Key Points

- After an October that was almost straight up for stocks, a dose of reality hit the market in November. The digestion of gains is healthy as it keeps investor sentiment in check, which should help to keep the long-term bull market intact.

- A robust October jobs report pushed the probability of an initial Federal Reserve rate hike in December higher. We agree it’s likely the Fed will finally move off the zero bound, but reiterate that the pace is likely to be slow—which has historically been a positive for stocks.

- The human toll of terrorist attacks is immeasurable but the financial impact tends to be limited when looking at history.

Please note: Due to the Thanksgiving holiday the next Schwab Market Perspective will be published on December 11, 2015.

A dose of reality

After an October that had the bulls roaring ahead at full speed, November has brought the proverbial speed bump. After the dovish result of the Fed’s September meeting, stocks surged as investors breathed a sigh of relief. October’s meeting, however, threw some cold water on the situation, with the Fed noting specifically that a December rate hike was still very much on the table, and the robust October jobs report reinforced that possibility. Investor sentiment according to Ned Davis Research’s Crowd Sentiment Poll reached excessive optimism territory alongside the October rally, while earnings season didn’t back up the sharp increase in prices in many cases. This set up the recent consolidation of gains in November.

We view the recent pullback as a pause that refreshed and recommend investors remain at their long-term equity allocations; in line with our “neutral” rating on stocks. Looking ahead, more choppy action seems likely as we approach the December Fed meeting and deal with increased global security concerns. Additionally, there is increasing angst about the holiday shopping season after some disappointing results from retailers. On a technical level, stocks market breadth has been relatively narrow—a sign of “distribution” (stocks moving from strong hands to weaker hands) —indicating the possibility of more volatility. The good news is that we are in a positive seasonal time of the year for stocks, and many areas of the economy continue to show strength.

Glass more than half full

The US economy is currently bifurcated; with manufacturing recently near contraction territory, but services showing healthy growth. Given the 12% and 88% respective weights in the economy, a broader recession is unlikely. In addition, the outperformance of the industrials sector since the August-September correction suggests the worst may be over for the manufacturing sector.

Along with the robust October labor report, average hourly earnings posted a nice gain, indicating we may be finally getting the increase in wages we’ve been expecting. Further, the National Federation of Independent Business Survey recently indicated that small business confidence remains steady, while 17% of respondents plan to increase compensation over the next year, the highest reading in eight years.

This should help to support the consumer, whose status remains in question. The recent retail sales report showed lackluster growth with sales ex-autos and gas rising by 0.3%—not great, but not terrible either. But within the consumer sector there are some conflicting signals. For example, auto sales continue to move higher, indicating improving consumer confidence.

Auto sales indicate a confident consumer

Source: Bloomberg. As of Nov. 17, 2015.

We have to recognize that there is a new, and perhaps “smarter” consumer, born out of the financial crisis and subsequent deleveraging cycle. In particular, consumers are increasingly anxious about taking on more revolving debt to fund consumption. In addition, some traditional retail measurements may not best capture the full scope of changing consumer behaviors. For instance, more money, according to recent retail sales reports, appears to be going toward experiences rather than goods, and the purchases that are made increasingly move to more nontraditional spaces. For example, e-commerce sales are up 11.2% year-over-year (y/y) on a nominal basis, while sales in food service and drinking places are up 8.4% y/y according to Cornerstone Macro Research. So be careful about those sounding the death knell for American consumers—they appear to be spending more conscientiously and in different places and ways than in years past.

Consumers appear reluctant to add to debt

Source: FactSet, Federal Reserve. Includes mortgage and consumer debt, auto lease payments, rental payments, homeowners insurance, and property tax payments. As of Nov. 17, 2015.

We remain optimistic about the 68% of the US economy driven by consumer spending as wages appear to be rising, and lower energy costs leaves more discretionary money in consumers’ pockets.

Will the Fed follow Congress and break the cycle?

Investors’ attention remains squarely on the Fed and its upcoming mid-December meeting. Perhaps the Fed can look down the street in DC for inspiration. Congress finally broke the cycle of deadline deals and month-to-month budgeting as they agreed to suspend the debt ceiling for two years, while also putting in place a broad budget for two years. There are still appropriations fights to be had, but the lack of political brinksmanship should help.

