Are the Bulls Regaining Their Footing?

Key Points

- Stocks have moved off of their correction lows despite continued global growth concerns and Fed uncertainty. We think most of the damage has been done in price ; but more time (and volatility) may be needed before the bottoming process ends.

- The Federal Reserve punted on raising rates and took pains to indicate their continued dovishness and preference to raise rates slowly in the future. The continued uncertainty will likely contribute to elevated volatility in the coming months.

- The plunge in commodity prices should prove to be a net benefit to the global economy, despite some pockets of weakness for commodity-exposed sectors and industries.

The US equity market has started the recovery process from the correction which began last month. But we don’t believe stocks are off to the races, as there are still plenty of potential speed bumps along the road. Valuations have improved somewhat, although not to the point that equities should be considered cheap; monetary policy remains accommodative in the United States, and highly-stimulative in Europe, China and Japan; and the US economy continues to grow at a steady pace. But the volatility associated with interest rate uncertainty is likely to persist.

As mentioned, the ride won’t likely be a smooth one so investors need to be prepared for more ups and downs and should endeavor not to be distracted from established investing plan. There are still economic growth concerns in China, while there are also upcoming European elections that could unnerve investors at least temporarily. As such, the volatility we expect to persist, is global in nature.

US Economy Still Supportive of Stocks

Underlying the view that the bull market is not over is the continued growth in the US economy. The manufacturing sector, as well as multi-nationals, have been hit double-barreled by China’s growth slowdown and the dollar’s strength. The manufacturing sector is only about 12% of the US economy though; with the services side representing the other 88%. And here the picture is much brighter. Associated with that strength is the improvement in housing—which is increasing its weight in the economy—and job growth, which continues to hum.

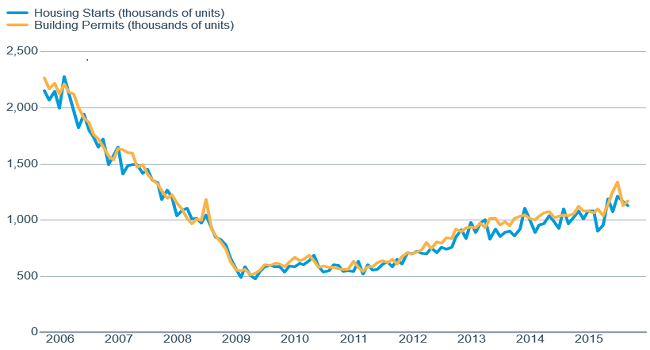

The National Association of Homebuilders’ (NAHB) recent survey showed sentiment moved up to 62, which is a 10-year high. And while housing starts fell modestly in August, partly influenced by a tax-related incentive surge in the previous month, they are up 25,000 from the average seen last year. And building permits, which are one of the key leading indicators for the economy, and rose 3.5% in August and are up nearly 120,000 relative to 2014. And despite the prospect of higher short-term rates by the Federal Reserve, mortgage rates remain near historically low levels, which will continue to support housing.

Housing continues to gradually improve

Source: FactSet, U.S. Census Bureau. As of Sept. 17, 2015.

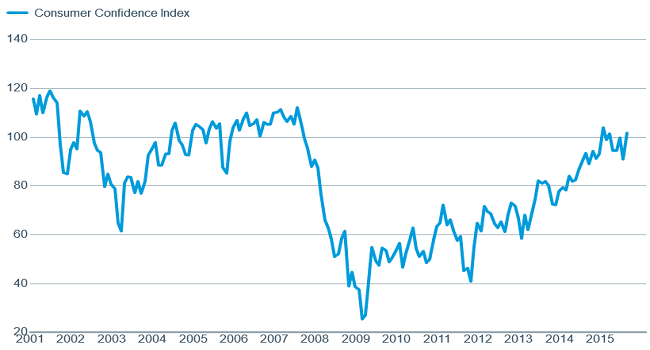

As we’ve mentioned, housing’s actual economic impact has lessened substantially since the peak of the housing market. But we do believe housing has a noticeable impact on the psyche of the American consumer, which is also improving as the Conference Board reported their recent consumer confidence survey moved close to its highest level since the great recession.

Which appears to be helping consumer confidence

Source: FactSet, Conference Board. As of Sept. 17, 2015.

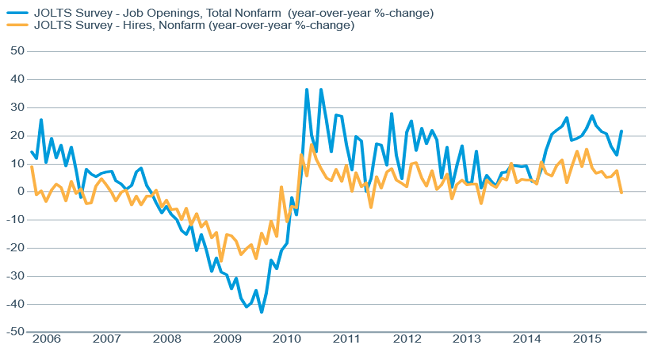

Also contributing to the better outlook among consumers is the continued improvement in the labor market. Unemployment is down to 5.1% and initial jobless claims indicate the rate will move even lower in the coming months. Further, we are finally seeing some signs of upward pressure on wages. Companies unable to find skilled workers for open positions is becoming an increasingly common story. This was confirmed by the lack of hiring despite a large number of job openings in the recent Job Opening and Labor Turnover Survey (JOLTS) release.

