Under Pressure: Earnings Recession Warning; Economic Recession Watch

Key Points

- S&P earnings are expected to head south into negative territory; bringing overall economic worries along with them.

- Recession risk remains relatively low.

- Tailwinds will likely reign over headwinds; but being on recession watch looking ahead is warranted.

Many of the questions I’ve been getting recently at client events are around earnings, and whether the expected move into negative territory for earnings growth is a signal of a pending economic recession.

As you can see in the chart below, S&P 500 earnings recessions (when the blue line dips sub-zero) and economic recessions (gray-shaded regions) often come hand-in-hand. But there are plenty of exceptions—when earnings growth dips into negative territory, but the economy’s growth remains out of recession. Since 1986, there have been four such periods, as noted by the circles on the chart.

Earnings and Economic Recessions Often Linked…But Not Always

Source: Bureau of Economic Research, FactSet, Strategas Research Partners LLC. EPS (earnings per share) as of September 30, 2015, and based on 12-month operating consensus estimates. GDP as of 2Q15. Gray-shaded areas indicate periods of recession.

Energy sector under pressure

A common thread among the losing earnings periods was falling oil prices—and typically a strengthening US dollar—clearly a defining characteristic of today’s environment. The way this has played out in the past (and is possible currently) is lower oil prices immediately dent energy sector earnings, while a stronger dollar immediately dents multinationals’/exporters’ earnings due to the currency translation effect. A strong dollar not only makes US-made goods more expensive and less competitive globally; it also favors non-US manufacturers, since they can afford to sell their goods for less in the United States. But, keep in mind that exports represent only 13% of the US economy, while consumption represents 68%.

Ultimately, given that the US economy is consumption-driven, weaker oil and other commodity prices are economic benefits. In other words, the hit comes first; while the offsetting economic positive, especially related to consumption, comes a bit later. As such, weakness in the export-oriented manufacturing sector must be viewed with an appropriately-tinted lens.

Yes, the ISM Manufacturing Index is barely in expansion territory (above 50); but it represents only 12% of the US economy. The ISM Non-Manufacturing Index is just under 57; and represents the much larger 88% of the US economy that is services-oriented. Within the latter index, orders remained solid and employment rose to a very strong reading, adding to evidence that last Friday’s weak jobs report mainly reflected typical volatility in the data.

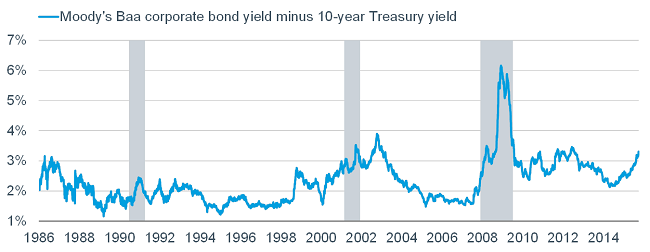

Spreads under pressure

Elsewhere in the corporate sector though, there are signs of stress and the contraction in earnings should not be dismissed. There has been a relentless widening of US credit spreads, as you can see below.

Credit Spreads on the Rise, Signaling Stress

Source: FactSet, as of October 1, 2015. Gray-shaded areas indicate periods of recession.

This is but one signal of tighter financial conditions—the stronger dollar being another. Weak global growth and trade means the US economy is yet again importing deflation, which is why expectations for an initial rate hike by the Federal Reserve this year have plunged. It’s also why profit margins have been under pressure.

Profit margins under pressure

From an all-time high of over 9% reach in 2014, S&P 500 profit margins have dropped by 60 basis points over the past year and now sit at 8.5%. Declines of this magnitude are rare outside of recessions, other than in 1985, which was the only time in the past 40 years margins dropped this much without an attendant recession according to Barclays. It’s an important reference point because profit margins fell in 1985 due to a 60% plunge in oil prices; while profit margins outside of the energy sector remained stable.

Over the two years, energy sector net profit margins have imploded from over 8% and are now on their way toward 2%. On the other hand, the collective revenue-weighted net profit margin of the other nine S&P sectors has continued to trend marginally higher and sits near an all-time high, which means earnings pressure will also be mostly felt within the energy sector.

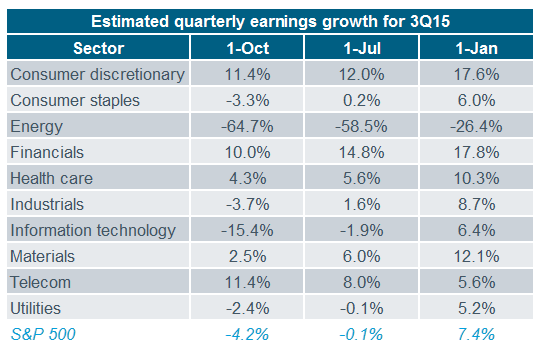

Earnings expectations under pressure

As you can see in the table below, current estimates point to an earnings contraction in the third quarter over more than 4%. The column after that shows that at the end of the second quarter, analysts were less bearish on the third quarter, with a consensus of a marginal decline. And relative to the consensus expectation at the beginning of the year of 7.4% for the third quarter, you can see how far estimates have fallen.