Now we’ll see if the Fed can break the cycle its been in for some time. For much of this year, we’ve seen any sort of hawkish commentary from the Fed result in a strengthening of the US dollar and pleas from foreign sources, such as the International Monetary Fund (IMF) not to raise rates. The strengthening of the dollar has a tightening effect as it makes US goods less competitive abroad—but also tends to hold down inflation, especially in commodities that are traded in dollars, such as oil. This combination has then led to dovish comments by Fed members to ease concerns and a continued holding of interest rates at rock bottom levels. This is the “Fed Policy Loop” discussed in Liz Ann’s latest commentary.

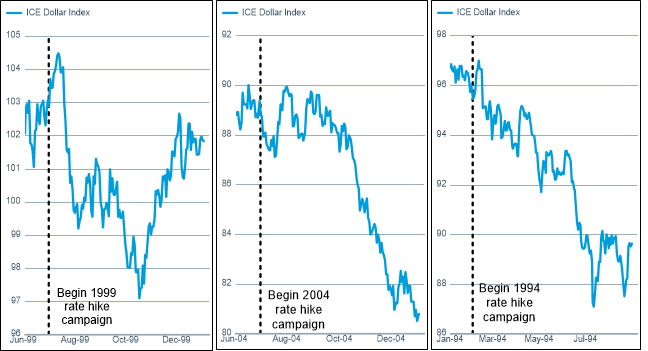

Will strengthening dollar derail the Fed?

Source: FactSet, Intercontinental Exchange. As of Nov. 17, 2015.

Although we believe the dollar is in a long-term bull market, there is some historical precedence for the dollar to retreat a bit once the Fed starts to raise rates—call it a “buy the rumor, sell the news” scenario, as seen below.

Sell the news?

Source: FactSet, Intercontinental Exchange, Cornerstone Macro. As of Nov. 17, 2015.

Economic data, especially the next jobs report, will guide the Fed over the next month. We lean toward a December initial hike, but believe it will be accompanied by a fairly dovish statement. And the pace of hikes is likely to be quite slow, at least at the beginning, given the Fed won’t be chasing an inflation problem. This environment should continue to be generally positive for stocks, but likely marked with continued bouts of volatility.

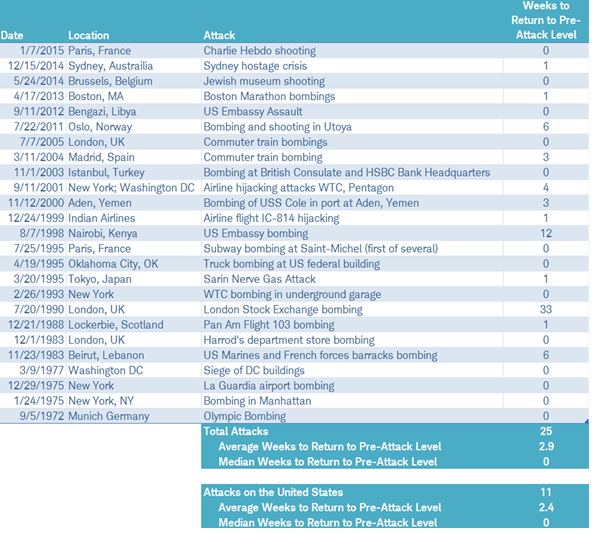

Global stock market impact of terrorist attacks

The impact of the terrorist attacks in Paris will stay in our hearts and minds long after any economic cost is recouped. The human toll is immeasurable. Unfortunately, we have a long history of terrorist attacks worldwide over the past 25 years that give us a lot of history to examine to assess their market and economic impacts.

Historically, major acts of terrorism have not had lasting negative effects on financial markets. In fact, in the countries where these terrorist attacks occurred the stock market fully recovered in less than a week in most cases and within three weeks, on average.

Market reactions to 25 terrorist attacks over the past 45 years

Source: Charles Schwab, Factset & Bloomberg data as of 11/6/2015.

Indexes used for attacks on: U.S. and U.S. military or embassies = S&P 500; UK and UK consulate = FTSE 100 (except 12/1/83 MSCI United Kingdom Index); Norway = Oslo Stock Exchange -OBX; France = CAC 40; Germany = DAX Index; India = Bombay Exchange Sensitive Index SENSEX Index; Spain = IBEX 35; Japan = Nikkei 225; Australia = ASX 200; Belgium = BEL 20; Canada = S&P TSX Index.

