Doing what's necessary isn't always easy, especially when it involves taking risks. And when it comes to investing for retirement, we're hard-wired to avoid doing things that might hurt us, even if the perceived benefits are far greater than the potential pitfalls.

The conventional approach to asset allocation in target-date funds has long been rooted in risk and return. That is, it's all about the pursuit of what Harry Markowitz called the efficient frontier. And, for a while, that was a pretty sound foundation on which to lay your nest egg. But that model is now evolving, as we begin to better understand the impact of behavioral biases on retirement portfolios.

For example, loss aversion—a psychological phenomenon marked by weighing losses more heavily than gains—leads investors to undershoot their retirement goals. It's a pervasive condition among retirement-plan participants. When investors become increasingly loss averse, it can create a gap between what's necessary to achieve their goals and the amount of risk they're comfortable with. That gap often translates into an income shortfall for retirees.

Essentially, it's math versus human emotion. Put another way, it's what works on paper versus real-world behavior. That's the next frontier for how we look at glide paths—the behavioral aspect. And behavioral finance research reveals that as people move closer to retirement, they become hyper loss averse.

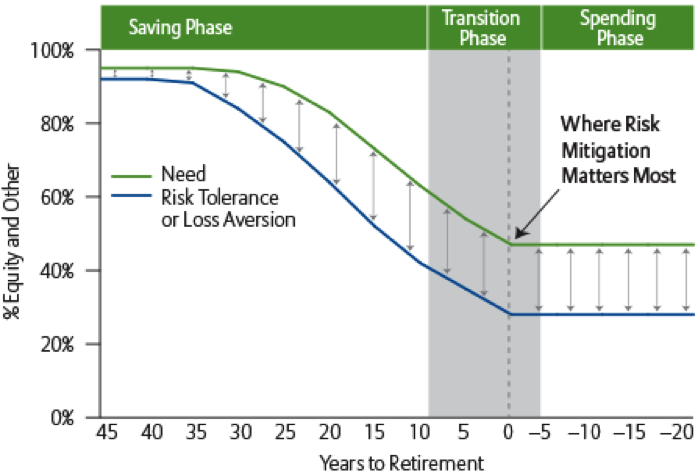

Bridging the Gap

Loss aversion creates a disparity between the glide

path that’s necessary to hit plan goals and the level

of risk participants are comfortable with—a gap

that often leads to an income shortfall.

The graph is for illustrative purposes only.

In 2008, most plan participants didn't take their money out of their target-date funds as the financial markets collapsed. However, the people that were closest to retirement—60-year olds and 65-year olds—did take their money out, locking in those losses. By selling out, they exacerbated the fallout from the financial crisis. That real-world experience is proof that we as an industry have to do a better job of educating plan participants—and plan sponsors—on savings best practices, improving plan design and demonstrating the benefits of a hands-on approach to risk management.

At Allianz Global Investors, we've found that there are three ways plan sponsors can close this retirement risk gap and, ultimately, increase their participants' chances of nailing their retirement income goals:

1. Boost savings rates

It starts with encouraging good savings behavior. Automatic enrollment in 401(k) plans—an opt-out model that defaults participants into the plan—has proven to push participation rates higher. Yet only half of Fortune 100 companies automatically enrolled employees in 401(k) plans in 2013, according to Towers Watson.1 Auto-escalation, or automatically stepping up contributions, is another way to bring more participants into the fold. Even as little as a 1% annual increase can make a big difference for retirement savers. Establishing a corporate match for employee contributions is another way to improve savings rates.

With a few changes to plan design, sponsors can get higher participation levels without incurring many additional costs. Indeed, a recent study conducted by the Urban Institute found that given the average wage, participation, and match rates of plans it analyzed, lowering the match rate by O.38% led to savings of roughly 7 cents per hour of labor. This offsets the 6.5 cents per hour in additional costs from higher participation rates.2

2. Work longer

Among employees, the prospect of working past the age of 65 is typically not met with great enthusiasm. And, for many participants, it may not be a viable option even if it's necessary. Some fields, such as construction or fitness, require younger, more able-bodied workers. Other disciplines come with a lot of stress, and there are a lot of folks who may not have the stamina for that daily grind anymore.

For the employer, keeping older employees around is costly because they tend to earn more than their younger, less experienced counterparts. Plus, it keeps the next generation from rising through the ranks and risks losing up-and-coming talent to free agency.

3. Actively manage risk

Most plan investments, including target-date funds, are managed with an eye toward getting the most return for the amount of risk taken. What we've uncovered is that many participants just can't stomach the risk that's involved.

That's where professional money managers come into play. Putting a dynamic risk-mitigation strategy in place has the potential to preserve most of that upside return that participants need to actually hit their retirement goals, while still minimizing the downside risk. And depending on market conditions, allocations can be raised and lowered, and risk budgets can be adjusted along the way.

For a plan participant, especially one that’s nearing retirement, downside protection is paramount. If plan sponsors can provide a buffer in turbulent markets, then participants are going to stick with the program. That means they increase their odds of making it to retirement with sufficient and reliable income—and avoid falling into the gap.

Glenn Dial is Head of Retirement Strategy in the US with Allianz Global Investors, which he joined in 2011. He has 23 years of defined contribution experience. Mr. Dial is a co-inventor of the method and system for evaluating target-date funds, and is also credited with developing the target-date fund category system known as “to vs. through.”

Subscribe Today

Dialed In to Retirement is available as a subscription for financial professionals only. New issues will be delivered via email every month. Your email address must be in our records for your subscription to take effect.

Past performance of the markets is no guarantee of future results. The principal value of the target date funds is not guaranteed at any time, including the target date. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities. The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York, NY 10019-7585, us.allianzgi.com, 1-800-926-4456.

AGI-2015-08-10-13006

1 “Cost of 401(K) Auto-Enrollment Negligible”, Benefits Pro and Towers Watson, March 4, 2015

2 “Researchers Find Little Cost Difference from Auto-Enrollment”, Plan Adviser, March 2, 2015