Key Points

- 2015 has been a disappointment thus far for equity investors, but the fourth quarter has typically been a positive one. The US economy is a mixed picture but the preponderance of evidence still points to sustained growth.

- The Federal government followed up the Federal Reserve and punted, extending funding for ten weeks and avoiding a government shutdown. December appears to be shaping up to be quite active on the policy front, which should keep volatility elevated.

- European inflation readings were disappointing on the surface, but the core rate provides encouragement. More quantitative easing may be needed, to the potential benefit of European stocks.

Good riddance

The third quarter is not going to be one most investors were sorry to see go. It marked the worst quarter since 2011 for the major indices, while the increase in volatility was a marked change from the low volatility and tight trading range in the first seven months of the year. Further, it marked the third-straight losing quarter for the Dow, which, according to MarketWatch, is the longest losing streak since the 2007-2009 recession, and only the third such streak in almost 40 years—good riddance!

But just because the calendar changes doesn’t mean we can start fresh, whether it’s the start of a year, or simply the start of a new quarter. We expect bouts of volatility to persist as global growth concerns stay with us; while Fed uncertainty along with a budget fight in Congress is likely to keep investors on edge. But there is precedent for a possible fourth quarter comeback. As we mentioned, the third quarter was the worst quarter for the S&P since 2011—in fact, so far this year the stock market has a 0.92 correlation with 2011’s; a remarkably similar pattern. Were the similarity to persist, it would bode well for the fourth quarter this year. In 2011, the S&P was up a robust 6%; bringing along with it holiday retail sales growth of 6.8%. And that goes to the seasonality advantage that we are heading into. According to Ned Davis Research, we are coming out of what since 1952 have been the worst months of the year for the stock market—August through October—while heading into the historically best three months—November through January. We often borrow a quote attributed to Mark Twain: “History doesn’t repeat itself, but it does rhyme.” Although we are maintaining our neutral rating on US stocks (meaning don’t take excess risk above your long-term equity allocation), for investors with excess cash and below their normal equity allocation, it may be appropriate to put some of that cash to work.

Glass 88% full, 12% empty?

Helping keep us relatively optimistic on US stocks is the continued strength in the service side of the economy, which makes up roughly 88% of activity according to High Frequency Economics (HFE). Of course, there is some bleeding of the manufacturing sector into the services sector, so the 12% representing traditional manufacturing is not irrelevant. There is no doubt that US manufacturing has weakened over the past several months, due to China’s growth slowdown, the strength in the US dollar, and the weakness in commodity prices. In particular, we have seen sizeable corrections in energy and basic materials stocks (read more at Bottom Fishing? By Brad Sorensen). The Institute of Supply Management’s (ISM) Manufacturing Index fell again, barely remaining in territory depicting expansion (>50), while the new orders component followed suit. Meanwhile, ISM’s Non-Manufacturing Index, representing the service side of the economy, also slipped modestly but remained well above the key level of 50, as did the new orders component.

Services strength is offsetting manufacturing weakness for global economy

Source: Charles Schwab, Bloomberg data as of 9/9/2015.

The slowdown in China and the manufacturing sector has impacted those US companies which do more business overseas, especially the energy and materials spaces as mentioned, but also extending to more internationally-based industrial and tech-related industries. Meanwhile, domestically-oriented companies have generally fared better. And the all-important US consumer appears to be relatively unfazed, helped by lower energy costs and a strengthening labor market.

Consumer supports continuing

Source: FactSet, Dow Jones & Co. As of Oct. 5, 2015.

Source: FactSet, U.S. Dept. of Labor. As of Oct. 5, 2015.

Jobs data continues to improve, despite the disappointing September labor report. Initial unemployment claims remain at historic lows, but the September labor report showed only 142,000 jobs were added, below expectations, while the previous two months were revised lower by 59,000. The unemployment rate remained at 5.1% but average hourly earnings were flat month-over-month. But despite the stock market volatility, Fed uncertainty, and global growth concerns, US consumer confidence rose in September according to the Conference Board—surprising economists who expected it to fall. Consumer spending also appears to be solid, as we saw a solid 0.4% gain month-over-month in August—potentially boding well for the holiday shopping season, while also providing support for the US economy and a potential fourth quarter stock market rally.

Punting competition in Washington

A risk to the fourth quarter rally possibility is the continued, and perhaps escalating, policy uncertainty in Washington. The Federal Reserve has an October meeting but it seems unlikely that concerns mentioned in their September meeting as reasons not to hike rates will have resolved themselves by then. Add to that the disappointing labor report and it probably takes it an October rate hike off the table. But December is still in play for the first hike since 2006.

Adding to the likely volatility associated with Fed uncertainty is the budget fight in Congress. Lawmakers did manage to avoid a government shutdown on October 1 by agreeing to a temporary funding measure that goes through December 11. But it gets a little more difficult because the debt ceiling will also need to be raised in the next couple of months, and the fight over sequester level funding will also escalate. Temporary measures damage business confidence and there is talk about trying to get a two-year deal done to avoid these problems in a highly-charged election year. Frankly, we’d be surprised if Congress got a full 2016 budget agreement by the December deadline, but hope springs eternal.