Hiring lagging despite high vacancy rate—higher wages needed?

Source: FactSet, U.S. Dept. of Labor. As of Sept. 17, 2015.

The growing evidence suggests we may start to see wages increase at a more rapid rate, which should further bolster the consumer. But the rub is that corporate profit margins may also feel the pressure as labor costs accelerate without the benefit of better top-line growth. At this point, we think margin pressure will be somewhat limited and will likely be largely offset by the increased demand coming from more flush consumers.

Fed punts, Congress squabbles—some things never change

The long-pointed to September Fed meeting has come and gone (read more at Fed Punts and Keeps Rates Unchanged by Liz Ann Sonders). The lack of a move was greeted less than enthusiastically by the market and the continued dovish tone and clear desire to move slowly in returning rates to a more normal level raised concerns that the global economy may be worse than investors currently believe—leading to more volatility. Continued dovishness is perceived to be a positive for equities, but there are risks to delaying the start of normalization; including the attendant uncertainty as a weight on the market and confidence.

Although somewhat overshadowed by the Federal Reserve, Congress returned from their summer break, only to be met with the possibility of another government shutdown due to the lack of a budget agreement. The current budget expires on September 30th but talks have begun on extending that expiration date by ten weeks. According to our Washington expert Michael Townsend, the odds of a shutdown on October 1st have increased, although it’s far from a fait accompli. At this point, even if we do see a shutdown, we believe it will be relatively short-lived and have little impact on investors, as there is not the threat of a debt default as was the case in recent government budget debates.

BARC worse than bite

The weak spot in the global economy is currently centered on commodities. The value of commodity output is falling along with prices. Manufacturing excluding commodities is relatively flat, according to data reported by the governments of major countries and regions like the United States, Eurozone, and Japan. At the same time, services are growing in these countries, measured by the latest releases of the service purchasing managers indexes (PMIs).

On balance, this is good news since services make up 75-80% of GDP for these countries. But those countries with economies more focused on commodities have fallen away from the rest. Canada’s second quarter gross domestic product (GDP) report released in September revealed the country has officially entered a recession; joining the group of commodity-driven economies in recession that includes emerging market countries Brazil and Russia. Australia, a developed market economy like Canada, may be the next to join the club despite being able to avoid a recession for almost 25 years.

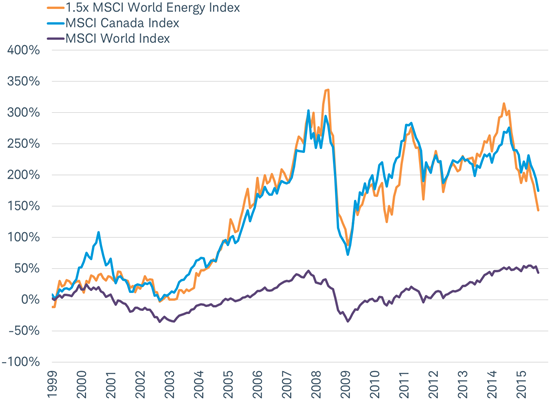

The commodity-driven slow-downs in the BARC (Brazil, Australia, Russia, and Canada) economies are being felt in the stock markets. In fact, just how commodity-driven these countries’ stock markets are can be seen in the chart below. Canada's stock market has behaved like 1.5 times the MSCI World Energy sector index over the past 15 years. That concentrated exposure helped a lot on the upside over the past 15 years, but cuts both ways as commodity prices have crashed over the past year pulling Canada’s stock market down along with it.

Canada’s Stock Market has Behaved like a Leveraged Bet on Energy Stocks

Source: Charles Schwab, Bloomberg data as of 9/22/2015.

Fortunately, the BARC is worse than their bite. The loss for the BARC countries is typically a gain for many other economies. Unlike a financial contagion that has a negative impact across countries, the offsetting impact of the plunge in commodity prices on different economies limits the ability to take a bite out of global economic growth.

This week’s PMI data provided the most up-to-date reading on the global economy which is important to investors for assessing where the economy, stocks, and the Federal Reserve are headed. While China’s manufacturing slowdown of the past year and a half continued in September, the Eurozone remained in expansion for the twenty-seventh straight month; with both manufacturing and services growing, albeit at a slightly slower pace than in August. The Eurozone composite PMI, which incorporates both service and manufacturing, pulled back only modestly from a four year high, showing little sign that the global economy is rapidly slowing. In fact, forward-looking components like new orders hit a five-month high and manufacturing orders were close to August's 16-month high. The overall message in the data is that global growth remains relatively stable despite the recessions in commodity-driven economies and the volatility in markets.

So what?

Uncertainty surrounding the Federal Reserve continues after its punt of rate hikes at its most recent meeting. But as the market gets more clarity on monetary policy and given a still-growing US economy, the bull market should slowly reestablish itself, albeit with bouts of volatility. Further support should come from global growth in areas that are net beneficiaries of the plunge in commodity prices.

(c) Charles Schwab