Source: Thomson Reuters, as of October 2, 2015.

Also clearly evident in the data above is the massive hit to earnings of the energy sector—the consensus is for a drop of nearly 65%; with the materials sector the only other double-digit loser at -15.4%. It’s glaringly obvious when looking at these figures that the plunge in oil and other commodities is taking its toll.

Looking ahead, there is hope though. Domestic-sourced profits for US companies are 2.5 times larger than foreign-sourced profits and were up 3.6% quarter-over-quarter in the second quarter; and are 16% above their 2006 peak, according to Cornerstone Macro. On the other hand, foreign profits were up 3.8% quarter-over-quarter in the second quarter; but are up a lesser 9% from their 2008 peak. The decoupling between domestic- and foreign-sourced profits is likely to persist.

Economy under (some) pressure

As witness to the earnings contraction, it’s natural to wonder about the ripple effects into the broader economy, especially following last Friday’s weak jobs report. Whether that report is the beginning of a shift, or just an outlier, is yet to be seen.

But the release was disappointing nearly across the board:

- Payroll growth was below expectations

- Prior two months’ payrolls were revised down

- Average hourly earnings stagnated

- Average workweek fell

- Participation rate fell to 38-year low

- U-6 “underemployment” rate fell to 10% for first time since May 2008 (only good news within report)

Economic tailwinds

Nothwithstanding the weak jobs report and the aforementioned deflationary headwinds, we are sticking with our view that an economic recession is not imminently in the cards. Not only are employment and real income growth still relatively healthy, consumer confidence and consumption growth have been notably strong—especially in housing and autos. Construction spending has risen to a new post-recession high and is within a few basis points of an all-time high in year-over-year percentage change terms.

Recessions come when excesses have built in the economy. But the current expansion is unique in history because it hasn’t yet recovered to its prior trend rate of growth. As such, there remains a huge “output gap,” with money and resources remaining fairly abundant.

At some point, perhaps soon, energy capital spending’s decline should begin to stabilize, after a near-30% plunge in the first half of this year. And government spending is turning around. According to Bank Credit Analyst (BCA), government spending on goods and services subtracted close to 50 basis points from per capital US growth over the past five years, compared to past recoveries where government spending added an average of 35 basis points to per capita growth. A reversal of this trend should spur aggregate demand.

Economic headwinds

I’ve already touched on the pressure on earnings and profit margins, as well as widening credit spreads. Persistent strength in the US dollar would continue to act as a tightening mechanism. There is also the possibility that some of the stronger tailwinds propelling the US economy begin to fade, including consumer and business confidence (courtesy of stock market volatility), bank lending standards, elevated asset values (houses, stocks, etc.), and 0% interest rates.

Looking globally, for the first time since the 1970s, global trade is growing more slowly than global gross domestic product (GDP). The common thinking is that it reflects weak global demand and/or the collapse in the velocity of money; both of which exacerbates deflationary pressures.

But GavekalResearch has a different and interesting take worth considering. Perhaps the trade slowdown reflects structural changes in the world economy, and signals that we are entering a new phase of globalization. We may be moving from a “Ricardian” growth era whose major beneficiaries were established multinationals and emerging Asia; to a “Schumpeterian” one in which the advanced industrial economies and innovative new firms will take the lead. Tasty food for thought; and in keeping with our thought that the developed markets are likely to outperform the emerging markets in the near-to-intermediate term.

In sum

The net is that it’s a mixed bag. An earnings recession is very likely; while an economic recession less so. Cornerstone Macro looks at 12 Recession Risk Indicators, and as you can see below, only one points to a recession.

- PCE deflator: No

- CPI energy: No

- Unit labor costs: No

- Average hourly earnings: No

- Consumer delinquency rate: No

- Residential construction% of GDP: No

- Total investment % GDP: No

- Output gap % potential GDP: No

- Domestic corporate profits % GDP: No

- Yield curve: No

- Global short rates: No

- BAA spreads: Yes

We believe an economic recession remains unlikely near-term, but we are on watch. We are maintaining our more cautious “neutral” rating on US equities, which means investors should not take any additional risk above and beyond their long-term allocation to equities.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(1015-6249)

© 2015 Charles Schwab & Co., Inc, All rights reserved.