In the past, global stock markets had more significant reactions to changing economic fundamentals and geopolitical events rather than terror attacks. An example can be seen in the lengthy stock market decline that followed, but was unrelated to, the London Stock Exchange Bombing in 1990. That attack was followed two weeks later (August 2, 1990) by Iraq’s invasion of Kuwait and the start of a recession in the United States. Similarly, the bombing of the US embassy in Kenya in August 1998 took place just as the unrelated Asian financial crisis erupted.

With the exception of the 9/11 attacks on the United States, there has never been a terrorist attack that has materially and negatively affected economic activity in a major country. The 9/11 attacks depressed economic activity for a very short period as November 2001 marked the end of the recession that began in March, and the US economy posted a gain in gross domestic product (GDP) in the fourth quarter. The stock market responded similarly. Within a week of reopening after the 9/11 attacks, the stock market was rallying—in the following nine weeks, the S&P 500 posted a gain of 20%. (For insight into what the Paris attacks may mean for the Fed see Liz Ann’s Wave of Sorrow piece.)

Resilient France

Nevertheless, there is still the risk that, for the first time in history, a terrorist attack would result in a serious disruption of economic activity and cause substantial declines in the markets. However, in recent months France has shown signs of improving economic growth, along with the rest of the Eurozone, making it likely that it will prove to be resilient to the Paris attacks. For example:

- Manufacturing in France is expanding again with the Markit France manufacturing purchasing managers index (PMI) having moved back above 50 in the past two months, continuing the steady improvement in that index over the past year.

- The year-over-year pace of retail sales in France in recent months has grown at the fastest pace in more than four years, per data from Eurostat.

- France’s business confidence composite index published by France’s National Statistics Office has been rising steadily this year to the highest level since 2011.

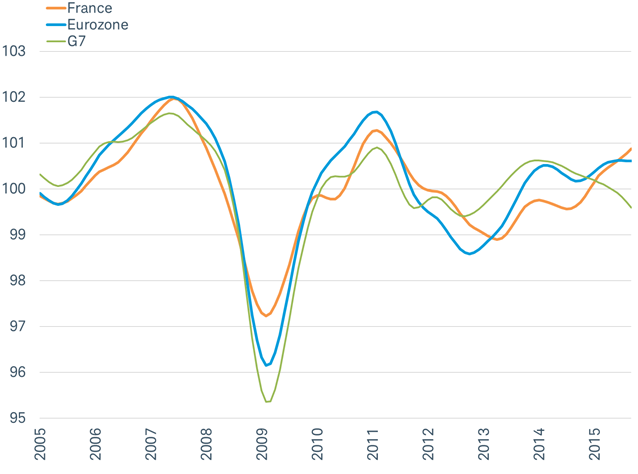

- The OECD (Organization for Economic Cooperation and Development) index of leading economic indicators for France remains on the rise, outpacing the modest gains in the index for the Eurozone and the slump in the index for the Group of 7 (G7) countries.

France’s index of leading economic indicators is outpacing the region and global peers

OECD composite index of leading indicators by country and group

Source: Charles Schwab, Bloomberg data as of 11/16/2015.

G7 = group of seven major advanced economies as reported by the International Monetary Fund: Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

Further support for stocks in France and elsewhere in Europe may come from the European Central Bank (ECB) at its upcoming December 3 meeting. ECB members have been signaling that a further cut to interest rates and a possible extension of its quantitative easing (QE) program may be forthcoming, citing concerns over weak inflation. European stocks had reacted positively to the announcement of the QE program in January of this year, and when the deposit rate was last cut in 2014, measured by the STOXX Europe 600 index.

So what?

Stocks have pulled back after their rip higher in October, which we believe is healthy and in keeping with our expectation of continued volatility. The US economic picture is mixed, but the recent robust labor report boosted the odds of a December Fed rate hike. Finally, while difficult to think about financial matters in the face of such horrific events as the Paris attack, the resilience of both people and economies around the world should give us all hope for the future.

(c) Charles Schwab