QE 1493

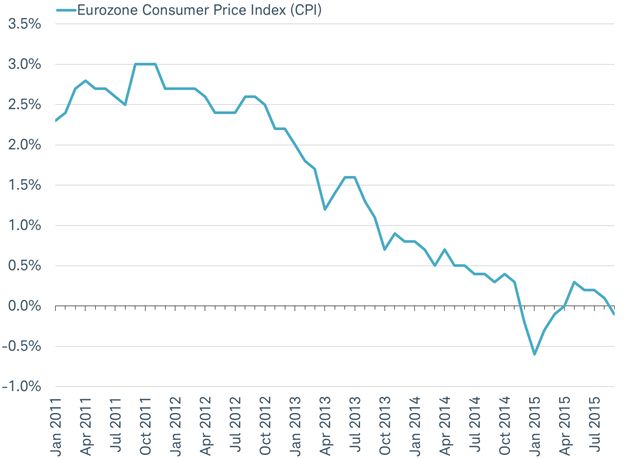

The Eurozone’s inflation rate unexpectedly turned negative in September for the first time in six months, adding pressure on the European Central Bank (ECB) to add to its quantitative easing (QE) bond buying program.

Eurozone returns to deflation

Source: Charles Schwab, Bloomberg data as of 10/7/2015.

Declining prices are largely a consequence of falling oil prices—core prices (excluding energy and food) remained unchanged at +0.9% in September, sustaining their rebound since the ECB’s QE began in March. The QE program has now been in place for six of the scheduled 19 months. However, policy makers including ECB President Mario Draghi have signaled that they could expand QE if needed to avert deflation. (For insights on the risks that deflation poses see: Deflation: What Investors Need to Know)

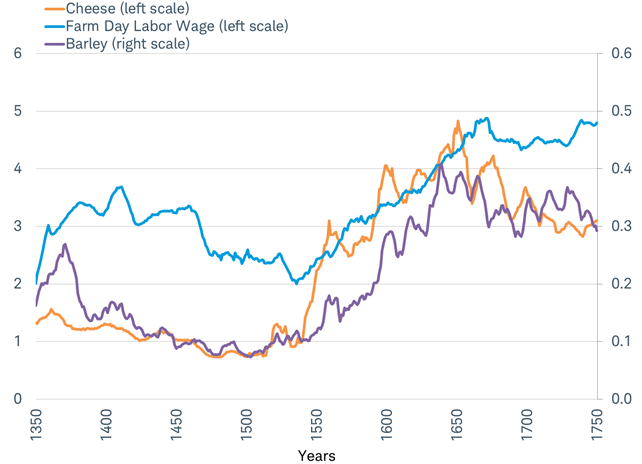

We celebrate Columbus Day on October 12 when he landed in the Americas in 1492. But Europe is looking to March 15, the day he returned to Europe in 1493, as something to celebrate. That was the last time there was a great boost to the money supply in Europe that brought an end to deflation. The start of a huge flow of gold and silver from the Americas ended about 150 years of deflation and began 150 years of inflation.

QE 1493: From Deflation to Inflation

UK prices in grams of silver

Source: Charles Schwab, Gregory Clark, "The Price History of English Agriculture, 1209-1914," Research in Economic History, data as of 2004.

For about 150 years before Columbus returned to Europe with all that money, prices were falling measured in silver, the money of the time. These prices included consumer goods like cheese, producer ingredients like barley, and even the minimum wage for unskilled labor earned by farm laborers. But once Columbus returned, and the flow of treasure from the Americas began, inflation took off with prices steadily rising.

Much like the Italian Captain Columbus, the captain of the ECB, former Italian finance minister Mario Draghi, has sought to reverse Europe’s deflation through supporting growth in the money supply by bringing the treasured American-style QE to Europe. Once “QE 1493” ended, after about 150 years, deflation returned to Europe around the year 1650. The consensus of economists tracked by Bloomberg is that the ECB will add to its 1.1 trillion euro QE program before the end of this year. The most likely action will be to extend QE beyond September 2016 for another 19 months until mid-2018, resulting in a 2.4 trillion euro program, equivalent to nearly 25% of the Eurozone economy.

While QE should help to boost inflation and may lend support to the Eurozone economy, the real effect is felt in the markets, where the actual buying is taking place and seeking to drive up the prices of financial assets like bonds and stocks. If the average ratio of Europe’s stock market capitalization to the size of the ECB’s balance sheet of 1.25 from 2009-present continues as the QE program adds to the balance sheet each month, it could mean that the ECB’s 60 billion euro per month QE program alone could lift the stock market by 2% per month. While such a direct effect is unlikely, it does offer some degree of support for the European stock market and something we may want to celebrate this Columbus Day weekend.

So What?

A disappointing year to this point for the US stock market has a chance to end on a better note, with good seasonality and a still-growing economy as supports. Consumers are in good shape, the Fed remains accommodative, and the much-larger service side of the US economy is still healthy. But Fed uncertainty, Congressional budget battles, and Chinese growth concerns will remain as headwinds and will likely contribute to continued bouts of volatility. Across the pond, the European fight against deflation appears to be working, although more QE may be needed, to the potential benefit of European stocks.

(c) Charles Schwab