago in the second quarter—the same growth rate as in the first quarter. Despite the ongoing decline in commodity prices and the drop in the mainland (A shares) Chinese stock market, the modest improvement in the monthly economic indicators suggests growth may be stabilizing.

China’s GDP growth rate remained at 7% in the second quarter

Source: Charles Schwab, Bloomberg data as of 7/29/2015.

As in Europe, the latest data highlight the improvement. Industrial production rose to 6.8% from 6.1% in June; the year-over-year pace of retail sales accelerated for a second month in June to 10.6%; and exports rose on a year-over-year basis in June after three months of declines. Many measures of Chinese economic growth which become popular in the mid-2000s, measure the “old China,” when manufacturing was the dominant sector of the economy, and not the “new China” increasingly driven by services and consumer spending which are reporting rapid growth.

So what?

The US stock market continues to trade in a very narrow range, with trading volumes slowing down into the summer vacation season. We expect the break out of this trading range to ultimately be higher, but given the market’s recent technical deterioration, a correction is possible. Remain globally diversified and patient, but limit risk-taking in the near term. The European economy appears to be improving and stocks look attractive to us there; while the Chinese economy is having a bumpy transition toward a more service-orientation.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX) is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days.

Davis Research (NDR) Daily Trading Sentiment Ned Composite® shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

The National Association of Homebuilders (NAHB) – Wells Fargo Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to measure homebuilder sentiment in the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. It is a weighted average of separate diffusion indices for these three key single-family series.

(0715-5160)